欧莱雅

Search documents

深度|673个产品“持证上岗”,防脱赛道迎来两重挑战

FBeauty未来迹· 2025-10-28 13:20

Core Insights - The current market for hair care brands in China is experiencing significant growth, with a clear delineation of brand tiers based on sales thresholds [3][4] - The scalp health market is expanding rapidly, with a projected market size of 600 billion yuan by 2025, reflecting a stable growth rate of around 10% [5] - The anti-hair loss segment is the most competitive area within the hair care market, with the Chinese market expected to reach 300 billion yuan by 2030, accounting for nearly one-third of the overall hair care market [6] Market Dynamics - The hair care market is characterized by high growth, high prices, and low consumer trust, driven by increasingly discerning consumers and tightening industry regulations [11][12] - The demand for anti-hair loss products has evolved from traditional concepts to a more systematic approach to scalp health management, with a younger and more diverse consumer base [12] - Regulatory frameworks are becoming more stringent, requiring anti-hair loss products to meet high standards of proof regarding efficacy and safety [13][14] Competitive Landscape - The market is witnessing a division among brands, with a focus on "certified" products and specialized offerings, as evidenced by the significant number of new certifications issued for anti-hair loss products [17][19] - Major international brands dominate the high-end market, while local brands leverage unique concepts and certifications to differentiate themselves [21] - The competition is shifting towards technological innovation and trust-building, with brands needing to demonstrate clinical validation and effective solutions [23][31] Innovation and Trust - The industry faces challenges related to ingredient efficacy and consumer skepticism, necessitating breakthroughs in formulation and delivery methods [25][28] - Brands are increasingly focusing on establishing trust through transparent communication of product efficacy and user experiences [29][31] - The successful brands in the future will likely be those that can balance technical advancements with consumer trust and emotional connections [31]

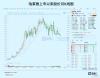

20倍消费大白马,跑不动了

Ge Long Hui· 2025-10-28 10:13

Core Viewpoint - The article highlights the contrasting performance of Proya, a leading domestic beauty brand, which achieved over 10 billion yuan in revenue for the first time while its stock price has significantly declined by over 20% since May and over 40% from its peak in 2023 [1][3][4]. Group 1: Company Performance - Proya's sales during the Double Eleven pre-sale event were strong, with the brand ranking first in the beauty category and achieving over 100 million yuan in sales shortly after the event began [1]. - In the first half of 2025, Proya reported revenue of 5.362 billion yuan, a year-on-year increase of 7.21%, and a net profit of 799 million yuan, up 13.80% [4][5]. - However, the revenue growth rate of Proya in the first half of 2025 is the lowest since its listing in 2017, significantly down from 37.9% in the same period last year [5][8]. Group 2: Brand and Market Dynamics - The main brand Proya, which contributes nearly 80% of the company's revenue, saw a slight decline in revenue of 0.08% to 3.979 billion yuan, marking its first negative growth in five years [9][10]. - Proya's multi-brand strategy, including acquisitions of domestic and international brands, has not significantly improved overall performance, with new brands contributing only 18.4% to total revenue [12][13]. Group 3: Competitive Landscape - The beauty market is becoming increasingly competitive, with other brands like Mao Geping and Marubi showing revenue growth rates above 30%, while Proya's growth has slowed [8][22]. - The overall beauty and skincare market saw a sales increase of 10.1% in the first half of 2025, indicating a shift in market dynamics towards mid-tier brands [22][24]. Group 4: Financial Metrics and Investment - Proya's sales expenses reached 5.161 billion yuan in 2024, accounting for 47.88% of its revenue, while R&D expenses were only 210 million yuan, highlighting a significant imbalance [16]. - The company is facing challenges in maintaining its market position due to high reliance on marketing and low R&D investment, which is critical in a market increasingly focused on product efficacy and ingredients [34][36]. Group 5: Future Outlook - Proya's management has proposed a "Double Ten Strategy" aiming to enter the top ten global cosmetics companies within the next decade, but the company faces significant valuation challenges compared to international giants [19][20]. - The article suggests that Proya must accelerate innovation and reform to realize its potential as a leading brand in the beauty industry [46].

产业前瞻|深度解码银发经济背后的时尚消费变革(下)

Sou Hu Cai Jing· 2025-10-28 06:16

Core Insights - The silver economy, driven by the awakening consumption power of the 50+ demographic, is emerging as a significant growth engine for the fashion, beauty, and health industries over the next decade [5][9][20] - The shift in societal perceptions of beauty is leading to a broader acceptance of aging, allowing brands to tap into a wider market potential [10][12] - The need for brands to adapt their strategies to cater to the 50+ demographic is becoming a critical question for all fashion brands [9][12] Industry Trends - The rise of the silver economy is not just a niche market but a strategic restructuring of the mainstream market [9][12] - Brands are encouraged to move away from a singular focus on youthfulness and instead create an "all-age adaptable" system [12][20] - The fashion industry must consider both functionality and style in their designs, catering to the needs of older consumers while maintaining aesthetic appeal [12][20] Consumer Behavior - The silver demographic seeks recognition as vibrant modern consumers, rejecting age-related stereotypes [10][17] - There is a growing demand for products that are not only anti-aging but also cater to the diverse needs of different segments within the silver population [13][15] - Emotional resonance and cross-generational engagement are becoming essential in marketing strategies [20][21] Strategic Recommendations - Brands should implement AI-driven strategies to create modular designs that cater to both younger and older consumers [16][20] - Retail experiences need to shift from transaction-focused to long-term engagement, fostering community and support for the silver demographic [15][20] - Marketing strategies should leverage dual-track approaches to reach both younger and older audiences effectively [20][21]

联合利华刮骨疗毒:裁员7500人、剥离梦龙,中国市场成转型试金石

3 6 Ke· 2025-10-28 04:00

Core Insights - Unilever is undergoing a significant transformation, marked by layoffs, divestitures, and executive changes, with the Chinese market serving as a critical testing ground for its strategic shift [1][2] Financial Performance - In the first three quarters of the year, Unilever reported revenues of €44.8 billion, a year-on-year decline of 3.3%, with Q3 sales at €14.7 billion, down 3.5% [1] - All five core business segments experienced negative growth, with home care leading at a 5.3% decline, followed by ice cream at 4.2%, and beauty, health, and food segments each declining around 3% [1] - The Americas market saw a significant drop of 5.1%, while Europe achieved a modest growth of 1.9%. In contrast, Indonesia and China showed signs of recovery, with China's Q3 sales returning to low single-digit growth [1][6] Strategic Reforms - CEO Alan Fernandis initiated aggressive reforms, focusing on cutting inefficient businesses, enhancing brand premiumization and innovation, and strengthening digital capabilities [2] - A major workforce reduction is planned, with 7,500 jobs cut, representing 5.9% of the total workforce, and a quarter of the top 200 executives will be replaced, aiming for annual cost savings of $800 million [2] Business Divestitures - Unilever has been actively divesting underperforming brands, including the sale of the water purifier brand Pureit and over 20 beauty brands, as well as the separation of its ice cream business, which has been rebranded as "Dream Ice Cream Company" [3] - The ice cream segment, which holds a 21% market share globally, is projected to generate €7.9 billion in revenue for 2024. In China, it ranks second in market share, trailing behind Yili [3] Market Adaptation - The Dream Ice Cream Company plans to innovate in market engagement, adopt competitive pricing strategies across all snack price points, and expand high-end brand offerings internationally [4] - Unilever is concentrating resources on its "Power Brands," which contribute 78% of sales and achieved a Q3 growth rate of 4.4%, significantly above the overall performance [4] Future Outlook - The company anticipates an improvement in operating profit margins, projecting at least 18.5% for the second half of the year [5] - Unilever aims for a full-year sales growth of 3% to 5% by 2025, with expectations of stronger performance in the second half compared to the first [8] - The management remains optimistic about the transformation despite the ongoing challenges, focusing on a streamlined portfolio that includes beauty, health, personal care, home care, and nutrition [8]

申万宏源证券晨会报告-20251028

Shenwan Hongyuan Securities· 2025-10-28 03:14

Core Insights - The report highlights a significant decline in investment growth across various sectors, including infrastructure, services, manufacturing, and real estate, with fixed asset investment growth dropping to historical lows since mid-2025 [11][5][4] - The central bank's decision to resume government bond trading is expected to have a short-term positive impact, but the long-term effects may be neutral due to ongoing economic pressures [12][14] - China Shenhua's Q3 2025 performance showed stable growth despite challenges, with revenue and net profit exceeding market expectations, driven by cost control measures [4][13] Investment Growth Decline - Investment growth has sharply decreased, with fixed asset investment growth falling 9.2 percentage points to -6.5% in September 2025, marking the lowest point in five years [11] - Major sectors such as infrastructure, services, real estate, and manufacturing have all experienced declines, with specific drops of 13.1%, 11.1%, 9.3%, and 9.1% respectively [11] - The decline in construction and installation investment is identified as a primary factor contributing to the overall drop in fixed asset investment [11] Reasons for Investment Slowdown - The acceleration of debt resolution has occupied investment funds, explaining over half of the investment decline, with the issuance of special refinancing bonds significantly impacting available government investment funds [11][5] - Companies are being pressured to clear debts, which has further constrained their ability to invest, particularly affecting state-owned enterprises and the real estate sector [11] - A lack of new projects is also contributing to the investment slowdown, with new construction projects seeing a significant drop in growth [11] Policy Optimization Effects - Recent fiscal measures are aimed at alleviating the impact of debt resolution on investment, with targeted policies already showing some positive effects [11] - The report suggests that improving cash flow for enterprises through debt resolution could restore investment vitality, particularly for small and medium-sized enterprises [11] Company Performance Insights - China Shenhua reported a Q3 2025 revenue of CNY 750.42 billion, a 9.51% increase from Q2, although it represents a 13.10% year-on-year decline [13] - The company’s net profit for Q3 was CNY 144.11 billion, reflecting a 13.54% increase from the previous quarter but a 6.24% year-on-year decline [13] - The company maintains a high dividend payout ratio, planning to distribute CNY 194.71 billion in dividends for the first half of 2025, which is 79% of its net profit [13][17] Market Trends and Future Outlook - The report indicates that the market may experience a short-term boost from the resumption of government bond trading, but the overall economic environment remains challenging [12][14] - The performance of various sectors, including the coal and energy sectors, is under scrutiny, with expectations of continued pressure on profit margins due to fluctuating prices [17][18] - Companies are advised to focus on optimizing costs and enhancing operational efficiency to navigate the current economic landscape [17][18]

冯卫东:我们投的鲍师傅,找到了不依赖IPO的投资盈利方式

创业家· 2025-10-27 10:10

Core Insights - The article emphasizes the long-term value of consumer investment despite recent challenges in the sector, suggesting that the current market conditions may present new opportunities for those who remain committed [1][3] Investment Strategy Adjustments - The company has expanded its investment focus to include sectors like biomedicine and low-altitude economy, categorizing consumer investments into technology and non-technology segments [1] - A shift in investment strategy has occurred, moving away from reliance on IPOs as the primary exit strategy due to the lengthy IPO process, which could take up to 50 years for all potential exits based on current rates [1][2] New Investment Approaches - The establishment of a merger and acquisition (M&A) fund is highlighted, targeting projects from diversified groups, "first-generation" entrepreneurs, and serial entrepreneurs who prefer selling businesses rather than taking them public [4] - The company is also pursuing an industrial integration fund, collaborating with industry leaders and local governments to launch investment funds focused on early and growth-stage companies [5] - A dividend strategy has been introduced, exemplified by the launch of a SPAC product in Macau, which utilizes a revenue-sharing model to invest in profitable businesses with strong cash flows [6][10] Market Outlook - The adjustments in strategy have opened up new investment opportunities that were previously inaccessible under an IPO-focused approach, allowing for a broader range of potential assets [9] - The company anticipates that these new strategies, including the industrial integration fund, M&A fund, and revenue-sharing products, will gain traction and lead to significant returns in the future [13]

奢侈品巨头释放复苏信号;蕾哈娜美妆品牌或被卖?丨二姨看时尚

2 1 Shi Ji Jing Ji Bao Dao· 2025-10-27 08:45

Core Insights - The global luxury goods industry is seeking a new balance amid structural differentiation, driven by creative innovation, market restructuring, and strategic focus [1] Group 1: Company Performance - Prada Group reported a revenue of €4.07 billion for the nine months ending September 30, 2025, an increase of 8.9% year-on-year, with Miu Miu's sales soaring by 41% [2] - Unilever's Q3 sales exceeded expectations, driven by double-digit growth in beauty brands like Dove, with a total turnover of €14.7 billion, down 3.5% year-on-year [3] - Chanel appointed Sarah Weisz-Pirel as the new communications director, emphasizing the brand's strategic focus on crisis and reputation management [4][5] - Kering's Q3 revenue fell by 10% to €3.42 billion, but the decline is narrowing compared to previous quarters, with North America showing a surprising 3% same-store sales growth [6] - L'Oréal's Q3 sales reached €10.33 billion, a 0.5% increase year-on-year, but still below analyst expectations [7][8] - Hermès reported a 9.6% increase in sales to €3.88 billion, although it fell short of market expectations [10][11] - LVMH is considering selling a 50% stake in Fenty Beauty, reflecting a strategic reassessment of its diverse business portfolio [12] - Ermenegildo Zegna's Q3 revenue grew by 0.2% to €398.2 million, with significant improvement in the Greater China region [13][14] Group 2: Market Trends - Swiss watch exports to the U.S. plummeted by 55.6%, resulting in the U.S. losing its status as the largest export market for Swiss watches [17] - The luxury goods sector is witnessing a shift towards high-end beauty and personal care products, as evidenced by Unilever's strategic focus [3][6] - The appointment of Grace Wales Bonner as Hermès' menswear creative director signifies a cultural and strategic shift towards contemporary aesthetics [16] - The collaboration between Hyatt and Home Inn to enter the long-stay hotel market indicates the growing potential of the business travel segment in China [18][19]

开云集团(KER):3Q25核心品牌与主要市场环比改善,结构优化推动修复拐点显现

Haitong Securities International· 2025-10-27 06:24

[Table_Title] 研究报告 Research Report 27 Oct 2025 开云集团 Kering (KER FP) 3Q25 核心品牌与主要市场环比改善,结构优化推动修复拐点显现 Core Brands and Key Markets Show Sequential Recovery in 3Q25, Structural Optimization Drives an Inflection Point 寇媛媛 Yuanyuan Kou 陈芳园 Ashley Chen yy.kou@htisec.com ashley.fy.chen@htisec.com [Table_yemei1] 热点速评 Flash Analysis [Table_summary] (Please see APPENDIX 1 for English summary) 事件:10 月 22 日,开云集团发布 3Q2025 业绩。集团收入同比下降 10%;可比门店增速-5%,汇率带来约 5 个百分 点负面影响。各主要品牌与地区均实现环比改善,北美与西欧表现最佳。 [Table_yejiao1] 本研究报告由海通国际分销, ...

震惊!致癌物质苏丹红从“餐桌”跑到“脸上”

Jing Ji Guan Cha Wang· 2025-10-27 05:28

Core Viewpoint - Multiple cosmetic products have been found to contain the banned substance Sudan Red, leading to a significant safety crisis in the beauty industry, affecting over 800 products and more than 400 brands [1][2][3]. Group 1: Detection and Impact - A third-party testing agency, "Old Dad Testing," discovered Sudan Red in a skin care product, prompting further testing of similar products, all of which tested positive for the substance [1][2]. - The detected Sudan Red levels in various products ranged from 435 to 1982 micrograms per kilogram (ug/kg), with one raw material containing as much as 1170 parts per million (ppm) [2][3]. - The incident has implicated well-known brands such as Kiehl's, FARMACY, and others, with a total of over 800 products identified as containing the problematic ingredient [3][6]. Group 2: Regulatory and Supply Chain Issues - The presence of Sudan Red in cosmetics highlights a significant regulatory oversight in the supply chain, where manufacturers may have added the banned substance to enhance visual appeal [7][8]. - The source of the banned substance is traced back to a supplier in Singapore, which specializes in natural ingredients but has been linked to the inclusion of industrial dyes in cosmetic products [7][8]. - The incident has raised concerns about the reliance of smaller companies on overseas suppliers and the lack of independent testing capabilities, which could lead to safety vulnerabilities [8]. Group 3: Brand Responses and Consumer Guidance - Following the revelation, brands like Kiehl's and Huaxizi have responded by halting sales of affected products and initiating internal investigations [5][6]. - Consumers are advised to check their skincare products for specific ingredients, including Eclipta Prostrata extract, Melia Azadirachta leaf extract, and Moringa Oleifera seed oil, and to refrain from using products containing these until further testing results are available [9].

趋势研判!2025年中国洗护用品行业发展历程、产业链、市场规模、竞争格局及未来趋势:个性化需求日益凸显,推动洗护用品市场规模达3429亿元[图]

Chan Ye Xin Xi Wang· 2025-10-27 01:17

Core Insights - The Chinese personal care industry is experiencing rapid growth driven by the "beauty economy" and "Healthy China" initiatives, with a market size projected to increase from 189.2 billion yuan in 2017 to 342.9 billion yuan in 2024, reflecting a compound annual growth rate (CAGR) of 8.9% [1][12] - Key growth drivers include rising household income, the emergence of younger consumers prioritizing personalized experiences, and the expansion of social media and e-commerce platforms [1][11] - Consumer demand has shifted from basic cleaning functions to a comprehensive pursuit of ingredient safety, precise efficacy, and emotional experience, leading to rapid growth in niche markets such as anti-hair loss and scalp care [1][11] Industry Overview - The personal care industry encompasses various products for cleaning, maintenance, and personal hygiene, including hair care, skin care, oral care, and household cleaning products [4] - The industry has evolved from basic cleaning products in the initial stages to a comprehensive range of products that meet diverse consumer needs [6][8] Market Dynamics - The market is characterized by intense competition between international brands like Procter & Gamble and Unilever and local brands that are gaining market share by understanding local consumer needs [12] - Local brands such as Natural Hall, Baique Ling, and Adolph have successfully captured consumer interest by offering products tailored to local preferences [12] Consumer Trends - Rising disposable income in China, from 26,000 yuan in 2017 to 41,300 yuan in 2024, has led to increased consumer spending on personal care products, with a CAGR of 6.83% [8] - The demand for high-quality, effective, and experiential products is driving consumers to pay premiums for specialized hair care solutions and natural ingredients [8] Supply Chain Insights - The supply chain for personal care products includes raw materials such as surfactants, moisturizers, and emulsifiers, with the production and manufacturing processes occurring in the midstream [8][9] - The surfactant industry, a key raw material for personal care products, is projected to grow from 2.148 million tons in 2015 to 5.0764 million tons in 2024, with a CAGR of 10.03% [10] Future Trends - The industry is expected to see advancements in smart technology, allowing for personalized care solutions based on real-time data analysis [17] - Personalization will become a core focus, enabling consumers to receive tailored products that meet their specific needs [17] - Sustainability will be a key development principle, with an emphasis on natural ingredients, sustainable packaging, and corporate social responsibility [18]