焦炭

Search documents

广发期货《黑色》日报-20251022

Guang Fa Qi Huo· 2025-10-22 01:43

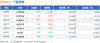

免责声明 本报告中的信息均来源于被广发期货有限公司认为可称的已公开资料,但广发期货时这些信息的准确性及完整性不作任何保证。本报告反映研究人员的不同观点、见解及 分析方法,并不代表广发期货或其附属机构的立场。在任何情况下,报告内审仅供参考,报告中的信息或所表达的急见开不勾成所述品种买卖的出价或询价,投资器比 投资,风险自担。本报告旨在发送给广发明货特定客户及其他专业人士,版权归广发期货所有,未经广发期货节面授权,任何人不得对本报告进行任何形式的发布、复制 。如引用、刊发,需注明出处为"广发期货"。 | 材产业期现日报 | 投资咨询业务资格:证监许可 【2011】1292号 | | | | | | | --- | --- | --- | --- | --- | --- | --- | | 2025年10月22日 | | | | 周敦波 | Z0010559 | | | 钢材价格及价差 | | | | | | | | 品种 | | 现值 | 前目 | 狱跌 | 基差 | 单位 | | 螺纹钢现货(华东) | | 3200 | 3200 | O | 153 | | | 螺纹钢现货(华北) | | 3110 | 311 ...

焦炭板块10月21日跌0.86%,安泰集团领跌,主力资金净流出3.76亿元

Zheng Xing Xing Ye Ri Bao· 2025-10-21 08:28

Core Insights - The coke sector experienced a decline of 0.86% on October 21, with Antai Group leading the losses [1] - The Shanghai Composite Index closed at 3916.33, up 1.36%, while the Shenzhen Component Index closed at 13077.32, up 2.06% [1] Sector Performance - Key stocks in the coke sector showed mixed performance, with Yunmei Energy rising by 3.44% and Antai Group falling by 7.34% [1] - The trading volume for Yunmei Energy was 1.5663 million shares, while Antai Group had a trading volume of 2.7398 million shares [1] Capital Flow - The coke sector saw a net outflow of 376 million yuan from main funds, while retail investors contributed a net inflow of 158 million yuan [1] - The detailed capital flow indicates that major funds withdrew from several stocks, including Antai Group and Shanxi Coking, while retail investors showed interest in stocks like Yunmei Energy and Meijin Energy [2]

焦炭板块10月20日涨6.02%,陕西黑猫领涨,主力资金净流入5.08亿元

Zheng Xing Xing Ye Ri Bao· 2025-10-20 08:37

Core Insights - The coke sector experienced a significant increase of 6.02% on October 20, with Shaanxi Black Cat leading the gains [1] - The Shanghai Composite Index closed at 3863.89, up 0.63%, while the Shenzhen Component Index closed at 12813.21, up 0.98% [1] Sector Performance - Shaanxi Black Cat (601015) closed at 4.24, with a rise of 10.13% and a trading volume of 1.5557 million shares, amounting to a transaction value of 632 million yuan [1] - Antai Group (600408) closed at 3.27, up 10.10%, with a trading volume of 2.8265 million shares [1] - Baotailong (601011) closed at 4.40, increasing by 10.00%, with a trading volume of 4.7728 million shares, resulting in a transaction value of 2.059 billion yuan [1] - Yunmei Energy (600792) closed at 4.65, up 9.93%, with a trading volume of 508,000 shares [1] - Shanxi Coking Coal (600740) closed at 4.34, increasing by 4.58%, with a trading volume of 803,700 shares [1] - Meijin Energy (000723) closed at 5.01, up 3.09%, with a trading volume of 1.404 million shares [1] - Yunwei Co. (600725) closed at 3.75, increasing by 2.74%, with a trading volume of 520,200 shares [1] Capital Flow - The coke sector saw a net inflow of 508 million yuan from main funds, while retail funds experienced a net outflow of 340 million yuan [1] - The detailed capital flow for individual stocks indicates that Baotailong had a net inflow of 254 million yuan from main funds, while it faced a net outflow of 132 million yuan from retail investors [2] - Shaanxi Black Cat had a net inflow of 104 million yuan from main funds, but also saw a net outflow of approximately 90 million yuan from retail investors [2] - Yunmei Energy recorded a net inflow of 81.515 million yuan from main funds, with a net outflow of around 39 million yuan from retail investors [2] - Meijin Energy had a net inflow of 56.43 million yuan from main funds, while retail investors experienced a net outflow of about 5.12 million yuan [2]

《黑色》日报-20251020

Guang Fa Qi Huo· 2025-10-20 08:07

Group 1: Steel Industry Industry Investment Rating No investment rating information is provided in the steel industry report. Core Viewpoints - After the holiday, the apparent demand for steel has recovered, but there was significant inventory accumulation in the plate market. Steel mills need to cut production to ease inventory pressure, and the price decline has already factored in the expected supply surplus. The carbon element cost on the cost side is supported, while the iron element cost may decline due to the expected drop in molten iron. Steel prices have fallen significantly, compressing steel mill profits. It is recommended to wait and see on single - side trades. The January contracts for rebar and hot - rolled coils are expected to stabilize around 3000 and 3200 yuan respectively and enter a sideways consolidation trend. Given the expected reduction in coal mine production and the strengthening of thermal coal, the carbon element is stronger than the iron element. A long - carbon and short - iron arbitrage can be considered, such as a long - coking coal and short - hot - rolled coil operation. The spread between hot - rolled coils and rebar is expected to continue to narrow [1]. Summary by Directory - **Steel Prices and Spreads**: Rebar and hot - rolled coil prices showed mixed trends in different regions and contracts. For example, the spot price of rebar in East China increased by 10 yuan/ton to 3200 yuan/ton, while the 01 contract price decreased by 12 yuan/ton to 3037 yuan/ton. The spot price of hot - rolled coils in East China decreased by 10 yuan/ton to 3270 yuan/ton, and the 01 contract price decreased by 15 yuan/ton to 3204 yuan/ton [1]. - **Cost and Profit**: The billet price remained unchanged at 2920 yuan, and the slab price was stable at 3730 yuan. The cost of Jiangsu electric - arc furnace rebar decreased by 7 yuan to 3300 yuan, while the cost of Jiangsu converter rebar increased by 13 yuan to 3153 yuan. Profits in different regions and for different products showed varying degrees of decline [1]. - **Production and Inventory**: The daily average molten iron output decreased by 0.6 to 240.9, a decline of 0.3%. The output of five major steel products decreased by 6.4 to 857.0, a decline of 0.7%. The inventory of five major steel products decreased by 18.5 to 1582.3, a decline of 1.2%. The rebar inventory decreased by 18.6 to 641.1, a decline of 2.8%, while the hot - rolled coil inventory increased by 6.3 to 419.2, an increase of 1.5% [1]. - **Transaction and Demand**: The building materials trading volume decreased by 0.7 to 9.5, a decline of 6.7%. The apparent demand for five major steel products increased by 124.0 to 875.4, an increase of 16.5%. The apparent demand for rebar increased by 66.6 to 219.8, an increase of 43.5%, and the apparent demand for hot - rolled coils increased by 20.5 to 315.6, an increase of 7.0% [1]. Group 2: Iron Ore Industry Industry Investment Rating No investment rating information is provided in the iron ore industry report. Core Viewpoints - Last week, iron ore futures continued to decline in a sideways trend. On the supply side, the global iron ore shipment volume decreased, and the arrival volume at 45 ports increased. On the demand side, the steel mill profit margin declined slightly, the molten iron output decreased from a high level, and the steel mill replenishment demand weakened. In the future, due to the weak operation of steel prices, the steel mill profitability will continue to decline, and the weak demand will force iron ore to operate weakly. The iron ore market is shifting from a state of slightly tight balance to oversupply. It is recommended to wait and see on single - side trades, with a reference range of 730 - 800. An arbitrage strategy of long - coking coal and short - iron ore is recommended, and it is advisable to buy out - of - the - money put options on the 2601 iron ore contract at high prices [4]. Summary by Directory - **Prices and Spreads**: The warehouse receipt costs of some iron ore varieties decreased slightly, while the 01 - contract basis of some varieties increased. The 5 - 9 spread increased by 0.5 to 21.5, an increase of 2.4%, and the 1 - 5 spread decreased by 0.5 to 21.0, a decrease of 2.3% [4]. - **Supply and Demand**: The weekly arrival volume at 45 ports increased by 437.1 to 3045.8, an increase of 16.8%, and the global weekly shipment volume decreased by 71.5 to 3207.5, a decrease of 2.2%. The weekly average molten iron output of 247 steel mills decreased by 0.6 to 241.0, a decrease of 0.2%, and the weekly average port clearance volume at 45 ports decreased by 20.7 to 315.7, a decrease of 6.1% [4]. - **Inventory**: The 45 - port inventory increased by 192.1 to 14278.27, an increase of 1.4%, and the imported iron ore inventory of 247 steel mills decreased by 63.5 to 8982.7, a decrease of 0.7% [4]. Group 3: Coking Coal and Coke Industry Industry Investment Rating No investment rating information is provided in the coking coal and coke industry report. Core Viewpoints - **Coke**: Last week, coke futures showed a sideways upward trend. The spot market had a second - round price increase proposed by mainstream coking enterprises. On the supply side, coking production decreased due to losses. On the demand side, the molten iron output of steel mills decreased from a high level, steel prices weakened, and steel mill profits declined. In the inventory aspect, coking plants and steel mills reduced inventory, while ports accumulated inventory. Recently, production cuts at Mongolian coal mines, rising prices in Shanxi auctions, and the impact of mine accidents have led to concerns about supply, causing coal - coke prices to rebound from the bottom. Speculative investors are advised to go long on the 2601 coke contract at low prices, with a reference range of 1650 - 1800, and an arbitrage strategy of long - coking coal and short - coke can be considered [6]. - **Coking Coal**: Last week, coking coal futures also showed a sideways upward trend. The spot price in Shanxi recovered, and the prices of some coal types rebounded significantly. After the holiday, the domestic coking coal market began to rebound after a slight decline. On the supply side, although main - producing area coal mines resumed production after the holiday, recent mine accidents have led to expectations of supply reduction. On the demand side, the molten iron output decreased slightly, and coking plant operations decreased slightly but remained at a relatively high level. In the inventory aspect, coal mines, coal - washing plants, coking plants, and steel mills accumulated inventory, while ports and border crossings reduced inventory. It is recommended to go long on the 2601 coking coal contract at low prices in the short term, with a reference range of 1150 - 1300, and an arbitrage strategy of long - coking coal and short - coke can be considered [6]. Summary by Directory - **Prices and Spreads**: For coke, the price of Shanxi quasi - first - grade wet - quenched coke (warehouse receipt) remained unchanged at 1561 yuan, and the 01 - contract price increased by 4 yuan to 1676 yuan. For coking coal, the price of Shanxi medium - sulfur primary coking coal (warehouse receipt) remained unchanged at 1300 yuan, and the 01 - contract price decreased by 7 yuan to 1179 yuan [6]. - **Supply**: The daily average output of all - sample coking plants decreased by 0.8 to 65.3, a decrease of 1.3%, and the daily average output of 247 steel mills decreased by 0.6 to 241.0, a decrease of 0.2%. The weekly output of Fenwei sample coal mines increased, with the raw coal output increasing by 18.2 to 854.9, an increase of 2.2%, and the clean coal output increasing by 11.8 to 438.2, an increase of 2.8% [6]. - **Demand**: The molten iron output of 247 steel mills decreased by 0.6 to 241.0, a decrease of 0.2%. The daily average output of all - sample coking plants decreased by 0.8 to 65.3, a decrease of 1.3%, and the daily average output of 247 steel mills decreased by 0.6 to 241.0, a decrease of 0.2% [6]. - **Inventory**: The total coke inventory decreased by 17.9 to 891.9, a decrease of 2.0%. The coking coal inventory of Fenwei coal mines decreased, while the coking coal inventory of all - sample coking plants, 247 steel mills, and the available days increased to varying degrees [6].

煤焦周度报告20251020:现货成交有所改善,双焦震荡偏强运行-20251020

Zheng Xin Qi Huo· 2025-10-20 07:01

1. Report Industry Investment Rating - Not provided in the content 2. Core Viewpoints of the Report - Last week, the spot transaction of coking coal improved. With the news of the upcoming central safety production assessment and inspection in 2025 and better - than - expected steel production reduction and inventory depletion data, both coking coal and coke fluctuated strongly. As of Friday's close, the coke 01 contract rose 0.87% to 1676, and the coking coal 01 contract rose 1.2% to 1179 [8]. - In the context of anti - involution expectations and over - production inspection policies, there are continuous disturbances on the supply side of coal mines. Pig iron production remains at a high level, and the spot transaction of coking coal is acceptable. The upward space of coking coal depends on the macro situation and the sustainability of steel inventory depletion. It is recommended to wait and see on a single - side basis and continue to pay attention to the reverse spread of coking coal 1 - 5. In the long term, coking coal maintains a bullish outlook under the expectations of a strict macro environment and coal mine safety supervision [8]. 3. Summary According to the Directory 3.1 Coke 3.1.1 Price - Last week, the futures market fluctuated strongly. The second - round price increase of spot coke started but has not been implemented yet. The spot price remained stable, and attention should be paid to this week's macro and steel data. The freight for coke transportation remained stable [6][9][16]. - The coke 01 contract rose 0.87% to 1676 as of Friday's close [8]. 3.1.2 Supply - Profit compression and production reduction in some coking plants led to a slight tightening of coke supply. As of October 17, the capacity utilization rate of all - sample independent coking enterprises was 74.24%, a decrease of 0.94 percentage points from the previous week, and the daily average coke output was 65.29 tons, a decrease of 0.83 tons from the previous week. The capacity utilization rate of 247 steel mills' coking plants was 84.72%, a decrease of 0.81 percentage points from the previous week, and the daily average coke output was 45.94 tons, a decrease of 0.44 tons from the previous week [27][32]. 3.1.3 Demand - Pig iron production remained at a high level, providing strong support for raw material demand. However, after the holiday, due to logistics, weather and other reasons, the inventory - building pace of steel mills was slow. As of October 17, the blast furnace start - up rate of 247 sample steel mills was 84.27%, unchanged from the previous week; the capacity utilization rate was 90.33%, a decrease of 0.02 percentage points from the previous week; the daily average pig iron output was 240.95 tons, a decrease of 0.07 tons from the previous week; and the profitability rate of steel mills was 55.41%, a decrease of 3.46 percentage points from the previous week [35]. - Speculative sentiment was average, export profit changed little, and the daily trading volume of building materials was lower than the same period in previous years [37]. 3.1.4 Inventory - Both upstream and downstream reduced their inventories, and the total inventory decreased. As of October 17, the total coke inventory decreased by 17.87 tons to 891.88 tons compared with the previous week. Among them, the port inventory increased by 0.06 tons to 195.15 tons, the inventory of all - sample independent coking enterprises decreased by 6.55 tons to 57.29 tons, and the inventory of 247 sample steel mills decreased by 11.38 tons to 639.44 tons [42][45]. 3.1.5 Profit - The profitability of coking enterprises was compressed, and the futures market profit of coke weakened slightly. The average profit per ton of 30 independent coking enterprises was - 13 yuan/ton, a decrease of 22 yuan from the previous week. The futures market profit of coke 01 decreased by 9.4 yuan/ton to 143.3 yuan/ton compared with the previous week [53]. 3.1.6 Valuation - The premium of coke 01 increased, and the 1 - 5 spread fluctuated. The basis of coke 01 decreased by 44.3 to - 81.86 compared with the previous week, and the 1 - 5 spread increased by 4 to - 148 compared with the previous week [57]. 3.2 Coking Coal 3.2.1 Price - Last week, the futures market fluctuated strongly, and it is expected to maintain a strong trend in the short term. Most of the spot prices increased [60][63]. - The coking coal 01 contract rose 1.2% to 1179 as of Friday's close [8]. 3.2.2 Supply - The supply from production areas continued to recover, the output of coal washing plants was basically flat, the daily customs clearance vehicle number at the Mongolian Ganqimaodu Port has recovered to over 1200 vehicles, and the year - on - year decline in imported coking coal from January to August 2025 narrowed [66][74]. - As of October 17, the capacity utilization rate of 314 sample coal washing plants was 35.79%, an increase of 0.47 percentage points from the previous week, and the daily average clean coal output was 26.11 tons, an increase of 0.45 tons from the previous week [71]. 3.2.3 Inventory - Downstream enterprises replenished their inventories appropriately, coal mines did not accumulate obvious inventories, and the total inventory increased. As of October 17, the total coking coal inventory increased by 42.95 tons to 2554.22 tons compared with the previous week. Among them, the inventory of mining enterprises increased by 9.55 tons to 205.41 tons, the port inventory decreased by 22.28 tons to 272.71 tons, the clean coal inventory of coal washing plants increased by 10.18 tons to 290.41 tons, the inventory of all - sample independent coking enterprises increased by 38.31 tons to 997.37 tons, and the inventory of 247 sample steel mills increased by 7.19 tons to 788.32 tons [77][80]. 3.2.4 Valuation - The basis of coking coal 01 weakened, and the 1 - 5 spread strengthened slightly. The basis of coking coal 01 decreased by 33 to 8 compared with the previous week, and the 1 - 5 spread increased by 14 to - 82.5 compared with the previous week [101].

黑色建材周报:补库需求回暖,价格偏强震荡-20251019

Hua Tai Qi Huo· 2025-10-19 12:15

Report Summary 1. Investment Ratings - **Coking coal**: Oscillation [3] - **Coke**: Oscillation [3] - **Cross - variety**: None [3] - **Spot - futures**: None [3] - **Options**: None [3] 2. Core Views - In the coking coal market, influenced by the continuous price increase of coal, the short - term replenishment demand from downstream and mid - stream has increased. Meanwhile, safety inspections in the northern regions have become stricter, leading to a price rebound. After the thermal coal price stabilizes, opportunities for shorting coking coal should be monitored [2]. - In the coke market, affected by the rising price of thermal coal, the price of raw coal has increased, and the enthusiasm for replenishment from mid - and downstream has grown. However, as steel mill profits have shrunk significantly, steel mills are strongly resistant, intensifying the game between coking plants and steel mills. The price of coke is oscillating widely, with an upper limit due to the expected steel mill production cuts and a lower limit supported by the rising coal prices [2]. 3. Summary by Directory Price and Spread - As of the close this Friday, the coke 2601 contract closed at 1,676 yuan/ton, a 0.57% increase from last week. The coking coal 2601 contract closed at 1,179 yuan/ton, a 1.55% increase from last week. Affected by factors such as the post - National Day demand recovery, prices are oscillating strongly [1][5]. Supply - This week, the daily average coke production of independent coking enterprises in the Mysteel sample was 521,800 tons, a decrease of 6,800 tons from last week. The capacity utilization rate was 73.99%, a 0.96% decrease from last week [1][25]. Demand - According to Mysteel's research, the blast furnace operating rate of 247 steel mills was 84.27%, unchanged from last week and 2.59 percentage points higher than last year. The blast furnace iron - making capacity utilization rate was 90.33%, a 0.22 - percentage - point decrease from last week but 2.34 percentage points higher than last year. The steel mill profitability rate was 55.41%, a 0.87 - percentage - point decrease from last week and 19.05 percentage points lower than last year. The daily average pig iron output was 240,950 tons, a decrease of 590 tons from last week but an increase of 6,590 tons compared to last year [1][33]. Inventory - The coke inventory of 247 steel mills was 595,080 tons, a decrease of 3,290 tons from last week. The coking coal inventory of 247 steel mills was 751,870 tons, a decrease of 14,580 tons from last week. Independent coking enterprises had a slight inventory reduction; the total coking coal inventory of the full - sample independent coking enterprises was 829,780 tons, a decrease of 17,210 tons from last week [1][34].

焦炭板块10月17日跌0.44%,美锦能源领跌,主力资金净流出3.39亿元

Zheng Xing Xing Ye Ri Bao· 2025-10-17 08:37

Core Viewpoint - The coke sector experienced a decline of 0.44% on October 17, with Meijin Energy leading the drop. The Shanghai Composite Index closed at 3839.76, down 1.95%, while the Shenzhen Component Index closed at 12688.94, down 3.04% [1] Group 1: Market Performance - The coke sector's individual stock performance varied, with An Tai Group seeing a significant increase of 10.00% to a closing price of 2.97 [1] - Other notable performances included Yunmei Energy, which rose by 2.67% to 4.23, and Baotailong, which increased by 1.27% to 4.00 [1] - Conversely, Meijin Energy fell by 2.80% to 4.86, while Shanxi Coking Coal decreased by 0.72% to 4.15 [1] Group 2: Trading Volume and Capital Flow - The total trading volume for the coke sector was significant, with An Tai Group trading 1.9851 million shares and a transaction value of 5.83 million yuan [1] - The sector experienced a net outflow of 339 million yuan from main funds, while retail investors contributed a net inflow of 241 million yuan [1] - Speculative funds saw a net inflow of 98.38 million yuan, indicating varied investor sentiment within the sector [1]

美锦能源跌2.20%,成交额3.05亿元,主力资金净流出4038.10万元

Xin Lang Cai Jing· 2025-10-17 05:48

Core Viewpoint - Meijin Energy's stock price has shown fluctuations, with a year-to-date increase of 8.43% but a recent decline of 2.20% on October 17, 2023, indicating potential volatility in the market [1] Company Overview - Meijin Energy, established on January 8, 1997, and listed on May 15, 1997, is located in Taiyuan, Shanxi Province. The company primarily engages in the production and sales of coal, coke, natural gas, and hydrogen fuel cell vehicles, with 97.45% of its revenue coming from coal and coke products [1][2] - As of June 30, 2025, Meijin Energy reported a revenue of 8.245 billion yuan, a year-on-year decrease of 6.46%, and a net profit attributable to shareholders of -674 million yuan, reflecting a growth of 1.29% [2] Stock Performance - As of October 17, 2023, Meijin Energy's stock was trading at 4.89 yuan per share, with a total market capitalization of 21.533 billion yuan. The stock has experienced a trading volume of 305 million yuan and a turnover rate of 1.40% [1] - The stock has appeared on the "Dragon and Tiger List" twice this year, with the most recent instance on July 10, 2023, where it recorded a net purchase of 50.3192 million yuan [1] Shareholder Information - As of June 30, 2025, Meijin Energy had 248,700 shareholders, a decrease of 5.77% from the previous period. The average number of circulating shares per person increased by 6.12% to 17,679 shares [2][3] - The top ten circulating shareholders include significant institutional investors, with notable increases in holdings from Guotai Zhongxin Coal ETF and Southern CSI 500 ETF [3]

中信期货晨报:国内商品期货多数上涨,新能源材料涨幅居前-20251017

Zhong Xin Qi Huo· 2025-10-17 01:56

Report Industry Investment Rating - Not provided in the given content Core View of the Report - Next week, there is a risk of increased volatility in global major asset classes. Investors are advised to maintain a strategic allocation to precious metals such as gold and be relatively cautious about risk assets like equities, waiting and seeing. In the medium - term of the fourth quarter, the basic allocation view of equities > commodities > bonds is still held, and attention can be paid to potential buying opportunities for equity assets after the turmoil subsides [6] Summary by Related Catalogs Market Performance Summary - **Financial Market**: In the stock index futures, technology events catalyze the active growth style; the market turnover of index options slightly declines; the bond market of treasury bond futures remains weak. For example, the current price of CSI 300 futures is 4,590 with a daily increase of 0.30%, and the 2 - year treasury bond futures price is 102.362 with a daily decrease of 0.02% [2][7] - **Commodity Market**: Precious metals like COMEX gold and silver have significant increases, with COMEX gold rising 1.57% daily and COMEX silver rising 4.69% daily. In the energy sector, NYMEX WTI crude oil and ICE Brent oil have daily increases of 0.27% and 0.31% respectively, but have declined this year. In the agricultural products sector, CBOT soybeans and other varieties show different trends [2] - **Shipping Market**: The freight rate of container shipping to Europe is under pressure, with a monthly decline of 3.37% [3] Macro - situation Analysis - **Overseas Macro**: Next week, attention should be paid to new tariff threats from Trump and the marginal changes in the US government shutdown. There is a risk of conflict escalation before the APEC meeting at the end of October. If the US government shutdown exceeds 30 days, it will increase the recession risk [6] - **Domestic Macro**: China will gradually enter the period of focusing on the "15th Five - Year Plan" and tracking incremental policies. The progress and effectiveness of a batch of incremental policies such as 500 billion new policy - based financial instruments are worthy of follow - up [6] Asset Views - **Short - term**: Maintain a strategic allocation to precious metals such as gold, and be cautious about risk assets like equities next week [6] - **Medium - term (Fourth Quarter)**: Hold the basic allocation view of equities > commodities > bonds, and pay attention to potential buying opportunities for equity assets after the turmoil [6] View Highlights - **Financial**: Stock index futures are expected to rise in shock, index options to fluctuate, and treasury bond futures to oscillate [7] - **Precious Metals**: Gold and silver are expected to rise in shock [7] - **Shipping**: Container shipping to Europe is expected to fluctuate [7] - **Black Building Materials**: Most varieties such as steel, iron ore, coke, etc. are expected to oscillate [7] - **Non - ferrous Metals and New Materials**: Most non - ferrous metal varieties are expected to oscillate, and aluminum is expected to rise in shock [7] - **Energy and Chemicals**: Most varieties are expected to decline in shock, and some varieties such as asphalt and high - sulfur fuel oil are expected to oscillate [9] - **Agriculture**: Most varieties are expected to oscillate, and some varieties such as sugar and paper pulp are expected to decline in shock [9]

安泰集团2025年10月17日涨停分析:业绩扭亏+债务重组+游资炒作

Xin Lang Cai Jing· 2025-10-17 01:55

Core Viewpoint - Antai Group (sh600408) reached the daily limit of 10% increase, closing at 2.97 yuan, with a total market capitalization of 2.99 billion yuan, driven by improved financial performance, debt restructuring, and speculative trading [1] Financial Performance - In the first half of 2025, the company achieved a net profit of 5.28 million yuan, a significant turnaround from a loss of 93.01 million yuan in the same period of 2024, indicating a recovery in profitability [1] - The net cash flow from operating activities was 86.26 million yuan, providing support for the stock price increase [1] Debt Restructuring - The company's debt from Minsheng Bank has been transferred to Wuhu Xinjing, and discussions regarding a debt resolution plan are ongoing, alleviating market concerns about the company's debt issues [1] Business Operations - Antai Group primarily engages in the production and sale of coke and section steel products, with additional involvement in coal washing and electricity generation [1] Market Activity - On October 16, 2025, the stock was included in the "Dragon and Tiger List," with a trading volume of 500 million yuan, indicating significant market interest [1] - The total buying amounted to 103 million yuan, while total selling was 85.88 million yuan, suggesting strong speculative trading activity [1] Technical Analysis - Although specific technical indicators were not mentioned, the influx of speculative capital may have helped the stock price break through key resistance levels, attracting further investor interest [1] - Market expectations for improved performance in the upcoming quarterly report may have prompted some investors to position themselves early [1]