WUS(002463)

Search documents

财通策略、多行业:2025年11月金股

CAITONG SECURITIES· 2025-10-31 11:05

Core Insights - The report emphasizes a strategic shift towards financial and consumer sectors, indicating a positive market outlook following the resolution of tariff impacts and a rebound after initial panic [4][7] - The report highlights the importance of new economic technologies and service consumption, alongside traditional resource industries, as key investment themes for the upcoming quarter [4][7] - The report identifies a favorable environment for investment, driven by domestic policy shifts and international cooperation, particularly in consumption and technology sectors [4][7] Company Summaries - **Haier Smart Home (600690)**: The company is positioned as a global leader in home appliances, focusing on digital transformation and supply chain optimization. It aims to enhance its global competitiveness through increased self-sufficiency in core components and overseas expansion [12] - **Lixing Shares (300421)**: As a leader in the rolling body industry, the company is expanding into high-end products like ceramic rolling bodies, benefiting from the recovery in high-speed rail and wind power sectors, with steady growth expected [13] - **China National Glass (600176)**: The company is experiencing improved profitability due to product price recovery and cost reductions. Its gross margin for Q3 2025 was 32.8%, reflecting a 4.6 percentage point increase year-on-year [14] - **Lihigh Food (300973)**: The company is leveraging management efficiency, channel benefits, and product upgrades to enhance performance [15] - **Muyuan Foods (002714)**: As a leading player in pig farming, the company maintains a solid cost advantage and is committed to high-quality development [16] - **Landai Technology (002765)**: The company is rapidly expanding its new energy business, with significant growth in sales and revenue share expected from 2022 to 2024 [17] - **Hui Electric (002463)**: The company is increasing capital expenditure to support growth, with a focus on AI servers and switches, and is expected to reach a reasonable economic scale by the end of 2025 [19] - **Xiechuang Data (300857)**: The company is investing heavily in computing power, with strong demand for AI computing services driving growth [20] - **Tencent Holdings (00700)**: The company has established a robust user base through its social networks, enabling it to build a diverse ecosystem across various sectors, including digital content and financial technology [21] - **Greentown Service (02869)**: The company is focusing on its core business and reforming its operations, resulting in rapid profit growth and improved financial metrics [22]

沪电股份(002463):经营稳健,产能扩张推进

Guoyuan Securities· 2025-10-31 08:44

Investment Rating - The report maintains a "Buy" rating for the company [5][7]. Core Insights - The company has demonstrated robust operational performance with significant revenue growth driven by structural demand in the printed circuit board (PCB) sector, particularly from high-speed computing servers and artificial intelligence applications [2][5]. - The company's revenue for the first three quarters of 2025 reached 135.12 billion yuan, a year-on-year increase of 49.96%, while the net profit attributable to shareholders was 27.18 billion yuan, up 47.03% year-on-year [1][2]. - The company is expanding its production capacity, with a new project for high-end PCBs for AI chips expected to begin trial production in the second half of 2026 [4]. Financial Performance Summary - For Q3 2025, the company reported revenue of 50.19 billion yuan, a 39.92% increase year-on-year and a 12.62% increase quarter-on-quarter, with a net profit of 10.35 billion yuan, reflecting a 46.25% year-on-year growth [1][2]. - The gross margin for the first three quarters of 2025 was approximately 35.40%, showing a slight year-on-year decline of 0.45 percentage points [2]. - The company’s inventory as of Q3 2025 was 35.92 billion yuan, a 33.5% increase year-on-year, indicating strong demand and production planning [3]. Capacity Expansion and Future Outlook - The company has accelerated capital expenditures, with plans to invest approximately 4.3 billion yuan in a new production facility for AI chip-related PCBs, which commenced construction in June 2025 [4]. - The forecasted net profits for 2025, 2026, and 2027 are expected to be 40.29 billion yuan, 52.26 billion yuan, and 62.28 billion yuan, respectively, with corresponding price-to-earnings (P/E) ratios of 36, 28, and 23 [5].

沪电股份(002463):AI驱动业绩增长,积极推进产能扩充

Dongguan Securities· 2025-10-31 07:26

Investment Rating - The report maintains a "Buy" rating for the company, indicating an expectation that the stock will outperform the market index by more than 15% over the next six months [2][7]. Core Insights - The company's revenue for the first three quarters of 2025 reached 13.512 billion yuan, representing a year-on-year growth of 49.96%. The net profit attributable to shareholders was 2.718 billion yuan, with a year-on-year increase of 47.03% [3][4]. - The growth is primarily driven by the structural demand for PCBs in emerging computing scenarios such as high-performance servers and artificial intelligence [4]. - The company is actively expanding its production capacity to meet the increasing demand for high-end PCBs, with significant investments planned for new projects [4]. Financial Summary - For the first three quarters of 2025, the company's gross margin was 35.40%, a decrease of 0.46 percentage points year-on-year, while the net margin was 20.08%, down 0.23 percentage points year-on-year [4]. - The projected earnings per share (EPS) for 2025 and 2026 are 2.07 yuan and 2.96 yuan, respectively, with corresponding price-to-earnings (PE) ratios of 37 and 26 times [4][5]. - The total revenue forecast for 2025 is 18.882 billion yuan, with a net profit of approximately 3.977 billion yuan [5].

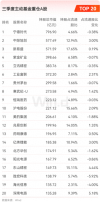

公募三季报持仓洗牌:科技股“七雄”霸榜,茅台失宠,ST华通成黑马

Hua Xia Shi Bao· 2025-10-30 13:16

Core Viewpoint - The report highlights significant shifts in the holdings of actively managed equity funds in the third quarter of 2025, with a notable rise in technology stocks and a decline in traditional consumer stocks like Kweichow Moutai [3][4][6]. Group 1: Fund Holdings Overview - As of September 2025, the total assets under management in the public fund industry reached 35.85 trillion yuan, a quarter-on-quarter increase of 6.30% [3]. - The top three holdings of actively managed equity funds are dominated by technology companies, with CATL reclaiming the top position, surpassing Tencent Holdings [3][4]. - Kweichow Moutai's total market value held by active equity funds decreased to 29.958 billion yuan, down from 30.616 billion yuan in the previous quarter, dropping from third to seventh place among top holdings [3][6]. Group 2: Technology Sector Performance - The technology sector emerged as the primary focus for public fund investments, with seven out of the top ten holdings being technology-related companies [4]. - Notable performers include Xinyi Technology and Zhongji Xuchuang, both of which ranked among the top three heavyweights [4]. - The current market trend indicates a strong and sustained interest in technology stocks, driven by China's economic transformation towards a hard-tech model [4][5]. Group 3: Challenges in Traditional Consumer Sector - The traditional consumer sector, particularly the liquor industry, is facing significant challenges, with 59.7% of liquor companies reporting a decrease in operating profits [6][7]. - The white liquor market is undergoing a deep adjustment phase due to policy changes, consumption structure transformation, and intense competition [6][7]. - The overall sales volume in the liquor industry is expected to decline by over 20% year-on-year, reflecting macroeconomic fluctuations and slow recovery in consumer spending [7][8]. Group 4: Fund Manager Strategies - The top five stocks with increased holdings include Zhongji Xuchuang, Industrial Fulian, ST Huatuo, Dongshan Precision, and Hanwha Technology, all of which are technology companies [9][10]. - Conversely, the top stocks with reduced holdings include Shenghong Technology and Haiguang Information, with significant sell-offs attributed to internal management's actions [11]. - Despite CATL being the top holding, it also appears on the list of reduced holdings, indicating a complex strategy among institutional investors [11].

这七只股藏不住了! 国信证券称AI机柜方案将持续放量

智通财经网· 2025-10-30 09:09

Core Insights - The demand for AI servers is rapidly expanding, leading major global cloud service providers (CSPs) to increase procurement of NVIDIA GPU solutions and expand data center infrastructure [1] - Capital expenditures for eight major CSPs, including Google, AWS, Meta, Microsoft, Oracle, Tencent, Alibaba, and Baidu, are projected to exceed $420 billion by 2025, representing a 61% year-on-year increase [1] - By 2026, total capital expenditures for CSPs are expected to reach a new high of over $520 billion, driven by the continued rollout of AI cabinet solutions [1] - Morgan Stanley forecasts that global cloud capital expenditures could reach $820 billion by 2026, with a year-on-year growth of 31%, significantly surpassing the market consensus of 16% [1] - Capital expenditures for AI servers are anticipated to grow by 70%, indicating an unprecedented growth trajectory [1] Industry Focus - The AI sector is identified as a high-growth investment theme with strong demand certainty, prompting recommendations to focus on companies such as Hon Hai Precision Industry, Huaqin Technology, Huadian Technology, Loongson Technology, Lenovo Group, Luxshare Precision, and Amlogic [1]

AI仍是需求确定性高增长的投资主线 国信证券看好工业富联、联想等七只股

Ge Long Hui· 2025-10-30 09:09

Core Insights - The demand for AI servers is rapidly expanding, leading major global cloud service providers (CSPs) to increase procurement of NVIDIA GPU solutions and expand data center infrastructure [1] - Capital expenditures for eight major CSPs, including Google, AWS, Meta, Microsoft, Oracle, Tencent, Alibaba, and Baidu, are projected to exceed $420 billion by 2025, representing a 61% year-on-year increase [1] - By 2026, total capital expenditures for CSPs are expected to reach a new high of over $520 billion, driven by the continued rollout of AI cabinet solutions [1] - Morgan Stanley forecasts that global cloud capital expenditures could reach $820 billion by 2026, a 31% year-on-year growth, significantly surpassing the market consensus of 16% [1] - Capital expenditures for AI servers are anticipated to grow by 70%, indicating an unprecedented growth trajectory [1] Industry Focus - The AI sector remains a high-growth investment theme with strong demand certainty, prompting recommendations to focus on companies such as Hon Hai Precision Industry, Huaqin Technology, Huadian Technology, Loongson Technology, Lenovo Group, Luxshare Precision, and Amlogic [1]

【招商电子】沪电股份:Q3业绩符合市场预期,利润保持同环比增长趋势

招商电子· 2025-10-30 01:20

Core Viewpoint - The company reported strong Q3 performance with continued high growth in revenue and improved profitability, driven by accelerated capacity expansion and a global strategy that is expected to sustain high growth in performance [2][3]. Financial Performance - For the first three quarters, revenue reached 13.512 billion, a year-on-year increase of 49.96%, while net profit attributable to shareholders was 2.718 billion, up 47.03% year-on-year. The non-recurring net profit was 2.676 billion, reflecting a 48.17% increase year-on-year [3]. - In Q3 alone, revenue was 5.019 billion, showing a year-on-year growth of 39.92% and a quarter-on-quarter increase of 12.62%. The net profit attributable to shareholders was 1.035 billion, up 46.25% year-on-year and 12.44% quarter-on-quarter [3]. - The gross margin for Q3 was 35.84%, a year-on-year increase of 0.90 percentage points, while the net margin was 20.62%, up 1.05 percentage points year-on-year [3]. Key Indicators - As of the end of Q3 2025, fixed assets amounted to 5.22 billion, a 29.4% increase from the beginning of the year, primarily due to construction projects being transferred to fixed assets [4]. - Inventory increased to 3.59 billion, up 0.5 billion from the end of Q2, and accounts receivable rose to 4.87 billion, indicating strong demand from downstream computing power customers [4]. Future Outlook - Looking ahead to Q4, the company expects continued improvement in capacity utilization and product structure optimization, which may further enhance profitability [4]. - The acceleration of global AI technology development is anticipated to drive demand for computing power, with the company planning to deepen strategic cooperation with leading clients in Europe and the U.S. [4]. - The company is advancing its overseas capacity construction and improving its global supply chain, which is expected to enhance customer service capabilities and market responsiveness [4].

开源晨会-20251029

KAIYUAN SECURITIES· 2025-10-29 14:45

Group 1: Market Overview - The report highlights the recent performance of the Shanghai Composite Index and the ChiNext Index, showing a significant decline over the past year, with the Shanghai Composite down by 32% and the ChiNext down by 16% [1][2] Group 2: Industry Insights - The report discusses the strong performance of the power equipment and non-bank financial sectors, with power equipment showing a rise of 4.79% and non-bank financials increasing by 2.08% in the latest trading session [1] - Conversely, the banking sector experienced a decline of 1.98%, indicating a challenging environment for traditional financial institutions [2] Group 3: Investment Strategies - The report emphasizes a dual-driven strategy focusing on technology and PPI trading, suggesting that AI and self-controlled technology will lead the market, supported by stable dividends and sectors like gold and military [6] - The recommended industry sectors for November include social services, non-bank financials, and public utilities, indicating a diversified approach to investment [7] Group 4: Company-Specific Updates - Celestica reported a strong Q3 performance with revenues of $3.19 billion, a 28% year-over-year increase, and raised its full-year revenue guidance to $12.2 billion, reflecting confidence in the AI infrastructure market [20] - Tesla plans to launch its Optimus V3 robot by Q1 2026, with a production capacity of 1 million units per year, showcasing advancements in robotics and AI [29][30] - The report notes that the food and beverage sector, particularly companies like Hai Tian Wei Ye, has shown steady revenue growth of 2.5% and profit growth of 3.4% in Q3 2025, highlighting resilience in challenging market conditions [51]

沪电股份(002463):加速扩充高阶产能,静待产能瓶颈打开大放异彩

CAITONG SECURITIES· 2025-10-29 13:13

Investment Rating - The investment rating for the company is "Accumulate" (maintained) [2] Core Views - The company has accelerated the expansion of high-end production capacity, anticipating a significant performance boost once capacity constraints are alleviated [1] - The company reported a revenue of 13.51 billion yuan for the first three quarters of 2025, representing a year-on-year growth of 49.96%, and a net profit attributable to shareholders of 2.72 billion yuan, up 47.03% year-on-year [8] - The demand for AI is robust, driving continuous high growth in performance, with the company benefiting from structural demand for printed circuit boards in high-performance computing and AI applications [8] - The company is expected to achieve revenues of 18.23 billion yuan, 23.88 billion yuan, and 32.70 billion yuan for 2025, 2026, and 2027 respectively, with net profits of 3.90 billion yuan, 5.17 billion yuan, and 7.24 billion yuan for the same years [8] Financial Performance - The company achieved a revenue of 50.19 billion yuan in Q3 2025, a year-on-year increase of 39.92% and a quarter-on-quarter increase of 12.62% [8] - The gross margin for Q3 2025 was 35.84%, reflecting a year-on-year increase of 0.9 percentage points but a quarter-on-quarter decline of 1.47 percentage points due to increased stock incentive costs and other factors [8] - The company has maintained high levels of capital expenditure, with cash payments for fixed assets and other long-term assets amounting to approximately 1.39 billion yuan in the first half of 2025 and 715 million yuan in Q3 2025 [8] Earnings Forecast - The company is projected to achieve a revenue growth rate of 36.6% in 2025, followed by 31.0% in 2026 and 36.9% in 2027 [7] - The expected earnings per share (EPS) for 2025 is 2.03 yuan, with a price-to-earnings (PE) ratio of 39.5 [7] - The return on equity (ROE) is forecasted to increase to 27.0% in 2025 and further to 32.6% by 2027 [7]

沪电股份(002463):Q3延续高增长趋势,产能扩张打开成长空间

Xinda Securities· 2025-10-29 09:34

Investment Rating - The investment rating for the company is "Buy" [3] Core Views - The company is experiencing strong growth driven by AI, with high demand for server and switch PCB products. The performance is primarily benefiting from the structural demand for high-end printed circuit boards (PCBs) in emerging computing scenarios such as high-performance computing and artificial intelligence. The PCB market is projected to grow from $73.6 billion in 2024 to $94.7 billion in 2029, with a five-year CAGR of 5.2% [3] - The company is accelerating capacity expansion to meet the robust downstream demand driven by AI. A project to expand high-end printed circuit board capacity for AI chips has been initiated with a total investment of approximately 4.3 billion yuan, expected to begin trial production in the second half of 2026. The overseas production base in Thailand has entered small-scale production, receiving formal recognition from clients in AI server and switch applications [3] - Profit forecasts indicate that the company's net profit attributable to shareholders is expected to reach 3.882 billion yuan, 5.992 billion yuan, and 7.565 billion yuan for 2025, 2026, and 2027 respectively, with corresponding P/E ratios of 39.35, 25.49, and 20.19. The company is viewed as a core player in the computing power industry chain, and the outlook for its development in this field is positive [3] Financial Summary - For the third quarter, the company achieved operating revenue of 5.019 billion yuan, a year-on-year increase of 39.92% and a quarter-on-quarter increase of 12.63%. The net profit attributable to shareholders was 1.035 billion yuan, up 46.19% year-on-year and 12.50% quarter-on-quarter. For the first three quarters, the operating revenue reached 13.512 billion yuan, a year-on-year increase of 49.96%, and the net profit attributable to shareholders was 2.718 billion yuan, up 47.03% year-on-year [1][3] - Key financial indicators for 2025E include total revenue of 17.512 billion yuan, net profit of 3.882 billion yuan, and a gross margin of 38.8% [4]