存内计算

Search documents

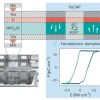

温控新技术显著提升AI核心硬件性能

Ke Ji Ri Bao· 2026-02-25 23:02

Core Insights - Scientists from Sungkyunkwan University have developed a new technology that utilizes heat to precisely control the internal structure of semiconductors, significantly enhancing the performance of next-generation AI core hardware, enabling complex AI computations to be processed faster with lower power consumption [1][2] Group 1: Technology Development - The current architecture of computers separates processors and memory, leading to inefficiencies as data must be transferred back and forth, akin to students moving between a desk and a bookshelf [1] - The proposed solution, "in-memory computing," allows computations to be performed directly within the memory, focusing on the use of ferroelectric transistors [1] - The key challenge in manufacturing these transistors lies in the material hafnium oxide, which requires specific atomic arrangements to maintain storage functionality [1] Group 2: Innovative Approach - Previous methods to address the challenges involved doping with other chemical elements, which are complex and not suitable for mass production [1] - The research team employed the principle of thermal expansion, where different materials expand and contract at varying rates when heated, to overcome these challenges [2] Group 3: Performance and Applications - The team designed electrodes around the semiconductor material that apply compressive stress to the hafnium oxide during cooling, effectively "shaping" the atoms into an optimal crystalline structure for storage operations [2] - Tests indicate that the newly designed semiconductor devices remain stable after over one trillion operations and achieve an accuracy rate of 97.2% in AI image recognition tasks [2] - The results suggest that high-performance AI semiconductor devices can be achieved without complex chemical processes, relying solely on temperature control, which could lead to smarter and more efficient AI technologies in applications like autonomous vehicles and smartphones if commercialized [2]

从去库存寒冬到AI新战场,芯天下叩响港交所大门

Zhi Tong Cai Jing· 2026-01-13 11:00

Core Viewpoint - The company, Xintianxia Technology Co., Ltd., is preparing for an IPO on the Hong Kong Stock Exchange, aiming to leverage the growing demand for code flash memory chips amid the dual trends of domestic substitution and AI application explosion [1]. Group 1: Company Overview - Xintianxia, founded in 2014, specializes in the research, design, and sales of code flash memory chips, including NOR Flash and SLC NAND Flash, and ranks sixth among global fabless companies in this sector as of 2024 [1][2]. - The company has a strong market position, holding a 3.7% share in the global code flash memory chip market and 6.6% in the SLC NAND Flash segment [3]. Group 2: Financial Performance - The company's revenue was 663 million RMB in 2023, dropping to 442 million RMB in 2024, with consecutive net losses due to strategic pricing adjustments and industry-wide inventory destocking [2]. - By the end of September 2025, the company reported a revenue of 379 million RMB, a 10% increase year-on-year, and achieved profitability with a net profit of 8.4 million RMB [2]. Group 3: Product and Market Strategy - Xintianxia's core revenue comes from SLC NAND Flash and NOR Flash, contributing approximately 48.8% and 36.0% of revenue, respectively, in 2024 [2]. - The company has made significant advancements in high-performance storage, successfully producing a 2Gbit SPI NOR Flash using ETOX 55nm technology, breaking the monopoly of foreign companies in high-end applications [3]. Group 4: Strategic Initiatives - The company is adopting a "Storage + AI" strategy to enhance efficiency in edge computing, targeting the growing demand for high-performance storage chips driven by AI applications [4]. - Xintianxia is expanding its product lines to include analog chips and MCUs, providing comprehensive chip solutions that integrate power supply, control, storage, and drive functions [5]. - The company is also developing in-memory computing (CIM) acceleration chips based on ReRAM technology, aiming for production by the end of 2026, targeting low-power edge AI applications [5]. Group 5: Future Outlook - The global code flash memory chip market is projected to grow from $4.9 billion in 2024 to $8.3 billion by 2030, with China expected to account for over 55% of this market [4]. - The company aims to enhance its global brand recognition and expand its technological moat through its upcoming IPO, focusing on advanced manufacturing processes and strategic partnerships in Japan, Europe, and North America [6].

新股前瞻 | 从去库存寒冬到AI新战场,芯天下叩响港交所大门

智通财经网· 2026-01-13 10:02

Core Viewpoint - The company, Xintianxia Technology Co., Ltd., is preparing for an IPO on the Hong Kong Stock Exchange, aiming to leverage capital market support to transition from an innovator to a leader in the semiconductor industry, particularly in code flash memory and AI applications [1]. Group 1: Company Overview - Xintianxia was established in 2014 and focuses on the research, design, and sales of code flash memory chips, including NOR Flash and SLC NAND Flash, serving various sectors such as telecommunications, consumer electronics, industrial medical, and automotive electronics [1]. - As of 2024, Xintianxia ranks sixth among global fabless companies in code flash memory, and fourth and fifth in the SLC NAND Flash and NOR Flash segments, respectively [1]. Group 2: Financial Performance - The company's revenue was 663 million RMB in 2023, dropping to 442 million RMB in 2024, with consecutive net losses due to a temporary operational lag and strategic pricing adjustments [2]. - By the end of September 2025, the company reported a revenue of 379 million RMB, a 10% increase year-on-year, achieving profitability with a net profit of 8.4 million RMB [2]. Group 3: Market Position - Xintianxia holds a 3.7% market share in the global code flash memory market and 6.6% in the SLC NAND Flash sector as of 2024 [3]. - The company has made significant advancements in high-performance, large-capacity storage, successfully producing a 2Gbit SPI NOR Flash based on ETOX 55nm technology, breaking the monopoly of foreign companies in high-end applications [3]. Group 4: Strategic Initiatives - The company is focusing on a "Storage + AI" strategy to enhance efficiency in edge computing, responding to the growing demand for high-performance storage chips driven by AI applications [4]. - Xintianxia is expanding its product lines to include analog chips and MCUs, providing comprehensive chip solutions that integrate power supply, control, storage, and drive functions [5]. - The company is also developing in-memory computing (CIM) acceleration chips based on ReRAM technology, aiming for production by the end of 2026, targeting edge AI applications [5]. Group 5: Future Outlook - The importance of storage chips is expected to grow as AI technology penetrates new sectors such as smart vehicles and humanoid robots, with Xintianxia's upcoming IPO seen as a potential catalyst for enhancing its global brand recognition and technological capabilities [6].

突破“存储墙”,三路并进

3 6 Ke· 2025-12-31 03:35

Core Insights - The explosive growth of AI and high-performance computing is driving an exponential increase in computing demand, leading to a significant challenge known as the "storage wall" [1][2] - The competition for AI and high-performance computing chips will focus not only on transistor density and frequency but also on memory subsystem performance, energy efficiency, and integration innovation [1][4] Group 1: AI and Computing Demand - The evolution of AI models has led to a dramatic increase in computational requirements, with model parameters rising from millions to trillions, resulting in a training computation increase of over 10^18 times in the past 70 years [2][4] - The growth rate of computational performance has significantly outpaced that of memory bandwidth, creating a "bandwidth wall" that limits overall system performance [4][7] Group 2: Memory Technology Challenges - The traditional memory technologies are struggling to meet the unprecedented demands for performance, power consumption, and area (PPA) from various applications, including large language models and edge devices [1][4] - The average growth of DRAM bandwidth over the past 20 years has only been 100 times, compared to a 60,000 times increase in hardware peak floating-point performance [4][7] Group 3: TSMC's Strategic Insights - TSMC emphasizes that the future evolution of memory technology will revolve around "storage-compute synergy," transitioning from traditional on-chip caches to integrated memory solutions that enhance performance and energy efficiency [7][11] - TSMC is focusing on optimizing embedded memory technologies such as SRAM, MRAM, and DCiM to address the challenges posed by AI and HPC demands [11][33] Group 4: SRAM Technology - SRAM is identified as a key technology for high-speed embedded memory, offering low latency, high bandwidth, and low power consumption, making it essential for various high-performance chips [12][16] - The area scaling of SRAM is critical for optimizing chip performance, but it faces challenges as technology nodes advance to 2nm [12][17] Group 5: Computing-in-Memory (CIM) - CIM architecture represents a revolutionary approach that integrates computing capabilities directly into memory arrays, significantly reducing energy consumption and latency associated with data movement [21][24] - TSMC believes that DCiM (Digital Computing-in-Memory) has greater potential than ACiM (Analog Computing-in-Memory) due to its compatibility with advanced processes and flexibility in precision control [26][28] Group 6: MRAM Technology - MRAM is emerging as a viable alternative to traditional embedded flash memory, offering non-volatility, high reliability, and durability, making it suitable for applications in automotive electronics and edge AI [33][35] - TSMC's N16 FinFET embedded MRAM technology meets stringent automotive requirements, showcasing its potential in high-performance applications [39][49] Group 7: System-Level Integration - TSMC advocates for a system-level approach to memory technology breakthroughs, emphasizing the need for 3D packaging and chiplet integration to achieve high bandwidth and low latency [50][54] - The future of AI chips may see a blurring of boundaries between memory and computation, with innovations in 3D stacking and integrated voltage regulators enhancing overall system performance [60][61] Group 8: Future Outlook - The future of storage technology in AI computing is characterized by a comprehensive innovation revolution, with TSMC's roadmap focusing on SRAM, MRAM, and DCiM to overcome the "bandwidth wall" and energy efficiency challenges [62] - The ability to achieve full-stack optimization from transistors to systems will be crucial for leading the next era of AI computing [62]

突破“存储墙”,三路并进

半导体行业观察· 2025-12-31 01:40

Core Viewpoint - The article discusses the exponential growth of AI and high-performance computing, highlighting the emerging challenge of the "storage wall" that limits the performance of AI chips due to inadequate memory bandwidth and efficiency [1][2]. Group 1: AI and Storage Demand - The evolution of AI models has led to a dramatic increase in computational demands, with model parameters rising from millions to trillions, resulting in a training computation increase of over 10^18 times in the past 70 years [2]. - The performance of any computing system is determined by its peak computing power and memory bandwidth, leading to a significant imbalance where hardware peak floating-point performance has increased 60,000 times over the past 20 years, while DRAM bandwidth has only increased 100 times [5][8]. Group 2: Memory Technology Challenges - The rapid growth in computational performance has not been matched by memory bandwidth improvements, creating a "bandwidth wall" that restricts overall system performance [5][8]. - AI inference scenarios are particularly affected, with memory bandwidth becoming a major bottleneck, leading to idle computational resources as they wait for data [8]. Group 3: Future Directions in Memory Technology - TSMC emphasizes that the evolution of memory technology in the AI and HPC era requires a comprehensive optimization across materials, processes, architectures, and packaging [12]. - The future of memory architecture will focus on "storage-compute synergy," transitioning from traditional on-chip caches to integrated memory solutions that enhance performance and efficiency [12][10]. Group 4: SRAM as a Key Technology - SRAM is identified as a critical technology for high-performance embedded memory due to its low latency, high bandwidth, and energy efficiency, widely used in various high-performance chips [13][20]. - TSMC's SRAM technology has evolved through various process nodes, with ongoing innovations aimed at improving density and efficiency [14][22]. Group 5: Computing-in-Memory (CIM) Innovations - CIM architecture represents a revolutionary approach that integrates computing capabilities directly within memory arrays, significantly reducing data movement and energy consumption [23][26]. - TSMC believes that Digital Computing-in-Memory (DCiM) has greater potential than Analog Computing-in-Memory (ACiM) due to its compatibility with advanced processes and flexibility in precision control [28][30]. Group 6: MRAM Developments - MRAM is emerging as a viable alternative to traditional embedded flash memory, offering non-volatility, high reliability, and durability, making it suitable for applications in automotive electronics and edge AI [35][38]. - TSMC's MRAM technology meets stringent automotive requirements, providing robust performance and longevity [41][43]. Group 7: System-Level Integration - TSMC advocates for a system-level approach to memory and compute integration, utilizing advanced packaging technologies like 2.5D/3D integration to enhance bandwidth and reduce latency [50][52]. - The future of AI chips may see a blurring of the lines between memory and compute, with tightly integrated architectures that optimize energy efficiency and performance [58][60].

炬芯科技(688049):2025年三季报点评:持续刷新单季业绩记录,份额提升&端侧卡位共驱高速成长

Huachuang Securities· 2025-10-29 12:45

Investment Rating - The report maintains a "Strong Buy" rating for the company, indicating an expectation to outperform the benchmark index by over 20% in the next six months [1][23]. Core Insights - The company has achieved record quarterly performance, with Q3 2025 revenue reaching 273 million yuan, a year-over-year increase of 46.64% and a quarter-over-quarter increase of 6.16%. The net profit attributable to shareholders was 60 million yuan, reflecting a year-over-year growth of 101.09% and a quarter-over-quarter growth of 20.72% [1][8]. - The company is experiencing robust growth in market share and product offerings, particularly in the AI-enabled edge computing sector, which is driving significant revenue increases [8]. - The report highlights the successful penetration of the Bluetooth speaker SoC market, with increasing collaboration with leading audio brands and a strong demand for low-latency wireless audio products [8]. Financial Summary - Total revenue projections for the company are as follows: 652 million yuan in 2024, 986 million yuan in 2025, 1,324 million yuan in 2026, and 1,745 million yuan in 2027, with respective growth rates of 25.3%, 51.3%, 34.3%, and 31.8% [3]. - Net profit attributable to shareholders is forecasted to be 107 million yuan in 2024, 212 million yuan in 2025, 295 million yuan in 2026, and 397 million yuan in 2027, with growth rates of 63.8%, 98.8%, 39.2%, and 34.7% respectively [3]. - The report projects earnings per share (EPS) to increase from 0.61 yuan in 2024 to 2.27 yuan in 2027, with a corresponding decrease in price-to-earnings (P/E) ratio from 97 to 26 over the same period [3]. Market Position and Strategy - The company is strategically positioned in the AI edge computing market, focusing on low-power, high-performance chip development to meet the growing demand for advanced audio products [8]. - The report emphasizes the company's commitment to innovation, particularly in developing proprietary protocols to enhance wireless transmission capabilities and reduce latency [8]. - The target price for the company's stock is set at 87.58 yuan, based on a projected P/E ratio of 52x for 2026, reflecting confidence in the company's growth trajectory [3][8].

存内计算芯片,热度大增

半导体行业观察· 2025-10-26 03:16

Core Insights - The article emphasizes the importance of edge AI and the need for efficient memory and computation solutions to reduce power consumption and latency in edge devices [3][4][10]. Group 1: Edge AI Challenges - Edge AI applications require real-time responses and often deal with sensitive data that cannot be shared with third parties, leading to strict limitations on computational resources [3]. - In typical mobile workloads, data movement in memory accounts for 62% of total energy consumption, highlighting the inefficiency of current memory systems [3]. Group 2: Memory Solutions - Near-memory computing and advanced memory technologies like RRAM (Resistive Random Access Memory) and ferroelectric capacitors are proposed as potential solutions to address power and performance issues [4][5]. - RRAM offers high read endurance but has low write endurance, making it suitable for inference tasks but challenging for training tasks that require frequent updates [6][9]. Group 3: Hybrid Approaches - Hybrid solutions combining RRAM and ferroelectric materials can leverage the strengths of both technologies, allowing for efficient training and inference in edge AI applications [5][7]. - The integration of ferroelectric transistors into CMOS processes is complex but necessary for achieving high performance in memory computing [6][7]. Group 4: New Computational Frameworks - Memory computing can enhance not only traditional neural network computations but also facilitate the development of new modeling methods, such as solving Ising glass problems [10][11]. - Future advancements in memory computing will require new software frameworks that can adapt memory access patterns to specific problem requirements, independent of external memory controllers [13].

炬芯科技(688049):智能音频业务高速增长 存内计算加速落地

Xin Lang Cai Jing· 2025-08-26 00:33

Group 1 - The company achieved steady revenue growth in the first half of 2025, with a revenue of 449 million yuan, representing a year-over-year increase of 60.12% [1] - The gross profit margin reached 50.67%, an increase of 4.21 percentage points year-over-year, while the net profit attributable to shareholders was 91 million yuan, up 123.19% year-over-year [1] - In Q2 2025, the company reported a revenue of 257 million yuan, a year-over-year increase of 58.72% and a quarter-over-quarter increase of 33.98% [1] Group 2 - The SoC chip business experienced rapid growth, with significant penetration in the AIoT and wireless audio markets, driven by the integration of AI and hardware [2] - The company launched three AI audio chips (ATS323X, ATS362X, ATS286X) that have been quickly adopted by brand customers in wireless microphone products [2] - The company is strengthening partnerships with leading brands like Harman, Sony, and Bose, enhancing its market share in the Bluetooth speaker chip market [2] Group 3 - The commercialization of in-memory computing technology is accelerating, with the second generation of in-memory computing IP development on track to enhance NPU performance and energy efficiency [3] - The company is upgrading its ANDT development tools to strengthen the AI development ecosystem, facilitating model deployment for customers [3] - Revenue forecasts for 2025-2027 have been slightly adjusted, with expected revenues of 1 billion, 1.187 billion, and 1.485 billion yuan respectively, and net profits adjusted to 170 million, 270 million, and 370 million yuan [3]

炬芯科技董事长周正宇:以极致能效比打造长期核心竞争力

Zheng Quan Shi Bao Wang· 2025-05-28 12:16

Core Viewpoint - Yuchip Technology (688049) is focusing on high R&D investment and has achieved rapid growth in the Bluetooth speaker and audio markets, aiming for high-quality development through a differentiated strategy that emphasizes energy efficiency [1][2]. Group 1: Financial Performance - Yuchip Technology's net profit is projected to grow by 26.9% in 2024, with a staggering 385% increase in the first quarter of 2025 compared to the same period last year [2]. - The first quarter of 2025 marked the best quarterly performance since the company's listing, outperforming traditional peak seasons [2]. Group 2: Market Position and Strategy - The company has reached the second-largest market share in the Bluetooth speaker market and is targeting to surpass international brands like Harman, Sony, and Bose, aiming for a global market presence [2]. - Yuchip is not only focused on domestic market replacement but is also pursuing a global vision to compete with international giants [2]. Group 3: Technological Innovation - The company is investing heavily in a technology called in-memory computing, which enhances energy efficiency and supports AI functionalities without increasing battery usage [3]. - Yuchip's strategy prioritizes achieving a high energy efficiency ratio rather than merely increasing computational power, positioning itself as a leader in energy-efficient AI solutions [3]. Group 4: Leadership and Corporate Culture - The founder, Zhou Zhengyu, reflects on past experiences and emphasizes the importance of recognizing the core competencies of the team and being on the right track for sustainable growth [4]. - The company's ownership structure, with the team holding 30% of shares, is designed to incentivize long-term commitment and competitiveness [4].

炬芯科技:炬力前行,用芯聆听

China Post Securities· 2025-05-13 03:23

Investment Rating - The report maintains a "Buy" rating for the company [1] Core Views - The company specializes in wireless audio ICs, targeting high-end consumer and professional audio markets globally. Its main products include Bluetooth audio SoC chip series, portable audio and video SoC chip series, and smart voice interaction SoC chip series, which are widely used in Bluetooth speakers, headphones, smart education, and smart home applications. The company has become a mainstream supplier in the low-power wireless IoT field related to audio and has gradually achieved domestic substitution in relevant chip areas [2] - The company serves both international and domestic top-tier brands, including Harman, Sony, Bose, and Xiaomi, by providing differentiated chip combinations to meet the diverse needs of terminal brands in the market. This has led to increased penetration rates among mainstream terminal brands [2] - The company is continuously enhancing its product development and upgrades for 2.4G private communication protocols, which are widely applied in smart offices, smart homes, and industrial control. The latest generation of products supports a transmission power of up to 16dBm and a wireless transmission bandwidth of 4Mbps, showcasing strong wireless connection technology and anti-interference capabilities [2] - The company is leveraging AI advancements to enhance audio applications, including voice recognition and noise suppression. Its edge AI processor chips serve as a crucial link between audio and AI, providing low-power computing platforms for AI applications in IoT devices [2] Financial Forecast and Metrics - The company is projected to achieve revenues of 652 million yuan in 2024, with a growth rate of 25.34%, and is expected to reach 875 million yuan in 2025, 1,149 million yuan in 2026, and 1,493 million yuan in 2027. The net profit attributable to the parent company is forecasted to be 107 million yuan in 2024, growing to 163 million yuan in 2025, 231 million yuan in 2026, and 309 million yuan in 2027 [3][4] - The company's EBITDA is expected to grow from 80 million yuan in 2024 to 346 million yuan in 2027, indicating a strong upward trend in profitability [3] - The earnings per share (EPS) is projected to increase from 0.73 yuan in 2024 to 2.12 yuan in 2027, reflecting the company's robust growth potential [3] Product and Market Development - The company is deepening its focus on smart audio SoC technology, leading innovations in audio technology [5][8] - The company is expanding its market share in portable and home audio markets, particularly in wireless microphones and soundbars, with a gradual increase in market penetration [24][46] - The company is actively exploring the wireless microphone market, which is experiencing growth due to the rise of video streaming and content creation, with its products gaining popularity for their low power consumption and excellent noise reduction capabilities [50][51] R&D and Talent - The company is increasing its R&D investment, with a projected R&D expense rate of 33% in 2024, and total R&D expenditure expected to reach 215 million yuan, a year-on-year increase of 30.06% [22] - The company has optimized its R&D personnel structure, with 266 R&D staff accounting for 73.08% of the total workforce, focusing on high-performance and low-power technology innovations [22]