碳化硅外延晶片

Search documents

东兴证券晨报-20260330

Dongxing Securities· 2026-03-30 08:09

Core Insights - The report highlights the significant growth potential in the magnesium alloy industry, driven by increasing demand in high-end applications such as electric vehicles and robotics, with a projected CAGR of 29% from 2025 to 2028 [7][10][12] - The report also emphasizes the favorable price dynamics of magnesium compared to aluminum, with the magnesium-aluminum price ratio dropping to a five-year low of 0.66, indicating a 74% decline since 2021 [8][12] - The demand for magnesium alloys is expected to expand significantly across various sectors, including automotive, robotics, construction, and hydrogen storage, with specific forecasts indicating a rise in global magnesium alloy demand from 650,000 tons in 2025 to 1.39 million tons by 2028 [9][10][12] Company Insights - Hantian Technology, a silicon carbide wafer provider, recently went public in Hong Kong, with its stock price surging over 42% on the first day, achieving a market capitalization exceeding HKD 46.2 billion, marking the largest IPO in Xiamen this year [4] - Jiangfeng Electronics reported a revenue of CNY 4.605 billion for 2025, reflecting a year-on-year growth of 27.75%, with net profit increasing by 20.15% to CNY 481 million, driven by rising demand in the semiconductor sector [15][16] - Tesla's TERAFAB project aims to produce over 1 terawatt of computing power annually, indicating a significant increase in demand for high-performance chips as the humanoid robot industry scales up [4] Industry Insights - The report discusses the ongoing transformation in the financial sector, with the People's Bank of China emphasizing the importance of financial stability and risk management, which is crucial for maintaining overall economic health [6] - The logistics and express delivery industry is experiencing a shift towards quality over quantity, with major players like SF Express showing significant growth in revenue per package, indicating a positive trend in pricing strategies amid a competitive landscape [21] - The semiconductor materials market is expected to see a significant increase in demand, with projections indicating that the global sputtering target market could exceed CNY 25.11 billion by 2027, driven by rising production in the semiconductor industry [17][18]

瀚天天成(02726):IPO点评

国投证券(香港)· 2026-03-24 08:36

Investment Rating - The report assigns an IPO-specific rating of 4.9 out of 10 for the company, based on operational performance, industry outlook, valuation, and market sentiment [7]. Core Insights - The company is a global leader in the silicon carbide (SiC) epitaxy industry, focusing on the research, production, and sales of SiC epitaxial wafers, which are used in power device manufacturing for sectors such as electric vehicles, charging infrastructure, renewable energy, and energy storage [1]. - The company is expected to maintain profitability from 2022 to 2024, with net profits of 128 million, 108 million, and 165 million respectively, although revenue is projected to decline in 2024 and 2025 due to industry destocking and weakening downstream demand [1]. - The global SiC power device market is projected to reach $2.6 billion in 2024, with a compound annual growth rate (CAGR) of 39.9% from 2024 to 2029, reaching $13.6 billion by 2029 [2]. Company Overview - The company serves 134 clients, with four of the top five global SiC power device manufacturers among its customers, indicating a strong market position [1]. - The company employs a dual model of epitaxial wafer sales and wafer foundry services, with wafer sales being the primary revenue source [1]. - The company has delivered over 599,700 SiC epitaxial wafers and is the first globally to mass-produce 8-inch products, with plans to launch 12-inch wafers by December 2025 [3]. Financial Performance - Revenue figures for 2022, 2023, 2024, and the first nine months of 2025 are projected at 441 million, 1.14 billion, 974 million, and 535 million respectively, indicating a peak in 2023 followed by a decline [1]. - The gross margin is expected to decrease, with the first nine months of 2025 projected at 25.6% [4]. Market Conditions - The semiconductor industry is currently in a cyclical inventory adjustment phase, which is expected to conclude in the second half of 2026, leading to a recovery in demand and pricing [2]. - The company is well-positioned to benefit from the recovery in demand for power semiconductors and the trend towards domestic production in the renewable energy sector [11]. Use of Proceeds - The company plans to use the net proceeds from the IPO, estimated at 1.56 billion HKD, for expanding SiC epitaxial wafer production capacity (71%), R&D investments (19%), and general corporate purposes (10%) [10].

IPO点评:瀚天天成

国投证券(香港)· 2026-03-24 08:24

Investment Rating - The report assigns an IPO-specific rating of 4.9 out of 10 for the company, based on operational performance, industry outlook, valuation, and market sentiment [7]. Core Insights - The company is a global leader in the silicon carbide epitaxy industry, focusing on the research, production, and sales of silicon carbide epitaxial wafers, which are used in power device manufacturing for sectors such as electric vehicles, charging infrastructure, renewable energy, and energy storage [1]. - The company is expected to maintain its position as the largest supplier of silicon carbide epitaxial wafers, with a projected market share exceeding 30% in 2024 [1]. - Financial projections indicate a peak in revenue in 2023, followed by a decline in 2024 and 2025 due to industry destocking, price reductions, and weakened downstream demand [1][2]. Company Overview - The company serves 134 clients, including four of the top five global silicon carbide power device manufacturers [1]. - Revenue figures for 2022-2024 are projected at 4.41 billion, 11.4 billion, and 9.74 billion, respectively, with a net profit of 1.28 billion, 1.08 billion, and 1.65 billion for the same years [1]. - The company employs a dual model of epitaxial wafer sales and wafer foundry services, with wafer sales being the primary revenue source [1]. Industry Status and Outlook - The global silicon carbide power device market is expected to reach $2.6 billion in 2024, with a compound annual growth rate (CAGR) of 39.9% from 2024 to 2029, potentially reaching $13.6 billion by 2029 [2]. - The semiconductor industry is currently undergoing an inventory adjustment cycle, which is expected to conclude in the second half of 2026, indicating a cyclical rather than structural downturn [2]. Strengths and Opportunities - The company has significant technical barriers, with its founder being the first IEEE fellow in the silicon carbide field and over 35 years of research experience [3]. - The company has achieved a leading market position, being the first globally to mass-produce 8-inch products and planning to launch 12-inch silicon carbide epitaxial wafers by December 2025 [3]. - The end of the inventory cycle in 2026 is anticipated to lead to a recovery in demand, benefiting from new applications in home appliances, AI computing, and energy storage [3]. Weaknesses and Risks - Revenue is projected to decline by 14.7% in 2024 compared to 2023, with a continued decrease in gross margin expected [4]. - The company has a high customer concentration, with over 60% of revenue coming from its top five clients [4]. - There are risks associated with industry competition and potential prolonged inventory adjustments, which could impact profitability [4]. IPO Information - The IPO is scheduled from March 20 to March 25, 2026, with a share price set at HKD 76.26, and trading is expected to commence on March 30, 2026 [5]. - The company aims to raise approximately HKD 15.6 billion, with 71% allocated to expanding production capacity for silicon carbide epitaxial wafers [10]. Investment Recommendation - The company is positioned as a dominant player in the silicon carbide epitaxy market, with strong technical and customer advantages, and is expected to benefit from trends in renewable energy and domestic semiconductor production [11]. - The IPO price corresponds to a market capitalization of HKD 32.455 billion, with a price-to-sales ratio of approximately 41.2x, suggesting a cautious approach to subscription [11].

新股预览:瀚天天成

中国光大证券国际· 2026-03-20 06:24

Investment Rating - The investment rating for the company is set at ★★★★☆ for basic factors and valuation, ★★★★☆ for performance growth, ★★★☆☆ for industry representation, ★★★☆☆ for industry prosperity, and ★★★★☆ for market conditions [4]. Core Insights - The company is a global leader in the silicon carbide (SiC) epitaxy industry, being the largest supplier by sales volume since 2023, with a market share exceeding 30% in 2024 [1][3]. - The industry is experiencing rapid growth driven by the global energy revolution, where silicon carbide is becoming the mainstream material for power semiconductor devices due to its superior properties [2]. - The company has a strong technical foundation and a comprehensive product portfolio, having developed advanced SiC epitaxy growth technology over 14 years, which allows for high-quality and reliable product offerings [2]. Financial Summary - Revenue for the fiscal year ending December 31 is projected to be 4.41 billion RMB in 2022, increasing to 11.43 billion RMB in 2023, and then decreasing to 9.74 billion RMB in 2024 [4]. - The net profit for the same periods is expected to be 1.28 billion RMB in 2022, 1.08 billion RMB in 2023, and 1.65 billion RMB in 2024 [4]. Offering Details - The company plans to issue 0.21 billion shares, with 0.02 billion shares allocated for the Hong Kong offering and 0.19 billion for the international offering [5]. - The offering price is set at 76.26 HKD per share, with a maximum fundraising amount of 16.39 billion HKD [5]. - The subscription period is from March 20 to March 25, with the listing date on March 30 [5].

瀚天天成(02726) - 全球发售

2026-03-19 22:14

瀚天天成電子科技(廈門)股份有限公司 Epiworld International Co., Ltd. (於中華人民共和國註冊成立的股份有限公司) 股份代號 : 2726 全球發售 獨家保薦人、保薦人兼整體協調人、整體協調人、 聯席全球協調人、聯席賬簿管理人及聯席牽頭經辦人 整體協調人、聯席全球協調人、 聯席賬簿管理人及聯席牽頭經辦人 聯席全球協調人、聯席賬簿管理人及聯席牽頭經辦人 聯席賬簿管理人及聯席牽頭經辦人 重要提示 重要提示:如 閣下對本招股章程任何內容有任何疑問,應徵詢獨立專業意見。 Epiworld International Co., Ltd. 瀚天天成電子科技(廈門)股份有限公司 (於中華人民共和國註冊成立的股份有限公司) 全球發售 足,多繳股款可予退還) 獨家保薦人、保薦人兼整體協調人、整體協調人、 聯席全球協調人、聯席賬簿管理人及聯席牽頭經辦人 整體協調人、聯席全球協調人、聯席賬簿管理人及聯席牽頭經辦人 聯席全球協調人、聯席賬簿管理人及聯席牽頭經辦人 聯席賬簿管理人及聯席牽頭經辦人 香港交易及結算所有限公司、香港聯合交易所有限公司及香港中央結算有限公司對本招股章程的內容概不負責,對其準確性 ...

瀚天天成电子科技(厦门)股份有限公司(H0085) - 聆讯后资料集(第一次呈交)

2026-03-11 16:00

香港交易及結算所有限公司、香港聯合交易所有限公司與證券及期貨事務監察委員會對本聆訊後資料集的 內容概不負責,對其準確性或完整性亦不發表任何意見,並明確表示概不就因本聆訊後資料集全部或任何 部分內容而產生或因倚賴該等內容而引致的任何損失承擔任何責任。 Epiworld International Co., Ltd. 瀚天天成电子科技(厦门)股份有限公司 (「本公司」) (於中華人民共和國註冊成立的股份有限公司) 的聆訊後資料集 警告 本聆訊後資料集乃根據香港聯合交易所有限公司(「聯交所」)及證券及期貨事務監察委員會(「證 監會」)的要求而刊發,僅用作提供資料予香港公眾人士。 本聆訊後資料集為草擬本,其內所載資料並不完整,亦可能會作出重大變動。 閣下閱覽本文件, 即代表 閣下知悉、接納並向本公司、本公司的保薦人、整體協調人、顧問或承銷團成員表示同 意: 本公司招股章程根據香港法例第32章《公司(清盤及雜項條文)條例》送呈香港公司註冊處處長 登記前,本公司不會向香港公眾人士提出要約或邀請。倘在適當時候向香港公眾人士提出要約 或邀請,有意投資者務請僅依據於香港公司註冊處處長註冊的本公司招股章程作出投資決定, 招股章程 ...

华为加持!国内SiC厂商冲击港股IPO

Sou Hu Cai Jing· 2026-02-09 07:48

Core Viewpoint - Hantian Technology (Xiamen) Co., Ltd. has completed the key regulatory procedures for its overseas listing in Hong Kong, marking a significant step towards its IPO process on the Hong Kong Stock Exchange [1]. Company Overview - Founded in 2011 by Dr. Zhao Jianhui, Hantian Technology specializes in the research, production, and sales of silicon carbide (SiC) epitaxial wafers, being the first in China to commercialize full-size (3/4/6/8 inches) SiC epitaxial wafers [2][3]. - The company’s products are widely used in strategic emerging fields such as new energy vehicles, photovoltaic energy storage, industrial power supplies, and rail transportation, catering to high-end application needs [3]. Shareholder Structure - Hantian Technology plans to issue no more than 37.68 million overseas listed ordinary shares, while 39 shareholders intend to convert a total of 97.43 million domestic unlisted shares into overseas listed shares [3]. - The founder, Dr. Zhao Jianhui, holds a 28.85% stake, making him the controlling shareholder, while Huawei's Hubble Technology holds 4.03%, ranking as the fifth-largest shareholder [3]. Recent Developments - The company has been actively expanding its production capacity and enhancing its technology, laying a solid foundation for its upcoming IPO [5]. - In December 2025, Hantian Technology launched the world's first 12-inch silicon carbide epitaxial wafer, achieving a thickness non-uniformity of ≤3% and a doping concentration non-uniformity of ≤8%, with a yield rate exceeding 96% for 2mm×2mm chips [5]. Industry Context - The move towards an IPO by Hantian Technology reflects the current trend in the silicon carbide epitaxial and third-generation semiconductor industries, driven by explosive growth in downstream markets such as new energy vehicles and photovoltaic energy storage [6]. - The global silicon carbide epitaxial industry is expected to trend towards larger sizes, domestic production, collaboration, and high-end applications, with 8-inch and 12-inch wafers becoming mainstream [9]. - Successful listing will provide Hantian Technology with substantial fundraising support to accelerate its 8-inch capacity expansion and 12-inch technology development, contributing to the advancement of domestic silicon carbide epitaxial technology and capacity [9].

66岁厦大博士,创业15年二闯IPO

3 6 Ke· 2025-10-21 00:19

Core Insights - Hantian Technology has submitted a listing application to the Hong Kong Stock Exchange after previously attempting to list on the Sci-Tech Innovation Board without success [1] - The company is the largest supplier of silicon carbide epitaxial wafers globally, holding over 30% market share in 2024 and leading in shipment volumes for two consecutive years [1][2] - Hantian Technology's products are widely used in electric vehicles, renewable energy, and smart appliances, among other applications [2] Financial Performance - Revenue figures from 2022 to May 2025 show significant fluctuations, with revenues of 440 million, 1.143 billion, 974 million, and 266 million yuan respectively [2] - Net profits during the same period were 143 million, 122 million, 166 million, and 14 million yuan, indicating a strong correlation with market demand and competitive pressures [2][3] Market Challenges - The company faces increased competition and price wars due to domestic capacity expansion in silicon carbide epitaxial wafers, leading to a decline in its foundry business, which constituted nearly one-third of its operations [3] - The sales contribution of 6-inch silicon carbide epitaxial wafers remains high at 94.8%, while the 8-inch wafers have seen a rise to 4.9% [3] Technological Leadership - Hantian Technology is recognized for being the first to achieve mass production of 8-inch silicon carbide epitaxial wafers and has developed various sizes for commercial supply [2][4] - The company’s founder, Zhao Jianhui, has over 35 years of experience in silicon carbide technology and has led significant advancements in the field [4][5] Investment and Partnerships - The company has received substantial support from Xiamen state-owned assets, with multiple rounds of investment totaling 1.03 billion yuan for expansion and production upgrades [5] - Hantian Technology has established partnerships with 18 global enterprises for 8-inch products, aiming for an annual production capacity of 463,000 wafers by 2029 [6]

瀚天天成加码投入备战8英寸外延片竞赛,全球龙头新布局能否扭转业绩?

Zhi Tong Cai Jing· 2025-10-15 13:24

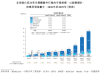

Industry Overview - The silicon carbide (SiC) market is rapidly expanding due to growth in sectors such as electric vehicles, photovoltaic energy storage, data centers, and AR glasses. The global sales of SiC power semiconductor devices are projected to reach $2.6 billion in 2024, with a compound annual growth rate (CAGR) of 45.4% from 2020 to 2024. By 2029, the market size is expected to increase to $13.6 billion, with the penetration rate in the global power semiconductor market rising from 4.9% in 2024 to 17.1% in 2029 [1][4]. Company Performance - Hantian Technology (Xiamen) Co., Ltd. is a leading player in the global SiC epitaxy industry, holding a significant market position. In 2024, the company is expected to capture 31.6% of the global sales volume and 29.2% of the revenue, both ranking first globally. Hantian Technology has been at the forefront of industry innovation, being the first in China to achieve commercial production of 3-inch, 4-inch, 6-inch, and 8-inch SiC epitaxy wafers [6][7]. Revenue Trends - Hantian Technology's revenue has shown volatility, with total revenues of 441 million yuan in 2022, 1.143 billion yuan in 2023, and a projected 974 million yuan in 2024. The revenue structure indicates that sales of epitaxy wafers have consistently been the largest source of income, increasing from 63% in 2022 to 86.4% in 2024. Conversely, the contribution from epitaxy wafer foundry services has declined significantly [7][10]. Market Dynamics - The price of SiC epitaxy wafers has been on a downward trend due to reduced raw material costs and technological advancements. For instance, the average price of 6-inch SiC epitaxy wafers is expected to drop from 11,400 yuan in 2020 to approximately 4,400 yuan by 2029, indicating a potential decline of nearly 40% [11][12]. Strategic Initiatives - To ensure sustained growth, Hantian Technology is focusing on technological innovation and scaling up production to reduce costs. The company has made significant progress in 8-inch SiC epitaxy technology, which is anticipated to enhance production efficiency and lower unit costs. By expanding the production of 8-inch wafers, Hantian Technology aims to capture a larger market share and improve profitability [12][13].

新股前瞻|瀚天天成加码投入备战8英寸外延片竞赛,全球龙头新布局能否扭转业绩?

智通财经网· 2025-10-15 13:19

Industry Overview - The silicon carbide (SiC) market is rapidly expanding due to growth in sectors such as electric vehicles, photovoltaic energy storage, data centers, and AR glasses. The global sales of SiC power semiconductor devices are projected to reach $2.6 billion in 2024, with a compound annual growth rate (CAGR) of 45.4% from 2020 to 2024. By 2029, the market size is expected to grow to $13.6 billion, increasing the penetration rate from 4.9% in 2024 to 17.1% in 2029 [1][4]. Company Performance - Hantian Technology (Xiamen) Co., Ltd. is a leading player in the global SiC epitaxy industry, holding a significant market share of 31.6% in sales and 29.2% in revenue in 2024. The company has established itself as a pioneer in the commercialization of various sizes of SiC epitaxial wafers [6][7]. - The company's revenue has shown volatility, with total revenues of 441 million yuan in 2022, 1.143 billion yuan in 2023, and a decline to 974 million yuan in 2024. The revenue from epitaxial wafer sales has consistently increased, accounting for 86.4% of total revenue in 2024 [7][10]. Market Dynamics - The SiC epitaxial wafer market is expected to grow from $1.2 billion in 2024 to $5.8 billion by 2029, with a CAGR of 38.2%. The quality of SiC epitaxial wafers is crucial, as they represent about 25% of the value chain of SiC power devices [4]. - The average price of 6-inch SiC epitaxial wafers has been declining, projected to drop from 7,300 yuan in 2024 to 4,400 yuan by 2029, indicating a potential decrease of nearly 40% [11]. Strategic Initiatives - Hantian Technology is focusing on technological innovation and scaling up production to maintain its competitive edge. The company has successfully developed 8-inch SiC epitaxial wafer technology and established partnerships with 18 companies for mass supply [12][13]. - The sales of 8-inch SiC epitaxial wafers are expected to increase significantly, from 285 units in 2023 to 7,466 units in 2024, with 2,914 units sold in the first five months of 2025, reflecting a substantial growth trajectory [13].