重庆银行

Search documents

内银股普涨,农业银行涨超1%再创新高,录得10连阳

Ge Long Hui· 2025-10-22 02:11

Core Viewpoint - The Hong Kong banking sector continues to experience an upward trend, with Agricultural Bank of China reaching a new historical high and recording a 10-day consecutive rise, indicating strong market performance in the sector [1]. Group 1: Market Performance - Agricultural Bank of China has increased by over 1%, achieving a new historical high [1]. - Other banks such as Chongqing Bank, Zheshang Bank, Zhengzhou Bank, China Merchants Bank, Industrial and Commercial Bank of China, CITIC Bank, and Bank of China also reported gains [1]. Group 2: Analyst Insights - Morgan Stanley believes that after a seasonal adjustment in Q3, the banking sector will present good investment opportunities in Q4 and Q1 of the following year [1]. - The upcoming dividend distributions, stabilization of interest rates, and support from a 500 billion RMB structural financial policy tool are expected to bolster the revaluation of Chinese banking stocks [1]. - Investors should focus on high-quality banks that are likely to achieve earlier and stronger rebounds in a "natural clearing" environment [1].

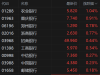

港股异动丨内银股普涨,农业银行涨超1%再创新高,录得10连阳

Ge Long Hui· 2025-10-22 01:56

Group 1 - The core viewpoint is that Hong Kong bank stocks are experiencing a bullish trend, with Agricultural Bank of China reaching a new historical high and achieving a 10-day consecutive rise [1] - Morgan Stanley anticipates that after a seasonal adjustment in Q3, there will be good investment opportunities in Q4 and Q1 of the following year for domestic bank stocks [1] - Factors supporting the revaluation of Chinese banking stocks include upcoming dividend distributions, stabilized interest rates, a 500 billion RMB structural financial policy tool, and a more sustainable policy path [1] Group 2 - Agricultural Bank of China saw an increase of 1.04%, reaching a latest price of 5.820 [2] - Other banks also recorded gains, including Chongqing Bank (+0.91%), Zhengzhou Bank (+0.78%), and Zhejiang Bank (+0.77%) [2] - The overall trend indicates a positive performance across various banks, with notable increases in share prices for several institutions [2]

银行板块再度上扬,农业银行14连阳再创新高

Xin Lang Cai Jing· 2025-10-22 01:52

Core Insights - The banking sector has experienced a significant rally, with Agricultural Bank achieving a 14-day consecutive rise, reaching a new high [1] - The banking index has also seen a 10-day consecutive increase, indicating strong overall performance in the sector [1] - Several banks, including Jiangyin Bank, CITIC Bank, Zheshang Bank, Wuxi Bank, and Chongqing Bank, have shown upward movement in their stock prices [1]

农业银行实现“13连阳”,后市怎么看

Huan Qiu Wang· 2025-10-22 01:07

Core Viewpoint - Agricultural Bank of China (ABC) has shown a strong stock performance, achieving a 54.2% increase year-to-date, outperforming the overall banking sector, and reaching a market capitalization of 2.76 trillion yuan, leading the A-share banking sector [1][3][4] Group 1: Stock Performance - ABC's stock price increased by 1.68% to 7.88 yuan per share, marking a historical high of 7.89 yuan during trading, achieving a rare "13 consecutive days of gains" [1] - In October, the banking sector as a whole rebounded, with a cumulative increase of 7.47%, indicating a shift in market focus towards banking stocks [3] - Among state-owned banks, ABC led with an 18.14% increase in October, marking its largest monthly gain of the year [4][5] Group 2: Market Dynamics - Analysts suggest that the current rally in ABC's stock is primarily driven by valuation recovery rather than a shift to growth pricing, with its dividend yield significantly higher than government bond yields [5][6] - The resilience of ABC's fundamentals, including low deposit costs and controllable non-performing loan ratios, has strengthened its market position [5][6] Group 3: Investment Trends - Insurance funds are becoming a significant source of incremental capital for the banking sector, with a preference for high-dividend, low-volatility assets [7][8] - The proportion of bank stocks in the market value of insurance funds has increased, with bank stocks accounting for 47.2% of the total as of mid-2025 [7] Group 4: Future Outlook - Multiple institutions are optimistic about the banking sector's performance in the fourth quarter, with expectations of stable net interest margins and a gradual recovery in net interest income growth [9][10] - The overall dividend yield for major state-owned banks has returned to high levels, with many exceeding 4%, indicating a favorable risk-return profile for investors [9][10]

详解季报期的金融股投资机会

2025-10-21 15:00

详解季报期的金融股投资机会 20251021 摘要 保险公司通过提升权益仓位和优化结构,特别是 7 月以来加速加仓成长 股,提高了投资收益率,使其整体权益结构与市场风格的匹配度更高。 利率上行环境下,部分 VFA 保单评估利率按市场利率核算,显著提升了 保险公司的承保服务业绩,中国人寿在此方面表现突出。即使未发布业 绩预增公告的公司,其增速也超市场预期。 当前环境下,推荐保险股的核心逻辑是投资端弹性。在利差收窄压力下, 关注投资端边际弹性更大的公司,首推新华保险和中国人寿,关注中国 平安和中国人保。 券商板块在 2025 年三季度表现超预期,同比增速达 60%。未来发展主 线包括居民资产配置重配带来的财富管理和资产管理业务增长,以及国 际化进程加快带来的新盈利增长点。 长期看好零售业务有竞争优势且国际化战略突出的券商,如中信证券和 华泰证券。同时,自营弹性较大的兴业证券和长江证券也值得关注。 银行板块整体业绩稳定,预计营收增速微正,利润增速约 1%。债券市 场波动影响有限,规模增长稳定,负债成本下降支撑净利息收入增速。 上市银行 OCI 浮盈可调节收入。 银行个股推荐方面,关注基本面和业绩积极变化的招商银行、 ...

冶钢原料板块10月21日涨1.43%,大中矿业领涨,主力资金净流入6461.47万元

Zheng Xing Xing Ye Ri Bao· 2025-10-21 08:21

Market Overview - The steel raw materials sector increased by 1.43% compared to the previous trading day, with Dazhong Mining leading the gains [1] - The Shanghai Composite Index closed at 3916.33, up 1.36%, while the Shenzhen Component Index closed at 13077.32, up 2.06% [1] Individual Stock Performance - Dazhong Mining (001203) closed at 13.78, with a rise of 5.35% and a trading volume of 362,700 shares, amounting to a transaction value of 503 million yuan [1] - Triangle Mining (601969) saw a 3.75% increase, closing at 9.41, with a trading volume of 656,800 shares and a transaction value of 615 million yuan [1] - Baodi Mining (601121) increased by 1.98%, closing at 7.22, with a trading volume of 276,000 shares and a transaction value of 2.66 million yuan [1] - Jinding Mining (000655) rose by 1.82%, closing at 10.05, with a trading volume of 1,391,200 shares and a transaction value of 393 million yuan [1] - Hebei Steel Resources (000923) increased by 1.34%, closing at 18.19, with a trading volume of 189,700 shares and a transaction value of 347 million yuan [1] - Steel Titanium Co. (000629) saw a modest increase of 1.02%, closing at 2.96, with a trading volume of 847,600 shares and a transaction value of 251 million yuan [1] - Guangdong Mingzhu (600382) experienced a slight decline of 0.27%, closing at 7.50, with a trading volume of 467,100 shares and a transaction value of 345 million yuan [1] - Fangda Carbon (600516) decreased by 0.56%, closing at 5.36, with a trading volume of 657,700 shares and a transaction value of 353 million yuan [1] - Ordos (600295) fell by 0.86%, closing at 10.42, with a trading volume of 91,500 shares and a transaction value of 95.34 million yuan [1] Capital Flow Analysis - The steel raw materials sector saw a net inflow of 64.61 million yuan from main funds, while retail funds experienced a net outflow of 61.74 million yuan [1] - The main funds' net inflow for Hainan Mining (601963) was 32.12 million yuan, while retail funds had a net outflow of 30.96 million yuan [2] - Hebei Steel Resources (000923) had a main fund net inflow of 17.36 million yuan and a retail fund net outflow of 39.21 million yuan [2] - Dazhong Mining (001203) recorded a main fund net inflow of 15.63 million yuan, with retail funds seeing a net outflow of 11.99 million yuan [2] - Baodi Mining (601121) had a main fund net inflow of 12.75 million yuan, while retail funds experienced a net outflow of 16.52 million yuan [2] - Jinding Mining (000655) saw a main fund net inflow of 7.72 million yuan, with retail funds having a net outflow of 8.78 million yuan [2]

金融行业周报:央行发布前三季度金融统计数据报告,证监会修订《上市公司治理准则》-20251020

Ping An Securities· 2025-10-20 07:01

Investment Rating - The industry investment rating is "Outperform the Market," indicating an expected performance of the industry index to exceed the CSI 300 index by more than 5% within the next six months [42]. Core Insights - The People's Bank of China reported that the new RMB loans increased by 1.29 trillion yuan in September 2025, a year-on-year decrease of 300 billion yuan, with a balance growth rate of 6.6%. The social financing scale increased by 3.53 trillion yuan, which is 233.9 billion yuan less than the same period last year, with a year-on-year growth rate of 8.7% [3][15]. - The China Securities Regulatory Commission revised the "Corporate Governance Standards for Listed Companies," effective January 1, 2026, to enhance governance standards and protect investor rights [4][17]. - A joint opinion from several ministries aims to improve the overseas comprehensive service system for Chinese enterprises, focusing on enhancing international competitiveness and safeguarding legitimate rights abroad [5][19]. Summary by Sections Financial Statistics - In September 2025, M0, M1, and M2 grew by 11.5%, 7.2%, and 8.4% year-on-year, respectively. The growth rates of M2 and social financing remained high, supporting economic recovery [3][14]. Corporate Governance - The revised governance standards emphasize the regulation of directors and senior management, the establishment of incentive mechanisms, and the regulation of controlling shareholders to enhance corporate governance effectiveness [4][18]. Overseas Services - The guidance document outlines six areas with 16 specific measures to enhance overseas services for Chinese enterprises, including optimizing public services and strengthening economic cooperation guarantees [5][19]. Market Performance - This week, the banking, securities, insurance, and fintech indices changed by +4.89%, -3.13%, +3.65%, and -5.08%, respectively, with the banking sector showing the highest performance [20][10]. Securities Market Data - The average daily trading volume of stock funds reached 28,985 billion yuan, reflecting a 4.8% increase from the previous week [28][29]. The margin financing balance was 24,572 billion yuan, up 0.48% week-on-week [33].

中信证券:银行基本面稳定 绝对收益有望延续

智通财经网· 2025-10-20 00:19

Core Viewpoint - The macro-prudential management expansion and the enhancement of financial stability tools are expected to lead banks into a new phase of risk management, which will strengthen their balance sheets and accelerate the realization of net asset revaluation expectations [1][2]. Summary by Sections Macro-Prudential Management - The interview with the head of the Financial Stability Bureau of the People's Bank of China emphasizes the need to balance growth and risk prevention, expanding the macro-prudential management framework and enhancing the financial stability toolbox [2]. - Future regulations will likely deepen oversight of non-traditional banking activities, including wealth management and asset management subsidiaries [2]. Banking Sector Performance - The banking sector is expected to maintain a stable performance in Q3, with positive trends in interest margins and stable non-performing loan generation, although investment income may see a quarter-on-quarter decline [1][4]. - The KBW bank index experienced a significant drop due to concerns over credit risks in U.S. regional banks, leading to a market capitalization loss of over $100 billion for 74 major banks in a single day [3]. Stock Market Trends - Last week, both A-shares and H-shares in the banking sector outperformed the broader market, with notable gains in individual bank stocks, particularly Chongqing Bank and Agricultural Bank [4]. - The increase in mid-term dividends from banks, now reaching 17 institutions, contributes to the relative and absolute returns of bank stocks amid rising market uncertainties [4]. Investment Strategy - The banking sector is seen as offering significant value, with a shift towards alpha strategies in stock selection, focusing on companies with high and stable ROE and optimistic valuation space [1][4].

银行业周度追踪2025年第41周:如何展望银行股行情的持续性?-20251019

Changjiang Securities· 2025-10-19 13:45

Investment Rating - The investment rating for the banking sector is "Positive" and is maintained [11] Core Viewpoints - There is still divergence in the market regarding the sustainability of the banking stock market. However, it is believed that valuation recovery will continue. From a strategic perspective, it is essential to view the relationship between banking stocks and market sentiment dialectically. In the medium to long term, undervalued banking stocks align with the market's slow bull direction, as the index has been reaching new highs over the past year. In the short term, the performance of growth stocks benefiting from high-risk preferences may diverge from low-risk banking stocks, which indirectly help stabilize the index [6][38] - The fundamental logic supporting the valuation recovery of banking stocks remains solid. The trend of establishing a bottom line for significant risks in urban investment, real estate, and capital is clear, with policies still supporting urban investment debt and orderly capital replenishment for important banks. Mainstream banks continue to show stable growth in performance, with revenue growth points shifting from investment income to net interest income since 2025. It is expected that more banks will see a reversal in net interest income growth as deposit costs continue to decline in 2026 [6][39] Summary by Sections Market Performance - This week, the banking index rose by 5.0%, outperforming the CSI 300 and ChiNext indices by 7.3% and 10.7%, respectively. The market's risk appetite has decreased since the fourth quarter, but the banking sector has seen significant relative gains due to a valuation recovery [2][8] - Individual stocks such as Chongqing Bank and Yunnan Rural Commercial Bank led the gains, while the stock price of Shanghai Pudong Development Bank showed notable elasticity as its convertible bonds approach maturity [19][21] Trading Dynamics - Each round of adjustment presents opportunities for low-valuation configurations. The mid-term dividend has already started, and the demand for dividend assets from absolute return funds remains unchanged. The pressure from new funds and the maturity of existing non-standard assets will push the dividend yield of banking stocks to continue declining [7][39] - The trading volume and turnover rate of state-owned banks, city commercial banks, and rural commercial banks have decreased compared to last week, but the turnover rate of banking stocks has begun to rise again, indicating a change in market risk appetite [10][31] Convertible Bonds - Attention is drawn to the strong redemption trading opportunities for convertible bonds in the banking sector. As the banking sector rises, the stock prices of convertible bond banks are approaching their strong redemption prices. The recent rebound in the stock price of Shanghai Pudong Development Bank has been driven by active conversions by major shareholders [9][26] Future Outlook - The market remains optimistic about the effectiveness of anti-involution measures and the expected recovery of the PPI next year. If macroeconomic recovery resolves the asset shortage contradiction, the fundamentals of banking stocks will benefit accordingly. Additionally, local state-owned assets and industrial capital continue to have a positive outlook on banking stocks, with frequent increases in holdings by major shareholders and management since the third quarter [7][39]

银行三季报业绩增长可期

Xiangcai Securities· 2025-10-19 12:11

Investment Rating - The industry rating is maintained at "Overweight" [10][34] Core Views - The banking sector is expected to see positive growth in Q3, with revenue growth of 1.0% and net profit growth of 0.8% in the first half of the year, indicating a stabilization trend [8][32] - Credit growth has been slowing down due to a significant decrease in bill financing, reflecting a weakened demand for scale expansion among banks [8][32] - The introduction of new policy financial tools is anticipated to support medium to long-term corporate loans, improving the loan structure [8][33] - Deposit growth remains strong, which is expected to help stabilize funding costs and potentially lead to a recovery in net interest margins [8][33] Summary by Sections Industry Performance - The banking sector's performance has shown a relative return of 2.3% over the past month, with an absolute return of 1.5% [7] - The banking index increased by 4.89% during the period from October 13 to October 19, outperforming the CSI 300 index by 7.12 percentage points [12] Financial Metrics - The net interest margin decreased by 8 basis points in the first half of the year, but is expected to stabilize in the second half [8][33] - Non-interest income is projected to remain stable, supported by growth in intermediary business income and favorable market conditions for capital markets [9][32] Investment Recommendations - The report suggests focusing on state-owned banks for their stable high dividend yield and potential valuation recovery opportunities in joint-stock and regional banks [10][34] - Specific banks recommended include CITIC Bank, Jiangsu Bank, Chengdu Bank, Shanghai Rural Commercial Bank, Chongqing Rural Commercial Bank, Changshu Bank, and Suzhou Bank [10][34]