NCI(601336)

Search documents

智通港股投资日志|10月30日

智通财经网· 2025-10-29 16:03

Group 1 - The article provides a list of companies and their respective activities related to shareholder meetings, new stock activities, performance announcements, and dividend distributions scheduled for October 30, 2025 [1][2][5][7]. - Several companies are mentioned as being in the process of initial public offerings (IPOs), including 旺山旺水-B, 均胜电子, 文远知行-W, and 赛力斯 [6]. - Companies such as 美的集团 and 翰森制药 are noted for their dividend distribution dates, indicating ongoing shareholder returns [7][8]. Group 2 - The article highlights the resumption of trading for companies like 舍图控股, 鸿盛昌资源, and 安能物流, suggesting a return to market activity after previous suspensions [6][7]. - The document lists various companies involved in dividend payouts, which may attract investor interest due to potential income generation [8]. - The presence of multiple companies in the IPO stage indicates a potentially active market environment for new investments [6].

【兴证非银&金融科技】新华保险深度报告:兼具价值成长性与业绩高弹性的纯寿险标的

Xin Lang Cai Jing· 2025-10-29 15:07

Core Viewpoint - The company is positioned for high-quality development through channel transformation and asset optimization, leading to a significant enhancement in profitability and operational quality, which drives a comprehensive revaluation of its value [1] Group 1: Performance and Growth - The company has a high operational leverage of 21.3 times as of mid-2025, compared to 9-13 times for listed peers, indicating strong performance elasticity [1] - The net profit attributable to shareholders is projected to increase by 201% year-on-year to 26.2 billion yuan in 2024, with a 33.5% year-on-year growth to 14.8 billion yuan in the first half of 2025 [1] - The company’s new business value (NBV) has shown robust growth, with increases of 65.1%, 106.8%, and 58.4% year-on-year for 2023 and the first half of 2025, maintaining a leading position among peers [2] Group 2: Channel and Product Optimization - The company has transitioned its agent channel from a "mass strategy" to a "professional elite" model, reducing the number of agents from 606,000 in 2020 to 136,000 by 2025, while increasing monthly per capita productivity from 2,617 yuan to 16,700 yuan [2] - The silver insurance channel has become a new growth driver, with the new business value rate improving by 3 percentage points compared to the end of 2024, reaching 52.8% of total new business value [2] Group 3: Asset Allocation and Investment Strategy - As of mid-2025, the total investment assets have increased to 1.71 trillion yuan, a 5.1% growth from the beginning of the year, with a significant shift in asset allocation towards bonds and equities [3] - The company has increased its bond allocation from 42.7% to 50.6% and equity allocation from 7.9% to 11.6% from the end of 2020 to mid-2025, enhancing its investment performance elasticity [3] - The annualized total investment return rate is 5.9% as of mid-2025, leading among listed peers, reflecting strong equity allocation and market timing capabilities [3] Group 4: Investment Outlook - The company is expected to exhibit high performance elasticity in the short term, particularly in a bullish equity market, with projected net profit for the first three quarters of 2025 estimated between 29.99 billion and 34.12 billion yuan, representing a year-on-year growth of 45% to 65% [4] - The new management has initiated a comprehensive strategic overhaul, enhancing operational vitality and driving robust internal growth momentum, with a focus on shareholder returns and stable dividend rates [4]

新华保险召开第22届全渠道高峰会,明确未来五大重点工作

Xin Lang Cai Jing· 2025-10-29 11:45

10月29日,新华保险召开第22届全渠道高峰会。会议现场集中发布了九大具有开创性和引领性的发展成 果,涵盖大产品体系、大培训体系、医康养服务体系、高客经营体系、"新华瑞"2026服务体系、大科 技/AI 赋能体系等多个领域,同时提出了运营智享服务焕新升级规划,并发布了"新华宝典"、一站式营 销数字化平台"鑫智能",为公司的发展注入了新的活力。 新华保险表示,未来保险行业、健康养老产业将迎来黄金十年发展机遇。新华保险将全力建设中国一流 的金融服务集团,做客户全生命周期的综合金融服务商。 在此次会议上,新华保险明确了未来五大重点工作,包括:为队伍提供最好的销售赋能体系,用立体 式、全方位、多元化服务满足客户和队伍需求,打造更稳定、更专业、更高价值的职业发展创业平台, 把强大的投资优势变成市场竞争力、产品吸引力和队伍战斗力,全面推进客户服务与队伍销售走向数字 化、智能化。(智通财经记者 胡志挺) ...

东吴证券:三季度公募基金减持保险持仓 券商及互金持仓环比基本持平

Zhi Tong Cai Jing· 2025-10-29 10:53

Core Viewpoint - The report from Dongwu Securities indicates a slight decrease in public fund holdings in the non-bank financial sector as of the end of Q3 2025, with expectations for continued benefits from an improving market environment [1][5]. Summary by Category Public Fund Holdings - As of the end of Q3 2025, public fund stock investments in the non-bank financial sector accounted for 1.61%, a decrease of 0.32 percentage points from Q2 2025. This represents an underweight of 8.35 percentage points compared to the market capitalization of the CSI 300 index, with a slight narrowing of the underweight by 0.13 percentage points from Q2 2025 [2]. Insurance Sector - The insurance sector's holdings were at 0.78%, down 0.32 percentage points from Q2 2025. Notably, China Life and Ping An saw increases in shareholdings, while other companies like PICC and Taikang Life experienced significant reductions [3]. - The dynamic valuation for the insurance sector was 0.66x PEV, remaining stable compared to Q2 2025. The holdings for major insurers as of Q3 2025 were: China Life (0.02%), Ping An (0.48%), Taikang (0.18%), Xinhua (0.09%), and PICC (0.01%) [3]. Brokerage and Internet Finance Sector - The holdings in the brokerage and internet finance sector remained relatively stable at 0.74%, with a slight increase of 0.01 percentage points from the first half of 2025. Traditional brokerages accounted for 0.54% of the holdings, reflecting a 0.01 percentage point increase [4]. - The valuation for the brokerage industry (CITIC Securities II Index) was 1.55x P/B at the end of Q3 2025, up from 1.41x P/B at the end of the first half of 2025 [4]. Market Trends and Recommendations - The non-bank financial sector has shown continuous improvement in market conditions, with significant increases in trading volumes. The average daily trading volume for equity funds reached 18,723 billion yuan in the first three quarters of 2025, a year-on-year increase of 109%, with Q3 alone seeing a 208% increase [5]. - Key recommendations for investment include China Ping An, Xinhua Insurance, China Life, CITIC Securities, Tonghuashun, and Jiufang Zhitu Holdings, as the sector remains underweighted in public fund portfolios [1][5].

新华保险第22届高峰会多维度赋能客户与队伍

Zheng Quan Ri Bao Wang· 2025-10-29 10:53

Core Insights - The 22nd All-Channel Summit of Xinhua Insurance was held in Yixing, Jiangsu, highlighting the company's achievements over the past year and recognizing outstanding sales teams and individuals [1] - Xinhua Insurance has made significant progress in its comprehensive strength, development efficiency, and corporate influence, aiming to become a leading financial service group in China with a focus on a "insurance + service + investment" collaborative development model [3] Group 1 - The company has enhanced its product system to better serve customers and sales teams, enriched its service ecosystem to improve customer management and service capabilities, and created an attractive career platform to enhance the sense of gain for the sales team [3] - Xinhua Insurance has actively participated in long-term investment pilot funds, invested in quality listed companies, and focused on hard technology and the health and elderly care industries, using its investment strength to drive the transformation of dividend insurance [3] - The application of AI technology has significantly improved customer experience and sales efficiency, with advancements in product development, customer service, underwriting, claims, and risk prevention [3] Group 2 - The summit introduced nine innovative development achievements across various fields, including a comprehensive product system, training system, health and elderly care service system, and a digital marketing platform called "Xing Smart" [4] - The company anticipates a golden decade of development opportunities in the insurance and health care industries and aims to become a comprehensive financial service provider for customers throughout their life cycle [4] - Five key focus areas for the future were outlined: enhancing sales empowerment, providing diverse services to meet customer and team needs, creating a stable and high-value career development platform, leveraging investment advantages for market competitiveness, and advancing digital and intelligent customer service and sales [4]

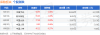

保险板块10月29日涨0.92%,中国平安领涨,主力资金净流出5.05亿元

Zheng Xing Xing Ye Ri Bao· 2025-10-29 08:41

Core Insights - The insurance sector experienced a rise of 0.92% on October 29, with China Ping An leading the gains [1] - The Shanghai Composite Index closed at 4016.33, up 0.7%, while the Shenzhen Component Index closed at 13691.38, up 1.95% [1] Insurance Sector Performance - China Ping An (601318) closed at 58.95, with a gain of 2.06% and a trading volume of 1.0444 million shares, amounting to a transaction value of 6.172 billion [1] - New China Life Insurance (601336) closed at 70.05, up 1.49%, with a trading volume of 169,100 shares [1] - China Pacific Insurance (601601) closed at 37.60, up 0.80%, with a trading volume of 590,700 shares [1] - China Life Insurance (601628) closed at 45.22, up 0.27%, with a trading volume of 175,700 shares [1] - China Reinsurance (601319) closed at 8.83, up 0.46%, with a trading volume of 589,300 shares [1] Fund Flow Analysis - The insurance sector saw a net outflow of 505 million from institutional investors, while retail investors contributed a net inflow of 434 million [1] - Among individual stocks, New China Life Insurance had a net inflow of 27.46 million from institutional investors, while China Ping An experienced a net outflow of 306 million [2] - China Life Insurance saw a net inflow of 19.49 million from retail investors, despite a net outflow of 51.38 million from institutional investors [2]

新华保险举行第22届高峰盛会

Jing Ji Guan Cha Wang· 2025-10-29 08:29

Core Insights - Xinhua Insurance (601336) held its 22nd All-Channel Summit in Yixing, where it announced nine major development achievements across various sectors [1] - The company aims to upgrade its "insurance + service + investment" collaborative development model to create a market-leading and competitive product system [1] Product Development - Xinhua Insurance will focus on three main areas: pension and wealth management product service systems, health care product service systems, and disability care product service systems [1] - New product offerings include the "Shengshi Glory Celebration Edition" whole life insurance (dividend type), "Shengshi Hengying" annuity insurance (dividend type), and "Kanghu Wuyou" nursing insurance [1] Service Expansion - The company has established a nationwide migratory elderly care network and launched renewed home elderly care service rights, along with expanding cross-border travel projects [1] - The first medium asset project, "Yixing Yada," has been launched in Yixing [1] Strategic Goals - Xinhua Insurance aims to build a first-class financial service group in China, serving as a comprehensive financial service provider throughout the customer lifecycle [1] - The company emphasizes a core goal of "five first-class" standards, providing the best sales empowerment system for its team [1] - There is a focus on creating a more stable, professional, and high-value entrepreneurial platform, leveraging strong investment advantages to enhance market competitiveness, product appeal, and team effectiveness [1] - The company plans to fully advance the digitalization and intelligence of customer service and team sales [1]

人保、国寿、太平、信保、中再、新华集体表态!

Jin Rong Shi Bao· 2025-10-29 05:45

Core Insights - The 20th Central Committee of the Communist Party of China approved the "15th Five-Year Plan" for economic and social development, outlining major principles and strategic deployments for the period [2] Group 1: China Life Insurance - China Life emphasized the importance of implementing the spirit of the 20th Central Committee as a major political task, focusing on the financial insurance sector's role in the "15th Five-Year Plan" [4][5] - The company aims to enhance its core competitiveness and foster new growth drivers while ensuring high-quality development and risk management [5] Group 2: China People's Insurance - China People's Insurance Group highlighted its commitment to serving the real economy and the public, focusing on its core functions as an economic stabilizer and social stabilizer [3] - The company plans to support national strategies, enhance healthcare and pension services, and contribute to common prosperity and regional development [3] Group 3: China Pacific Insurance - China Pacific Insurance is set to actively participate in the Guangdong-Hong Kong-Macao Greater Bay Area development, focusing on its main responsibilities and enhancing risk management [6] - The company aims to support technological innovation and green development while increasing the supply of inclusive insurance products [6] Group 4: China Export & Credit Insurance Corporation - China Export & Credit Insurance Corporation plans to expand its export credit insurance coverage and scale, aligning with the "Belt and Road" initiative and promoting balanced trade [7] - The company is focused on high-quality development and ensuring the successful completion of its "14th Five-Year Plan" [7] Group 5: China Reinsurance - China Reinsurance aims to enhance its high-quality development by focusing on its reinsurance functions and aligning its "15th Five-Year Plan" with national strategic goals [8] - The company is committed to risk management and ensuring the completion of its annual objectives while preparing for the "15th Five-Year Plan" [8] Group 6: New China Life Insurance - New China Life Insurance is focused on integrating its development with national reforms, emphasizing the importance of the "insurance + investment + service" model [9][10] - The company aims to leverage its long-term capital to support new productive forces and contribute to social governance and financial stability [9][10]

许昌监管分局同意新华保险鄢陵支公司营业场所变更

Jin Tou Wang· 2025-10-29 03:37

Core Viewpoint - The approval from the Xuchang Regulatory Bureau of the National Financial Supervision Administration indicates that Xinhua Life Insurance Co., Ltd. has successfully obtained permission to change the business address of its Yanling branch to a new location in Xuchang City, Henan Province [1] Group 1 - The new business address for the Yanling branch is specified as No. 5, 1-2 floors, Unit 1, Building 27, Siji Huacheng, Yanling County, Xuchang City, Henan Province [1] - Xinhua Life Insurance Co., Ltd. is required to handle the change and obtain the necessary permits in accordance with relevant regulations [1]

香港中国保险业 - 2025 年二季度香港保费增长加速;竞争持续加剧-Hong KongChina Insurance-2Q25 HK Premiums Growth Accelerated; Continued Intensified Competition

2025-10-29 02:52

Summary of the Conference Call on Hong Kong/China Insurance Industry Industry Overview - The conference call focused on the Hong Kong/China insurance industry, specifically discussing the premium growth and competitive landscape in the market during the second quarter of 2025 [7][2]. Key Points Premium Growth - Hong Kong's annualized premium equivalent (APE) reached HK$47.9 billion in 2Q25, representing a 57% year-on-year increase, significantly higher than the 25% growth observed in 1Q25 [3][2]. - This growth marks the second highest quarterly APE, just below the HK$51.2 billion recorded in 1Q25 [3][2]. - The strong influx of mainland Chinese visitors to Hong Kong is expected to maintain a consistent mix of onshore and offshore contributions to the market [3][2]. Competitive Landscape - Intense competition in the broker channel was highlighted, with its market share increasing by 5 percentage points year-on-year to 34% on an APE basis [4][2]. - In contrast, the banks and agency channels experienced a decline in market share, losing 6 percentage points and 2 percentage points, respectively, to 37% and 22% [4][2]. - Manulife's broker channel saw an impressive APE growth of 171%, while FWD's broker channel grew by 70% year-on-year [4][2]. - AIA and Prudential experienced a slight decline in market share, losing 2.2 percentage points and 3.2 percentage points year-on-year, while Manulife gained 0.5 percentage points [4][2]. Payment Patterns - The payment pattern for new business showed some growth, with single pay's first-year premium (FYP) remaining stable year-on-year at 45% of overall FYP, while the mix for policies with a duration of less than 5 years increased by 5 percentage points to 30% [5][2]. - The dominance of USD currency policies continued, accounting for 77% of total APE, while HKD policies gained 4 percentage points to represent 19% of total APE in 2Q25 [5][2]. Future Outlook - The competitive environment is expected to see some relief due to an illustrative rate cut at the end of June and further commission cuts anticipated in early 2026 [4][2]. Additional Insights - The report indicates that the overall industry view remains attractive, suggesting potential investment opportunities within the Hong Kong/China insurance sector [7][2]. - The data presented in the call is supported by various exhibits detailing market share, payment patterns, and visitor statistics, which provide a comprehensive view of the current market dynamics [12][2][18][2]. Conclusion - The Hong Kong/China insurance industry is experiencing robust growth in premiums, particularly in the broker channel, amidst intense competition. The future outlook suggests potential stabilization in competitive pressures, making it an attractive sector for investment.