摩托车及其他

Search documents

大族激光目标价涨幅超60%,嘉益股份、太辰光评级被调低|券商评级观察

2 1 Shi Ji Jing Ji Bao Dao· 2025-10-30 01:25

Group 1 - The core viewpoint of the article highlights significant target price increases for certain companies, with Dazhu Laser, Qianjiang Motorcycle, and Lihigh Food leading the rankings with target price increases of 62.27%, 54.74%, and 54.33% respectively, indicating strong market confidence in these sectors [1] Group 2 - On October 29, brokerages lowered ratings for two companies: Huazhong Securities downgraded Jiayi Co., from "Buy" to "Hold," while Qunyi Securities (Hong Kong) downgraded Taicheng Light from "Buy" to "Range Trading," reflecting a cautious outlook on these firms [1]

泉果基金孙伟:消费复苏需观察政策实施力度,三季度增配新消费与锂电

Sou Hu Cai Jing· 2025-10-29 09:20

Core Insights - The report from the "泉果消费机遇" fund indicates a significant growth in fund size, reaching 695 million yuan by the end of Q3 2025, up from 61.93 million yuan in Q2 2025, reflecting increasing recognition from investors, including institutions [1][2] - The fund's net value performance shows a 33.00% increase over the past year, outperforming the benchmark of 3.69% [1] Fund Performance and Market Context - The fund has gained favor among institutional investors, with 2.856 million shares held, accounting for 4.96% of total shares [2] - In Q3 2025, major stock indices performed well, with the Shanghai Composite Index rising by 12.73%, Shenzhen Component Index by 29.25%, CSI 300 by 17.90%, and Hang Seng Index by 11.56% [2] - Economic indicators showed steady growth, with industrial added value increasing by 5.7% and 5.2% in July and August respectively, and retail sales growing by 3.7% and 3.4% in the same months [2] Portfolio Adjustments - The fund manager, Sun Wei, indicated a slight increase in equity positions and adjustments in the portfolio structure, focusing on new consumption and lithium battery sectors [3] - The fund increased allocations in personal care, trendy toys, and gaming industries while reducing exposure in closely related sectors [3] - The top ten holdings account for 30.12% of the fund's net asset value, with Tencent Holdings, CATL, and Pop Mart among the largest positions [5] Investment Strategy - As of Q3 2025, the fund's stock position constituted 79.01% of its net assets, with a 24.77% allocation to Hong Kong stocks, showing stability compared to the previous quarter [4][3] - New entries in the top ten holdings include Pop Mart, Alibaba-W, and Tianqi Lithium, while previous holdings like Yanjing Beer and Li Auto have exited the list [3][5]

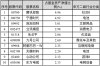

摩托车及其他板块10月28日涨0.12%,征和工业领涨,主力资金净流出1.51亿元

Zheng Xing Xing Ye Ri Bao· 2025-10-28 08:33

Market Overview - On October 28, the motorcycle and other sectors rose by 0.12%, led by Zhenghe Industrial. The Shanghai Composite Index closed at 3988.22, down 0.22%, while the Shenzhen Component Index closed at 13430.1, down 0.44% [1]. Stock Performance - Zhenghe Industrial (003033) closed at 86.53, up 10.01% with a trading volume of 51,900 shares and a transaction value of 432 million yuan [1]. - Shanghai Phoenix (600679) closed at 13.53, up 3.28% with a trading volume of 202,500 shares and a transaction value of 275 million yuan [1]. - TaoTao Vehicle (301345) closed at 252.20, up 2.40% with a trading volume of 18,100 shares and a transaction value of 454 million yuan [1]. - Qianli Technology (601777) closed at 11.41, up 1.78% with a trading volume of 421,100 shares and a transaction value of 480 million yuan [1]. - Other notable performances include Xinlong Health (002105) up 1.58% and Chunfeng Power (603129) up 0.52% [1]. Capital Flow - The motorcycle and other sectors experienced a net outflow of 151 million yuan from main funds, while retail funds saw a net inflow of 62.61 million yuan [2]. - The main funds showed a net outflow in several stocks, including Zhenghe Industrial and Qianli Technology, while retail investors contributed positively to stocks like Green通科技 [3]. Detailed Stock Capital Flow - Zhenghe Industrial had a main fund net outflow of 33.16 million yuan, with retail inflow of 21.91 million yuan [3]. - Qianli Technology saw a main fund net inflow of 13.31 million yuan, but retail investors had a net outflow of 15.13 million yuan [3]. - Chunfeng Power had a main fund net inflow of 9.84 million yuan, while retail investors had a slight outflow [3].

永安行涨2.21%,成交额5119.87万元,主力资金净流入19.73万元

Xin Lang Cai Jing· 2025-10-27 05:56

Group 1 - The stock price of Yong'an Xing increased by 2.21% on October 27, reaching 19.90 CNY per share, with a total market capitalization of 5.587 billion CNY [1] - Year-to-date, Yong'an Xing's stock price has risen by 56.45%, but it has seen a decline of 8.13% over the past 20 days and 9.46% over the past 60 days [1] - The company has appeared on the trading leaderboard five times this year, with the most recent instance on June 26, where it recorded a net buy of -32.5976 million CNY [1] Group 2 - Yong'an Xing Technology Co., Ltd. was established on August 24, 2010, and went public on August 17, 2017, focusing on shared mobility systems based on IoT and big data analysis [2] - The company's revenue composition includes: system operation services (35.18%), shared mobility services (21.06%), hydrogen products and services (19.40%), smart living services (13.76%), and system sales (10.59%) [2] - As of June 30, the number of shareholders increased by 5.04% to 16,600, while the average circulating shares per person decreased by 4.58% to 14,549 shares [2] Group 3 - Yong'an Xing has distributed a total of 438 million CNY in dividends since its A-share listing, with 158 million CNY distributed over the past three years [3]

爱玛科技跌2.02%,成交额2.56亿元,主力资金净流出1387.64万元

Xin Lang Cai Jing· 2025-10-27 03:07

Core Viewpoint - Aima Technology's stock has experienced a decline of 18.32% year-to-date, with recent trading activity showing a slight recovery in the last five days, but a continued downward trend over the past 20 and 60 days [1][2] Financial Performance - For the period from January to September 2025, Aima Technology reported a revenue of 21.093 billion yuan, representing a year-on-year growth of 20.78%. The net profit attributable to shareholders was 1.907 billion yuan, reflecting a year-on-year increase of 22.78% [2] Stock Market Activity - As of October 27, Aima Technology's stock price was 32.51 yuan per share, with a market capitalization of 28.255 billion yuan. The stock saw a trading volume of 256 million yuan and a turnover rate of 0.92% [1] - The stock has been on the "龙虎榜" (a list of stocks with significant trading activity) once this year, with the last appearance on February 6, where it recorded a net buy of 944,700 yuan [1] Shareholder Information - As of September 30, 2025, Aima Technology had 31,700 shareholders, an increase of 33.58% from the previous period. The average number of circulating shares per shareholder decreased by 25.19% to 26,718 shares [2] - The top ten circulating shareholders include Hong Kong Central Clearing Limited, which increased its holdings by 1.7094 million shares, and Southern CSI 500 ETF, which reduced its holdings by 74,000 shares [3] Dividend Distribution - Aima Technology has distributed a total of 3.056 billion yuan in dividends since its A-share listing, with 2.851 billion yuan distributed over the past three years [3] Business Overview - Aima Technology, established on September 27, 1999, and listed on June 15, 2021, specializes in the research, production, and sales of electric bicycles. The main revenue sources are electric two-wheelers, electric three-wheelers, bicycles, and accessories, accounting for 98.87% of total revenue [1]

摩托车及其他板块10月24日涨1.86%,征和工业领涨,主力资金净流入9253.51万元

Zheng Xing Xing Ye Ri Bao· 2025-10-24 08:21

Market Overview - On October 24, the motorcycle and other sectors rose by 1.86%, with Zhenghe Industrial leading the gains [1] - The Shanghai Composite Index closed at 3950.31, up 0.71%, while the Shenzhen Component Index closed at 13289.18, up 2.02% [1] Stock Performance - Zhenghe Industrial (003033) closed at 71.51, up 3.65% with a trading volume of 26,200 shares and a turnover of 186 million [1] - Ninebot (60006899) closed at 65.47, up 3.61% with a trading volume of 156,800 shares and a turnover of 1.013 billion [1] - Jiangxi General (603766) closed at 13.46, up 2.36% with a trading volume of 206,500 shares and a turnover of 27.7 million [1] - Taotao Industry (301345) closed at 237.80, up 2.27% with a trading volume of 15,700 shares and a turnover of 36.9 million [1] - Other notable stocks include Yong'anxing (603776) at 19.47, up 2.15%, and Aima Technology (603529) at 33.18, up 1.84% [1] Capital Flow - The motorcycle and other sectors saw a net inflow of 92.5351 million in main funds, while retail funds experienced a net outflow of 44.7828 million [2] - The main funds' net inflow and outflow for key stocks include: - Ninebot: 14.44% net inflow from main funds, with a net outflow of 29.7736 million from retail funds [3] - Aima Technology: 8.85% net inflow from main funds, with a net outflow of 2.82074 million from retail funds [3] - Zhenghe Industrial: 10.47% net inflow from main funds, with a net outflow of 1.62597 million from retail funds [3]

春风动力(603129):2025年三季度利润小幅提升,全地形车、极核等引领高端化

Guoxin Securities· 2025-10-23 11:23

Investment Rating - The report maintains an "Outperform" rating for the company [7][5][38] Core Insights - The company achieved revenue of 14.1 billion yuan in Q1-Q3 2025, a year-on-year increase of 30.9%, driven by the motorcycle and all-terrain vehicle (ATV) segments, although profit growth has slowed due to tariff impacts [1][10] - The company is set to launch several new products in 2024, including high-performance models in the ATV and motorcycle segments, which are expected to enhance competitiveness and drive growth [3][24][27] - The electric two-wheeler segment, represented by the brand "Jike," is emerging as a new growth curve, with significant sales increases anticipated [35][36] Financial Performance - For Q1-Q3 2025, the company reported a gross margin of 27.6%, down 3.9 percentage points year-on-year, and a net margin of 10.0%, up 0.1 percentage points year-on-year [2][18] - The company forecasts net profits of 18.49 billion, 23.86 billion, and 28.61 billion yuan for 2025, 2026, and 2027 respectively, with corresponding earnings per share of 12.12, 15.64, and 18.75 yuan [5][38] Product Development - The company is actively expanding its motorcycle lineup with new models set to launch in 2024 and 2025, enhancing its market presence and competitiveness [4][27][29] - The introduction of the U10 PRO and U10 XL PRO models in the ATV segment is expected to significantly boost the company's market position in high-end products [24][25] Market Expansion - The company is focusing on expanding its export business, particularly in North America and Europe, leveraging its competitive pricing and product offerings [31][32] - The electric two-wheeler market is being targeted with a comprehensive product matrix aimed at various consumer segments, indicating a strategic shift towards electric mobility [35][36]

春风动力(603129):2025 年三季度利润小幅提升,全地形车、极核等引领高端化

Guoxin Securities· 2025-10-23 09:05

Investment Rating - The report maintains an "Outperform" rating for the company [7][5]. Core Insights - The company achieved revenue of 14.1 billion yuan in Q1-Q3 2025, a year-on-year increase of 30.9%, driven by the motorcycle and all-terrain vehicle (ATV) businesses, although profit growth has slowed due to tariff impacts [1][10]. - The gross margin for Q1-Q3 2025 was 27.6%, down 3.9 percentage points year-on-year, while the net margin was 10.0%, up 0.1 percentage points year-on-year [2][18]. - The company is set to launch several new products in 2024, including the U10 PRO and U10 XL PRO, which are expected to drive significant growth in the ATV segment [3][24]. Financial Performance - For Q3 2025, the company reported revenue of 50.4 billion yuan, a year-on-year increase of 28.6%, but a quarter-on-quarter decline of 10.1% [1][10]. - The net profit for Q3 2025 was 4.1 billion yuan, reflecting a year-on-year growth of 11.0% but a quarter-on-quarter decline of 29.5% [1][10]. - The company forecasts net profits of 18.49 billion yuan, 23.86 billion yuan, and 28.61 billion yuan for 2025, 2026, and 2027, respectively [5][38]. Product Development - The company is actively expanding its motorcycle lineup with new models such as the 150SC, 450MT, and 500SR VOOM, aiming to enhance competitiveness and market share [4][27]. - The electric motorcycle brand, Jike, is expected to become a significant growth driver, with plans to establish a production base in Zhejiang Province [35][36]. Market Expansion - The company is focusing on both domestic and international markets, with a renewed emphasis on exporting motorcycles, particularly to North America and Europe [31][32]. - The competitive pricing of its products, such as the 450SS, positions the company favorably against established competitors in overseas markets [32][34].

摩托车及其他板块10月23日涨0.41%,上海凤凰领涨,主力资金净流入591.22万元

Zheng Xing Xing Ye Ri Bao· 2025-10-23 08:20

Market Overview - The motorcycle and other sectors increased by 0.41% on October 23, with Shanghai Phoenix leading the gains [1] - The Shanghai Composite Index closed at 3922.41, up 0.22%, while the Shenzhen Component Index closed at 13025.45, also up 0.22% [1] Stock Performance - Shanghai Phoenix (600679) closed at 13.46, up 5.73% with a trading volume of 322,700 shares and a turnover of 440 million yuan [1] - Other notable performers include: - Zhonglu Co., Ltd. (600818) at 10.48, up 2.24% [1] - Qianjiang Motorcycle (000913) at 16.79, up 1.70% [1] - New Day Co., Ltd. (603787) at 12.68, up 1.52% [1] Capital Flow - The motorcycle and other sectors saw a net inflow of 5.91 million yuan from main funds, while retail investors experienced a net outflow of 51.65 million yuan [2] - The main funds' net inflow for Shanghai Phoenix was 51.16 million yuan, indicating strong institutional interest [3] Individual Stock Capital Flow - Key stocks and their capital flow include: - Shanghai Phoenix: Main funds net inflow of 51.16 million yuan, retail net outflow of 50.88 million yuan [3] - Longxin General (603766): Main funds net inflow of 27.58 million yuan, retail net outflow of 38.43 million yuan [3] - Ninebot Company (689009): Main funds net inflow of 8.41 million yuan, retail net outflow of 19.88 million yuan [3]

涛涛车业(301345):点评报告:单三季度业绩同比增长121%,北美休闲车龙头有望强者恒强

ZHESHANG SECURITIES· 2025-10-22 14:04

Investment Rating - The investment rating for the company is "Buy" [5] Core Views - The company reported a significant increase in profits, with a 121% year-on-year growth in net profit for the third quarter of 2025, and a 101% increase for the first three quarters [1] - The company aims to enhance its global strategy by issuing H shares and listing on the Hong Kong Stock Exchange, which is expected to improve its international brand influence and financing capabilities [1] - The demand for electric low-speed vehicles in North America is expected to grow due to changing consumer habits and the high costs associated with traditional vehicles [2] - The company is expanding its market share as inventory levels in the North American electric low-speed vehicle industry are projected to decline [2] - The company has launched new products, including the CITY panoramic camping vehicle priced at $15,500, and has established strategic partnerships with over 50 high-end dealers in North America [3] - The company is advancing its smart technology initiatives through collaborations with various tech firms to develop intelligent robots and autonomous vehicles [3] - Revenue projections for 2025-2027 indicate a growth trajectory with expected revenues of 4.2 billion, 5.7 billion, and 7.5 billion yuan, respectively, alongside substantial increases in net profit [3] Summary by Sections Financial Performance - For the first three quarters of 2025, the company achieved revenue of 2.77 billion yuan, a 25% increase year-on-year, and a net profit of 610 million yuan, a 101% increase [1] - The third quarter alone saw revenue of 1.06 billion yuan, up 28% year-on-year, and a net profit of 260 million yuan, up 121% [1] - The weighted ROE for the first three quarters was 18.1%, an increase of 8.0 percentage points year-on-year [1] Market Dynamics - The North American market for electric low-speed vehicles is experiencing a surge in demand, driven by lifestyle changes and the high costs of traditional vehicles [2] - The company is well-positioned to capture market share as industry inventory levels are expected to decrease [2] Product and Channel Development - The company has launched new products and expanded its dealer network significantly, with over 230 high-end golf cart dealers and more than 300 electric bicycle dealers in North America [3] - Strategic partnerships with leading dealers and flagship stores are enhancing the company's market presence [3] Future Outlook - Revenue forecasts for 2025-2027 suggest a compound annual growth rate of 47%, with net profits expected to grow significantly during this period [3]