阿里云

Search documents

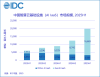

IDC:上半年中国AI IaaS市场规模达198.7亿元 整体市场同比增长122.4%

智通财经网· 2025-10-21 03:56

Core Insights - The overall AI IaaS market in China is expected to grow by 122.4% year-on-year, reaching a market size of 19.87 billion RMB by the first half of 2025 [1] - The GenAI IaaS market is projected to grow by 219.3%, with a market size of 16.68 billion RMB, while the Other AI IaaS market is expected to decline by 14.1%, reaching 3.19 billion RMB [1] Market Overview - The AI IaaS market is experiencing explosive growth, driven by strong demand across various sectors including internet, automotive, mobile manufacturing, finance, and government [5] - Cloud service providers have significantly increased capital investment in AI infrastructure, leading to stable resource supply and pricing in the computing market [5] - The demand for intelligent computing and AI applications is rising, particularly in the automotive sector, where competition for autonomous driving solutions is intensifying [5] GenAI IaaS Market Dynamics - The focus in the GenAI IaaS market is shifting from large-scale model training to inference, with inference scenarios accounting for 42% of the market share in the first half of the year [6] - The DeepSeek event has positively impacted the market, with significant deployments in state-owned enterprises and government sectors nearing completion [6] - Major enterprises are beginning to test generative AI applications within their business systems, indicating a shift towards more diverse AI applications [6] Supply Landscape - The supply landscape is evolving towards a diversified ecosystem, with cloud vendors and leading computing clients focusing on optimizing inference service cost structures [7] - Domestic and international cloud computing companies are increasingly investing in self-developed chips, signaling a new growth phase for domestic computing resources [7] Competitive Landscape - The GenAI IaaS market share has risen to 84%, while the Other AI IaaS market share has dropped to 16%, indicating a concentration of market power [9] - Alibaba Cloud maintains the largest market share by increasing capital expenditure on AI infrastructure and offering diverse AI IaaS services [9] - Other players like ByteDance's Volcano Engine and Baidu are also expanding their market presence through competitive pricing and technological advantages [9] Operator Developments - Major telecom operators are rapidly deploying intelligent computing resources, with significant growth in AI-related business [10] - China Telecom is building a distributed intelligent computing network, while China Mobile and China Unicom are enhancing their AI capabilities and service offerings [10] Future Projections - The AI IaaS market in China is expected to continue its rapid growth, potentially reaching nearly 150 billion RMB by 2029, with inference computing accounting for nearly 80% of the market [12] - Technological advancements in multi-modal models and video generation models are anticipated to drive new AI applications and further increase demand for AI computing resources [12]

全球首套脑机交互定制化磁共振平台启用,云计算ETF沪港深(517390)大涨2%,计算机ETF(159998)飘红

2 1 Shi Ji Jing Ji Bao Dao· 2025-10-21 02:17

Group 1 - The A-share market saw a strong performance on October 21, with the three major indices rising, particularly in the computer sector [1] - The Computer ETF (159998) increased by 0.39%, with notable gains from stocks like Jiangbolong, which rose over 3%, and other companies such as Zhongke Ruifeng and Keda Xunfei also showing positive movement [1] - The Cloud Computing ETF (517390) experienced a significant increase of 2%, with stocks like Zhongji Xuchuang rising over 5% and Alibaba-W increasing over 3% [1] Group 2 - The National Taxation Administration reported that the sales revenue of the equipment manufacturing industry grew by 9% year-on-year in the first three quarters, with computer communication equipment and industrial mother machines seeing increases of 13.5% and 11.8% respectively [2] - At the 2025 Brain-Computer Interface and MRI Summit, the world's first customized brain-computer interaction MRI platform "Shengong-Shengguan" was officially launched [2] - Alibaba Cloud's "Aegaeon" solution was selected for the top academic conference SOSP2025, demonstrating a significant reduction in the required number of NVIDIA H20 GPUs from 1192 to 213, a decrease of 82% [2] - Recent market sentiment has shown a decline in risk appetite, with the computer sector's previous gains being relatively modest, leading to improved cost-effectiveness for core leading companies in the sector [2] - It is suggested to focus on the third-quarter reports for short-term investment opportunities and to pay attention to high-quality stocks with marginal changes [2]

南京微短剧产业联盟成立,“攥指成拳”闯千亿级赛道

Nan Jing Ri Bao· 2025-10-21 02:13

Core Insights - The Nanjing micro-short drama industry is rapidly emerging as a significant player in the trillion-yuan market, with over 260 related enterprises and more than 1,500 high-quality productions achieving over 500 million views within 24 hours of release [1][2][3] Group 1: Industry Growth and Achievements - The short drama "He Ku Xiang Si Zhu Yu Nian," produced by Nanjing Baichuan Cultural Technology Co., surpassed 500 million views in 24 hours, marking it as a blockbuster [2] - The industry has seen a user base of 662 million in China by the end of last year, surpassing that of food delivery and ride-hailing services, with a market size exceeding 50.4 billion yuan [2] - Nanjing's micro-short drama sector has generated revenue of 4 billion yuan from 2022 to 2024, with a complete industry chain established from IP incubation to film production and precise distribution [3] Group 2: Competitive Advantages - Nanjing's micro-short drama industry benefits from its rich cultural heritage, abundant talent resources, robust industrial ecosystem, digital technology, innovative capabilities, and supportive policies, positioning it as a "hexagonal warrior" in the field [4][5] - The city hosts 54 universities that continuously supply talent in various fields related to film production, including computer science, artificial intelligence, and directing [5] Group 3: Policy and Infrastructure Support - The establishment of the Nanjing Micro-Short Drama Industry Alliance aims to enhance resource integration and address market demands, fostering collaboration among creators, production agencies, and platform operators [6][8] - The alliance will also attract talent, funding, and technology, promoting collaborative development across the industry chain [6] Group 4: Future Directions - The industry is transitioning from "scale expansion" to "quality enhancement," with experts providing insights on policy guidance, industry ecology, data support, and technological applications to navigate this critical transformation [8] - A new service app, "Nanjing 'Ju' Hao," was launched to facilitate access to filming locations, policy support, and other resources, enhancing the operational efficiency of the micro-short drama industry [7]

深度|百家供应商调研:账款支付倡议30天,我们日子更难了

汽车商业评论· 2025-10-20 23:29

Core Viewpoint - The article discusses the challenges and complexities surrounding payment terms in the Chinese automotive supply chain, highlighting the inadequacies of recent policies aimed at improving payment practices and the persistent issues faced by suppliers in receiving timely payments [4][19][55]. Group 1: Policy and Industry Response - The China Automotive Industry Association released the "Supplier Payment Norms Initiative" to address payment issues, but the response from the industry has been mixed, with many suppliers still unaware of their rights and the mechanisms available for complaints [4][5][19]. - A survey revealed that nearly half of the suppliers were unaware of the complaint platform established by the Ministry of Industry and Information Technology, and 88.3% of those aware chose not to file complaints despite facing issues [5][7]. Group 2: Payment Terms and Practices - Most domestic automakers fail to meet the mandated two-month payment term, with suppliers reporting average payment periods of around six months, and some extending up to 2.5 years [7][9]. - The survey indicated that 76.5% of suppliers believe that the implementation of the initiative will be difficult, with many expressing skepticism about the willingness of manufacturers to change their practices [18][19]. Group 3: Supplier Experiences - Suppliers reported that smaller companies often face worse payment terms compared to larger firms, with 80% of small suppliers indicating payment periods exceeding six months [12][15]. - The payment methods predominantly used by suppliers include bank acceptance bills and commercial acceptance bills, with cash payments being rare [11][17]. Group 4: Variability Among Different Types of Automakers - Overseas and joint venture automakers generally offer better payment terms compared to state-owned enterprises, with foreign companies averaging a payment cycle of 56 days, while domestic companies average 168 days [30][31]. - Some suppliers noted that while certain state-owned enterprises have improved their payment practices, many private companies remain problematic, with 52.9% of suppliers expressing dissatisfaction with their payment terms [32][33]. Group 5: Structural Issues in Payment Processes - The article highlights a complex payment structure where the actual payment cycle can exceed nine months due to delays in invoice processing and acceptance [20][23]. - Many suppliers reported that the lack of transparency in acceptance processes and arbitrary changes to acceptance standards contribute to prolonged payment cycles [23][25]. Group 6: Financial Instruments and Their Implications - The use of electronic debt certificates (X-chain) has become prevalent, allowing automakers to extend payment periods while suppliers face high costs to access their funds [44][50]. - The article emphasizes that while policies exist to protect suppliers, the enforcement and practical application of these policies remain weak, leading to continued exploitation of suppliers by larger automakers [28][55].

东盟及中日韩政产研人士赴浙江 共探人工智能新发展

Zhong Guo Xin Wen Wang· 2025-10-20 13:37

Group 1 - The core focus of the ASEAN-China-Japan-South Korea (10+3) Digital Economy Training Program is to enhance mutual learning and cooperation in the fields of digital economy and artificial intelligence among participating countries [1][2]. - The training program includes nearly 50 participants from various ASEAN countries, covering government, industry, and academic sectors, and aims to deepen collaboration and shared development in the digital economy [2][3]. - The program is part of China's initiative to train 1,000 digital talents for ASEAN countries over three years, with Zhejiang University having already trained nearly 200 participants in the past two years [2]. Group 2 - The training program is organized by Zhejiang University and supported by various governmental and academic institutions, highlighting the importance of regional cooperation in digital transformation [3][6]. - The curriculum focuses on artificial intelligence, digital economy, Internet of Things, digital infrastructure, and digital regulation, featuring experts from top universities and organizations [6]. - Participants will engage in case studies and site visits to leading companies in the digital sector, such as Alibaba Cloud and Tencent, to understand practical applications of digital technologies in governance and industry [6].

广交会遇上AI新叙事:中企出海抢抓技术普惠化新风口

2 1 Shi Ji Jing Ji Bao Dao· 2025-10-20 08:30

Core Insights - The 138th Canton Fair AI Trade Ecological Development Forum was held, focusing on the theme of "New Outbound, New Ecology, New Momentum - AI Trade Ecological Builders" [1] - The forum highlighted the integration of AI technology in global trade, emphasizing its role in enhancing efficiency and creating new business models in foreign trade [2] Group 1: AI Integration in Trade - AI technology is increasingly being adopted by foreign trade enterprises in China, with a significant focus on improving operational efficiency [2] - The forum discussed the three major trends in AI and trade: deeper technological integration, closer ecological collaboration, and more inclusive value creation [2] - A report titled "Artificial Intelligence International Trade Application Guide" was released, showcasing the latest practices in AI technology reshaping international trade rules [1][2] Group 2: Industry Growth and Trends - The number and scale of AI enterprises in China have been growing, with domestic models leading in global open-source community downloads [2] - AI is enhancing productivity and product capabilities in cross-border e-commerce, with a mature ecosystem of AI service providers emerging across the entire supply chain [2][3] - The integration of AI in cross-border e-commerce is accelerating, impacting various aspects such as marketing, customer service, and supply chain management [3] Group 3: Collaborative Ecosystem - There is a consensus on the need to build a competitive new ecosystem that integrates technology, quality, and service, emphasizing the importance of collaboration among government, enterprises, academia, and research [4] - The integration of supply chain resources and e-commerce platform advantages is seen as a key breakthrough for the development of AI in international trade [4] - The forum aims to continue exploring the application of AI technology across the entire international trade chain to enhance global competitiveness for Chinese enterprises [4]

应用材料公司技术项目总监 Dustin Ho 博士确认演讲 | 2025异质异构集成年会(HHIC 2025)

势银芯链· 2025-10-20 08:12

Core Viewpoint - The article discusses the upcoming 2025 Heterogeneous Integration Annual Conference, focusing on the theme of "Focusing on the Frontier of Heterogeneous Integration Technology, Advancing the Journey of Advanced Packaging" to promote the development of the advanced electronic information industry in Ningbo and the Yangtze River Delta region [18][20]. Group 1: Conference Details - The conference will take place from November 17-19, 2025, at the Nanyuan Wanghai Hotel in Zhenhai District, Ningbo [22]. - The event is organized by the Yongjiang Laboratory and TrendBank, with support from the Ningbo Electronic Industry Association [22]. - The expected attendance is between 300 to 500 participants [22]. Group 2: Key Themes and Topics - The conference will cover core technologies related to multi-material heterogeneous integration and optoelectronic fusion, focusing on advanced packaging technologies such as 2.5D/3D heterogeneous integration, optical-electrical co-packaging, and wafer-level bonding [20]. - Notable topics include the challenges and trends in heterogeneous integration processes, materials equipment, and the development of advanced packaging solutions [14][20]. Group 3: Featured Speakers and Presentations - Dr. Dustin Ho, Technical Project Director at Applied Materials, will present on "The Application of New Optical Waveguide Technology in Silicon Photonics/CPO" [2]. - Various industry experts will discuss topics such as AI-driven opportunities in chip integration, micro-nano device applications, and the latest advancements in optical technology [14][15][16]. Group 4: Background and Industry Context - The conference aims to address the stringent requirements for chip design and manufacturing driven by applications in artificial intelligence, smart driving, and high-performance computing [18]. - As traditional Moore's Law approaches its physical limits, heterogeneous integration is identified as a crucial and promising direction in the semiconductor field [19].

万咖壹联董事长获“景贤人才” 将深化“AI+出海”双轮战略布局

Zheng Quan Shi Bao Wang· 2025-10-20 01:09

Core Insights - WanKa YiLian (1762.HK) Chairman Gao Di Nan received the "Jingxian Talent" award at the 2025 Jingxian Talent Conference, recognizing contributions in technology innovation and industry development [1] - The company reported a revenue of 1.712 billion yuan in the first half of 2025, marking a 39% year-on-year increase, with overseas revenue growing over 400% [1] - WanKa YiLian signed a comprehensive cooperation memorandum with Alibaba Cloud to develop "AI Marketing Intelligent Body" and "AI Mobile Intelligent Body," aiming to create a global AI+marketing ecosystem [2] Group 1 - The "Jingxian Plan 2.0" was launched to support and encourage talent innovation and entrepreneurship in Shijingshan District [1] - The company has expanded its business from Android to Apple iOS and Huawei HarmonyOS, evolving from a distribution tool to a comprehensive marketing solution [1] - The partnership with Alibaba Cloud focuses on integrating AI large models and cloud computing to enhance advertising efficiency and return on investment (ROI) [2] Group 2 - WanKa YiLian aims to deepen its innovation in AI and mobile ecosystem integration, responding to the dual-driven strategy of "technology innovation + industry development" [3] - The company plans to strengthen its "AI + overseas" strategy, solidifying its innovation barriers and cultivating new growth engines in the AI mobile era [3] - Future efforts will focus on enhancing technological research and ecological collaboration to build a more open, intelligent, and sustainable digital ecosystem [3]

2025年中国基础云服务行业数据报告

艾瑞咨询· 2025-10-20 00:06

Core Insights - The overall cloud service market in China is projected to reach 544.54 billion yuan in 2024, with a growth rate of 15%. The rapid development of artificial intelligence (AI) is a key driver for the growth of cloud infrastructure and capability platforms [1][8][19]. Market Overview - The IaaS market is expected to grow to 371.86 billion yuan in 2024, with a growth rate of 19.1%. The PaaS market is projected to reach 101.86 billion yuan, growing at 35.8% [11]. - The public cloud service market is anticipated to reach 387.87 billion yuan in 2024, with an 18% growth rate [13]. - The non-public cloud service market is expected to grow to 163.58 billion yuan, with an 11.2% growth rate [16]. Market Characteristics - AI has become a focal point for the construction and business layout of the cloud service industry. Participants are expanding investments in intelligent computing infrastructure and improving AI development tools [8][11]. - The public cloud service market is experiencing new opportunities due to the rapid development of AI, particularly in sectors like government, finance, manufacturing, and energy [19]. Competitive Landscape - In the public cloud IaaS market, Alibaba Cloud, Huawei Cloud, and Tianyi Cloud rank as the top three providers, with Tencent Cloud and Mobile Cloud tied for fourth place, followed by Amazon Web Services [19]. - Operator-backed cloud vendors are enhancing their market competitiveness by improving infrastructure and increasing investments in AI, while internet-based cloud vendors are focusing on business streamlining and capability concentration to alleviate competitive pressure [19]. Development Trends - The cloud computing sector is expected to continue supporting the development of the AI industry by providing foundational resources and platform tools. There will be a deepening integration of cloud and intelligence, leading to upgrades in intelligent computing [8][11]. - In the short term, the market competition will be characterized by price wars, while in the long term, the rapid iteration of technology capabilities will expand business scenarios and drive demand for cloud services [13][16].

阿里云AI成果入选顶会,可让GPU用量削减82%;优必选再爆亿元大单|数智早参

Mei Ri Jing Ji Xin Wen· 2025-10-19 23:16

Group 1 - Alibaba Cloud's Aegaeon solution has been selected for the prestigious academic conference SOSP 2025, addressing GPU resource waste in AI model services and achieving an 82% reduction in GPU usage, thereby lowering hardware costs [1] - The Aegaeon technology has been applied to the Bailian platform, allowing single GPU services to support multiple models and enhancing throughput [1] Group 2 - UBTECH has secured a major contract worth 126 million yuan for the procurement and installation of humanoid robots, bringing the total order amount for the Walker series to over 630 million yuan for the year [2] - The humanoid robot market is experiencing rapid growth, with increasing demand across various sectors including industrial production, service industries, education, and home entertainment [2] Group 3 - An semiconductor company in Dongguan plans to implement a "four days on, three days off" work schedule due to supply chain disruptions and product shortages following government intervention [3] - The parent company is taking measures to stabilize the domestic supply chain to meet customer demands amid rising product prices and shortages [3]