普洛药业

Search documents

天宇股份的前世今生:2025年三季度营收22.87亿行业排第8,高于行业平均,净利润2.21亿行业排第11

Xin Lang Cai Jing· 2025-10-30 14:46

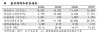

Core Viewpoint - Tianyu Co., Ltd. is a leading domestic pharmaceutical raw material enterprise, focusing on the research and production of pharmaceutical intermediates, raw materials, and formulations, with significant technical and cost advantages [1] Financial Performance - In Q3 2025, Tianyu's revenue reached 2.287 billion yuan, ranking 8th in the industry out of 47 companies, with the industry leader, Prolo Pharmaceutical, generating 7.764 billion yuan [2] - The net profit for the same period was 221 million yuan, placing Tianyu 11th in the industry, while the top performer, Zhejiang Pharmaceutical, reported 867 million yuan [2] Profitability and Debt Ratios - As of Q3 2025, Tianyu's debt-to-asset ratio was 43.32%, down from 45.02% year-on-year, which is higher than the industry average of 27.75% [3] - The gross profit margin for the same period was 39.14%, an increase from 35.47% year-on-year, surpassing the industry average of 35.38% [3] Executive Compensation - The chairman and general manager, Tu Yongjun, received a salary of 1.688 million yuan in 2024, an increase of 670,000 yuan from 2023 [4] Shareholder Information - As of September 30, 2025, the number of A-share shareholders decreased by 8.06% to 15,200, while the average number of shares held per shareholder increased by 8.76% to 13,900 [5] - Hong Kong Central Clearing Limited is the fifth-largest shareholder, holding 6.144 million shares, an increase of 2.7532 million shares from the previous period [5] Business Highlights - The company has seen high growth in non-sartan products, CDMO, and formulations, with continuous improvement in profitability [5] - In H1 2025, revenue from the generic drug raw materials and intermediates business, particularly for blood sugar-lowering and anti-asthma products, grew rapidly [6] - The CDMO business benefited from expanded customer demand, while the formulation business saw improvements due to product structure optimization and marketing channel development [6]

尔康制药的前世今生:2025年三季度营收10.06亿低于行业平均,净利润2711.07万排名靠后

Xin Lang Cai Jing· 2025-10-30 13:57

Core Viewpoint - Erkang Pharmaceutical is a leading enterprise in the pharmaceutical excipients industry in China, with a comprehensive industry chain advantage and strong product quality and market share [1] Group 1: Business Performance - In Q3 2025, Erkang Pharmaceutical reported a revenue of 1.006 billion yuan, ranking 18th among 47 companies in the industry, significantly lower than the top company, Puluo Pharmaceutical, which had a revenue of 7.764 billion yuan [2] - The main business composition includes pharmaceutical excipients, which accounted for 246 million yuan, representing 36.29% of total revenue [2] - The net profit for the same period was 27.11 million yuan, ranking 32nd in the industry, and was substantially lower than the leading company, Zhejiang Pharmaceutical, which reported a net profit of 867 million yuan [2] Group 2: Financial Ratios - As of Q3 2025, the debt-to-asset ratio for Erkang Pharmaceutical was 15.20%, an increase from 12.90% in the previous year, and lower than the industry average of 27.75%, indicating strong solvency [3] - The gross profit margin for Q3 2025 was 27.37%, down from 30.94% year-on-year, and below the industry average of 35.38%, suggesting a need for improvement in profitability [3] Group 3: Shareholder Information - As of September 30, 2025, the number of A-share shareholders increased by 14.88% to 49,100, while the average number of circulating A-shares held per shareholder decreased by 12.95% to 29,000 [5] - Among the top ten circulating shareholders, Hong Kong Central Clearing Limited ranked as the fifth largest, holding 25.8786 million shares, an increase of 4.3188 million shares from the previous period [5] Group 4: Executive Compensation - The chairman, Shuai Fangwen, received a salary of 512,900 yuan in 2024, a slight increase from 512,600 yuan in 2023 [4] - The general manager, Sun Qingrong, saw a significant salary increase to 1.0148 million yuan in 2024 from 335,700 yuan in 2023, reflecting a rise of 679,100 yuan [4]

大成基金徐彦争议产品完成建仓,权益仓位仅够“最低线”, 再次谈及“建仓难”

Mei Ri Jing Ji Xin Wen· 2025-10-29 06:29

Core Viewpoint - Dachen Fund's chief equity investment officer Xu Yan has completed the stock positioning for the Dachen Xingyuan Qihang mixed fund in the third quarter, despite previous controversies regarding the slow pace of building positions [1][2] Group 1: Fund Positioning and Strategy - The Dachen Xingyuan Qihang fund has a stock asset allocation of 60.89%, just meeting the minimum requirement for equity mixed funds [1][2] - Xu Yan maintains a cautious approach to stock selection, focusing on companies with a high margin of safety, and has a consistent heavy allocation in stocks like Kanghong Pharmaceutical and China National Offshore Oil Corporation [1][2] - The fund has not invested in bond assets due to the current challenging bond market environment, instead allocating 33.23% to bank deposits and settlement reserves [2] Group 2: Fund Performance and Management - Xu Yan's management scale has grown, with a total of 21.462 billion yuan across eight funds, marking a continuous increase for three consecutive quarters [3] - All eight funds under Xu Yan's management saw growth in scale during the third quarter, with the Dachen Competitive Advantage fund experiencing a significant increase of 41.25 billion yuan [3] - Despite the growth in fund size, the performance of Xu Yan's funds in the third quarter was not outstanding, with none achieving the median performance of 23.17% for similar funds [3][4] Group 3: Long-term Performance - Over the past three years, Xu Yan's long-term performance has been impressive, achieving a return of 46.98%, which exceeds the return of the CSI 300 index by more than 10 percentage points [4]

司美格鲁肽原料药需求旺盛 圣诺生物前三季净利同比增123%

Mei Ri Jing Ji Xin Wen· 2025-10-28 12:30

Core Insights - The company, Shengnuo Biopharmaceuticals, reported significant growth in revenue and net profit for the first three quarters of 2025, primarily driven by increased overseas sales of GLP-1 class drugs, Semaglutide and Tirzepatide [1][2] - The company achieved a revenue of 520 million yuan, a year-on-year increase of 53.96%, and a net profit of 127 million yuan, reflecting a 123.03% increase [1] - The raw material drug business has become a major performance support for the company, with raw material revenue in the first half of the year reaching 189 million yuan, a 232.3% increase, accounting for approximately 55.92% of total revenue [1] Company Developments - Shengnuo Biopharmaceuticals is expanding its production capacity through various projects, including a new production line for peptide raw materials and technological upgrades for formulation industrialization [2] - The company’s raw materials are primarily sold overseas, and the expiration of patents for popular peptide drugs like Semaglutide in 2026 is expected to accelerate the penetration of generic drugs, leading to increased demand for peptide raw materials [2] Industry Context - The competition in the GLP-1 raw material drug market is intensifying, with several domestic companies such as Pro Pharmaceutical, Nuotai Biotech, and Hanyu Pharmaceutical also involved [2] - The market for oral peptide formulations is anticipated to drive higher demand for raw materials, presenting new growth opportunities for companies that strategically invest in this area [2] - The original manufacturer of Semaglutide, Novo Nordisk, has lowered its annual performance guidance, raising questions about the sustainability of the current market dynamics [2]

普洛药业:公司产品拟中选第十一批全国药品集中采购

Zheng Quan Shi Bao Wang· 2025-10-28 10:57

Core Viewpoint - Pro Pharmaceutical (000739) announced that its subsidiary, Zhejiang Pro Kangyu Pharmaceutical Co., Ltd., has participated in the 11th national centralized drug procurement organized by the National Organization for Drug Procurement Office, with its product, injection adenosine methionine bisulfate, expected to be selected for this procurement [1] Group 1 - The selected product is anticipated to obtain the Drug Registration Certificate in November 2024, which is equivalent to passing the consistency evaluation of generic drug quality and efficacy [1]

普洛药业(000739) - 关于公司产品拟中选第十一批全国药品集中采购的公告

2025-10-28 10:52

普洛药业股份有限公司 关于公司产品拟中选第十一批全国药品集中采购的公告 证券代码:000739 证券简称:普洛药业 公告编号:2025-58 | 产品名称 | 适应症 | 中选规格 | 拟中选价 | 拟中选数量 | 拟供地区 | 采购 | | --- | --- | --- | --- | --- | --- | --- | | | | | 格(元/支) | (万支) | | 周期 | | 注射用丁 | 适用于肝硬化前和肝硬 | 0.5g(以 | 6.82 | 123.7594 | 福建、广 | 3 年 | | 二磺酸腺 | 化所致肝内胆汁淤积。 | 腺苷蛋氨 | | | 西、湖南、 | | | 苷蛋氨酸 | 适用于妊娠期肝内胆汁 | 酸计) | | | 云南、海 | | | | 淤积。 | | | | 南 | | 1.上述品种的拟中选价格及拟中选数量均以联合采购办公室发布的最终数 据为准。 2. 按照相关规定,本次拟中选产品的采购周期自中选结果执行之日起至 2028 年 12 月 31 日。 二、对公司的影响 本公司及董事会全体成员保证信息披露的内容真实、准确、完整,没有虚假 记载、误导性陈述或重大遗漏。 ...

普洛药业:公司产品注射用丁二磺酸腺苷蛋氨酸拟中选本次集中采购

Mei Ri Jing Ji Xin Wen· 2025-10-28 10:51

Group 1 - Prolo Pharmaceutical's subsidiary, Zhejiang Prolo Kangyu Pharmaceutical Co., Ltd., participated in the 11th national centralized drug procurement organized by the National Organization for Drug Procurement Office, with its product, injection adenosine methionine bisulfate, expected to be selected for this procurement [1] - For the first half of 2025, Prolo Pharmaceutical's revenue composition is projected to be 99.6% from the pharmaceutical industry and 0.4% from other businesses [1] - As of the report date, Prolo Pharmaceutical has a market capitalization of 17.9 billion yuan [1]

普洛药业:公司产品注射用丁二磺酸腺苷蛋氨酸拟中选第十一批全国药品集中采购

Mei Ri Jing Ji Xin Wen· 2025-10-28 10:48

Core Viewpoint - Pro Pharmaceutical (000739) announced that its subsidiary Zhejiang Pro Kangyu Pharmaceutical Co., Ltd. participated in the 11th batch of national centralized drug procurement, with its product, injection adenosine methionine bisulfate, expected to be selected [1] Group 1: Product and Market Impact - The selected product is indicated for conditions such as pre-cirrhosis and intrahepatic cholestasis due to cirrhosis, as well as intrahepatic cholestasis during pregnancy [1] - If the company signs the procurement contract and implements it, it will help expand the sales scale of the related product and increase market share [1] - The potential selection of the product is expected to have a positive impact on the company's future operating performance [1] Group 2: Uncertainty and Future Steps - The procurement contract for the selected product has not yet been signed, indicating uncertainty in subsequent matters [1]

【太平洋医药|点评】普洛药业 :Q3业绩底部已现,看好CDMO业务持续兑现

Xin Lang Cai Jing· 2025-10-27 13:29

Core Viewpoint - The company reported a decline in revenue and profit for the first three quarters of 2025, indicating pressure on profitability and a challenging market environment [1][2]. Financial Performance - For Q1-3 2025, the company achieved revenue of 7.764 billion yuan, a year-over-year decrease of 16.43%, and a net profit attributable to shareholders of 700 million yuan, down 19.48% year-over-year [1][2]. - In Q3 2025, revenue was 2.319 billion yuan, a decline of 18.94% year-over-year, with a net profit of 137 million yuan, down 43.95% year-over-year [2]. - The gross margin for Q1-3 2025 was 25.02%, an increase of 0.79 percentage points year-over-year, while the net margin was 9.02%, a decrease of 0.34 percentage points year-over-year [2]. Business Segments - The API business generated sales of 5.19 billion yuan, down over 20% year-over-year, primarily due to weak demand for antibiotics and a strategic contraction in trading activities [3]. - The CDMO business saw significant growth, with sales of 1.69 billion yuan, a nearly 20% increase year-over-year, and a gross margin of 44.4%, contributing nearly 40% to the overall gross profit [3]. - The company has a backlog of orders worth 5.2 billion yuan for the next 2-3 years, mainly from commercial orders and secondary supply transitions to commercial production [3]. Stock Buyback - The company announced a share buyback plan of 75 to 150 million yuan to support employee stock ownership plans, with a maximum buyback price of 22 yuan per share [3]. Future Outlook - The company is expected to see a gradual improvement in net profit margins from 2026 to 2027, with projected revenues of 10.332 billion yuan, 11.194 billion yuan, and 12.504 billion yuan for 2025, 2026, and 2027 respectively [4]. - The net profit forecast for the same years is 910 million yuan, 1.097 billion yuan, and 1.375 billion yuan, corresponding to a PE ratio of 20, 17, and 14 times [4].

公募最新调研路径曝光医药和科技板块备受青睐

Shang Hai Zheng Quan Bao· 2025-10-26 15:37

Group 1 - Public funds have shown strong interest in the pharmaceutical and technology sectors, with over 160 public institutions conducting more than 2000 company surveys in the past month [2][3] - The pharmaceutical and electronics sectors received the highest attention, with the pharmaceutical industry being surveyed 85 times, making it the most focused area for institutions [2][3] - Companies such as Meihua Medical, Prologis Pharmaceutical, and Weili Medical were the most frequently surveyed, receiving 19, 18, and 17 surveys respectively [2] Group 2 - The power equipment and electronics sectors followed closely, with survey frequencies of 68 and 54 times respectively [3] - Analysts believe that the hardware innovation driven by AI is expected to yield substantial results soon, benefiting high-value industries [3] - The investment cycle in the artificial intelligence sector is likely to last 3 to 5 years, currently at a critical stage of industry implementation and performance realization [3] Group 3 - The innovative drug sector has experienced a phase of correction due to previous high gains, but opportunities are expected to arise in the fourth quarter as many Chinese innovative drug companies continue to expand their business [4] - The Chinese innovative drug industry has shown significant progress in the past three years, with improved pipelines and global competitiveness, entering an upward cycle [4] - The potential for commercialization of Chinese innovative drugs is strengthening, with opportunities for low-cost investments as the industry matures [4]