POP MART(09992)

Search documents

智通港股通持股解析|10月23日

智通财经网· 2025-10-23 00:32

Core Insights - The top three companies by Hong Kong Stock Connect holding ratios are China Telecom (71.22%), COSCO Shipping Energy (70.13%), and GCL-Poly Energy (69.57%) [1] - In the last five trading days, the largest increases in holding amounts were seen in China Mobile (+1.929 billion), Tracker Fund of Hong Kong (+1.897 billion), and InnoCare Pharma (+1.751 billion) [1] - Conversely, Alibaba (-3.254 billion), SMIC (-2.330 billion), and Laopuhuang (-0.855 billion) experienced the largest decreases in holding amounts [2] Group 1: Hong Kong Stock Connect Holding Ratios - China Telecom (00728) has a holding ratio of 71.22% with 9.884 billion shares [1] - COSCO Shipping Energy (01138) has a holding ratio of 70.13% with 909 million shares [1] - GCL-Poly Energy (01330) has a holding ratio of 69.57% with 281 million shares [1] - Other notable companies include China Shenhua (67.74%), Kaisa Group (67.61%), and Xinte Energy (65.33%) [1] Group 2: Recent Increases in Holdings - China Mobile (00941) saw an increase of 1.929 billion in holding amount and 22.8427 million shares [1] - Tracker Fund of Hong Kong (02800) increased by 1.897 billion and 71.8145 million shares [1] - InnoCare Pharma (09606) increased by 1.751 billion and 5.5669 million shares [1] - Other companies with significant increases include Meituan-W (+1.592 billion) and Xiaomi Group-W (+1.105 billion) [1] Group 3: Recent Decreases in Holdings - Alibaba-W (09988) experienced a decrease of 3.254 billion in holding amount and 20.0969 million shares [2] - SMIC (00981) saw a decrease of 2.330 billion and 31.1261 million shares [2] - Laopuhuang (06181) decreased by 0.855 billion and 1.2141 million shares [2] - Other companies with notable decreases include Huahong Semiconductor (-0.792 billion) and Jiangxi Copper (-0.651 billion) [2]

iPhone Air在华首发遇冷,金价创12年来最大单日跌幅 | 财经日日评

吴晓波频道· 2025-10-23 00:30

Economic Indicators - In the first three quarters of 2025, the national per capita disposable income reached 32,509 yuan, with a nominal growth of 5.1% and a real growth of 5.2% after adjusting for price factors [2] - Urban residents had a per capita disposable income of 42,991 yuan, with a nominal growth of 4.4% and a real growth of 4.5%, while rural residents had 17,686 yuan, with a nominal growth of 5.7% and a real growth of 6.0% [2] - The income gap between regions remains significant, with high-income provinces like Shanghai and Beijing exceeding 65,000 yuan, while provinces like Gansu and Xinjiang are below 21,000 yuan, indicating a disparity of over three times [3] Gold Market - On October 21, international gold prices experienced their largest single-day drop in 12 years, with spot gold falling by 5.31% to $4,124.36 per ounce [4] - The decline in gold prices is attributed to a lack of support for the previous rapid increase, driven more by market sentiment than fundamentals, as geopolitical tensions ease and trade relations improve [4][5] - Short-term volatility in gold prices is expected to remain high, while the long-term outlook will depend on the global economic recovery or recession [5] Apple iPhone Launch - The launch of iPhone Air in mainland China saw a lukewarm response, with no long queues at major retail stores, contrasting sharply with the global launch of the iPhone 17 series [6] - The iPhone Air's pricing strategy at 7,999 yuan is considered high for Chinese consumers, and its exclusive support for eSIM technology may hinder adoption [6] - Despite the slow start for iPhone Air, the overall performance of the iPhone 17 series has been strong, with a 14% increase in sales compared to the previous generation [7] OpenAI Browser Launch - OpenAI launched its AI-driven web browser, ChatGPT Atlas, which allows users to interact with ChatGPT while browsing [8] - The browser is seen as a strategic move to enhance OpenAI's software ecosystem and compete directly with Google's Chrome, which has integrated AI features [8][9] - While Atlas offers similar functionalities to Chrome, it may face challenges in competing due to the established ecosystem of Chrome and its extensive plugin support [9] BYD's Strategic Partnership - BYD has entered a strategic partnership with Japan's AEON to establish sales points for electric vehicles in approximately 30 commercial facilities across Japan by 2025 [10] - The partnership aims to make BYD electric vehicles available at a starting price of around 2 million yen (approximately 94,000 yuan) [10] - Despite previous marketing efforts, BYD has faced challenges in gaining market share in Japan, highlighting the need for a more localized approach to consumer preferences [11][12] Pop Mart's Revenue Growth - Pop Mart reported a 245%-250% year-on-year increase in overall revenue for Q3 2025, with significant growth in both domestic and international markets [13] - The company's online sales growth outpaced offline sales, and its popular Labubu plush toy contributed to a substantial revenue increase in the first half of 2025 [13] - To combat the secondary market for its products, Pop Mart has implemented strategies such as increasing production and offering online pre-orders [14] Stock Trading App Usage - In September 2025, the monthly active user count for securities apps reached 175 million, marking a 0.74% increase from the previous month and a 9.73% year-on-year growth [15] - The number of new A-share accounts opened in September was 2.9372 million, a 60.73% increase year-on-year, indicating heightened interest in the stock market [15] - The rise in younger investors suggests that traditional brokerage firms may need to adapt to remain competitive in the evolving market landscape [16] Market Performance - On October 22, the stock market experienced slight fluctuations, with the Shanghai Composite Index closing down 0.07% [17] - Market activity was characterized by a decrease in trading volume, with a focus on sectors like deep earth economy and banking, while battery stocks faced declines [17][18] - Anticipation of upcoming trade negotiations and policy meetings may influence market sentiment and trading activity in the near term [18]

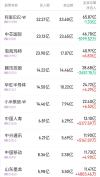

智通港股通资金流向统计(T+2)|10月23日

智通财经网· 2025-10-22 23:33

Core Insights - The top three companies with net inflows from southbound funds are China Mobile, Zijin Mining International, and InnoCare Pharma-B, with net inflows of 570 million, 494 million, and 457 million respectively [1] - The top three companies with net outflows are Alibaba-W, Innovent Biologics, and the Tracker Fund of Hong Kong, with net outflows of -1.758 billion, -494 million, and -450 million respectively [1] - In terms of net inflow ratios, E Fund Hang Seng ESG, GX Hang Seng Technology, and China Taiping lead the market with ratios of 99.40%, 75.71%, and 62.07% respectively [1] Net Inflow Rankings - The top net inflow stocks include: - China Mobile (00941) with a net inflow of 570 million and a closing price of 86.400, up 1.29% [2] - Zijin Mining International (02259) with a net inflow of 494 million and a closing price of 139.900, down 5.35% [2] - InnoCare Pharma-B (09606) with a net inflow of 457 million and a closing price of 340.000, up 1.74% [2] Net Outflow Rankings - The top net outflow stocks include: - Alibaba-W (09988) with a net outflow of -1.758 billion and a closing price of 161.900, up 4.86% [2] - Innovent Biologics (01801) with a net outflow of -494 million and a closing price of 86.100, down 0.86% [2] - Tracker Fund of Hong Kong (02800) with a net outflow of -450 million and a closing price of 26.520, up 2.55% [2] Net Inflow Ratio Rankings - The top net inflow ratio stocks include: - E Fund Hang Seng ESG (03039) with a net inflow ratio of 99.40% and a closing price of 3.898, up 2.96% [3] - GX Hang Seng Technology (02837) with a net inflow ratio of 75.71% and a closing price of 7.315, up 3.10% [3] - China Taiping (00966) with a net inflow ratio of 62.07% and a closing price of 16.750, up 2.13% [3]

北水成交净买入11.71亿 泡泡玛特盘后发布盈喜 北水全天抢筹超11亿港元

Zhi Tong Cai Jing· 2025-10-22 17:11

Core Viewpoint - The Hong Kong stock market experienced significant net inflows from northbound trading, with notable buying activity in specific stocks such as Pop Mart and Xiaomi, while other stocks like Alibaba faced substantial net selling [2][6]. Group 1: Stock Performance - Pop Mart (09992) received a net inflow of HKD 11.2 billion, with a projected revenue growth of 245%-250% year-on-year for Q3 2025, driven by strong domestic and international sales [6]. - Xiaomi Group-W (01810) saw a net inflow of HKD 4.81 billion, following a share buyback of 10.7 million shares at prices between HKD 45.9 and HKD 46.76, totaling approximately HKD 4.94 billion [6]. - Semiconductor stocks, including Huahong Semiconductor (01347) and SMIC (00981), attracted net inflows of HKD 4.41 billion and HKD 1.28 billion, respectively, amid positive sentiment regarding the semiconductor industry's growth driven by AI [6]. Group 2: Company Earnings and Projections - China Mobile (00941) reported Q3 service revenue of HKD 216.2 billion, a year-on-year increase of 0.8%, with EBITDA declining by 1.7% to HKD 79.4 billion, slightly below market expectations [7]. - China Life (02628) projected a net profit of approximately HKD 156.79 billion to HKD 177.69 billion for the first three quarters, reflecting a year-on-year growth of 50% to 70% [7]. - The report indicated that the net profit for Q3 could grow by 75% to 106% year-on-year, driven by improved investment returns and optimized asset allocation [7]. Group 3: Market Sentiment and Trends - The overall market sentiment showed a divergence in fund flows, with significant net selling in stocks like Alibaba (09988) and Tencent (00700), indicating cautious investor sentiment amid global economic uncertainties [8]. - The report highlighted that the current market volatility is influenced more by emotional factors rather than fundamental reversals, suggesting a need for careful timing in investment strategies [7].

中国潮玩迈向品牌“出海”

Zheng Quan Ri Bao Zhi Sheng· 2025-10-22 16:40

Core Insights - The article highlights the significant growth of Chinese潮玩 (trendy toys) brands in overseas markets, particularly by泡泡玛特 (Pop Mart), which reported substantial revenue increases across various regions in Q3 2025 [1][4] - The trend of self-owned IPs going global is emphasized, with companies focusing on their own intellectual properties rather than licensed ones [1][4] Group 1: Revenue Growth - In Q3 2025,泡泡玛特's overseas revenue in the Asia-Pacific region grew by 170% to 175%, in the Americas by 1265% to 1270%, and in Europe and other regions by 735% to 740% [1] - The overall export of toys from China, including trendy toys, exceeded 500 billion yuan in the first three quarters of 2025, reaching over 200 countries and regions [1] Group 2: Self-Owned IP Expansion -潮玩 brand HERE奇梦岛 has accelerated the international expansion of its self-owned IPs like WAKUKU and SIINONO, successfully launching multiple pop-up stores in Dubai, Indonesia, and Thailand [2] - 52TOYS showcased its self-owned IPs at major international exhibitions, with its变形机甲猛兽匣 series gaining significant attention and sales in overseas markets [2][3] Group 3: Market Strategy and Localization - The transition from "product export" to "brand export" is noted, indicating a shift towards exporting IP, culture, and complete consumer experiences [4] - HERE奇梦岛 emphasizes the importance of deep localization for emotional resonance, which includes understanding local cultural symbols and social habits [5]

港股通(深)净买入33.25亿港元

Zheng Quan Shi Bao Wang· 2025-10-22 14:29

Core Viewpoint - On October 22, the Hang Seng Index fell by 0.94% to close at 25,781.77 points, while southbound funds through the Stock Connect recorded a net purchase of HKD 10.018 billion [1] Group 1: Market Activity - The total trading volume for the Stock Connect on October 22 was HKD 106.582 billion, with a net purchase of HKD 10.018 billion [1] - The Shanghai Stock Connect accounted for HKD 66.693 billion in trading volume, with a net purchase of HKD 6.693 billion, while the Shenzhen Stock Connect had a trading volume of HKD 39.887 billion and a net purchase of HKD 3.325 billion [1] Group 2: Active Stocks - In the Shanghai Stock Connect, Alibaba-W had the highest trading volume at HKD 41.14 billion, followed by SMIC and Innovent Biologics with HKD 34.07 billion and HKD 32.39 billion respectively [1] - The top net purchase stock was the Tracker Fund of Hong Kong (盈富基金) with a net purchase of HKD 12.93 billion, despite a closing price drop of 1.05% [1] - Alibaba-W recorded the highest net sell amount at HKD 1.80 billion, closing down by 1.94% [1] Group 3: Shenzhen Stock Connect Activity - In the Shenzhen Stock Connect, Innovent Biologics led with a trading volume of HKD 26.84 billion, followed by Alibaba-W and Pop Mart with HKD 24.66 billion and HKD 23.36 billion respectively [2] - The Tracker Fund of Hong Kong (盈富基金) also had a net purchase of HKD 7.02 billion, closing down by 1.05% [2] - Innovent Biologics had the highest net sell amount at HKD 2.53 billion, with a closing price drop of 1.96% [2]

LABUBU卡牌带火“纸片经济”,二手平台溢价约30%

Mei Ri Jing Ji Xin Wen· 2025-10-22 13:45

Core Insights - The focus of the "Double 11" shopping festival has unexpectedly shifted to collectible cards, particularly the TOPPS X THE MONSTERS/LABUBU series, which sold out quickly despite high purchase limits and pre-sale conditions [1][2] - The collectible card market in China is experiencing significant growth, with major players like Pokémon and various entertainment giants entering the space, leading to a competitive landscape [1][6] - Bubble Mart, a leading player in the trendy toy industry, reported a projected revenue growth of 245%-250% year-on-year for Q3 2025, indicating strong performance in the collectible market [1][4] Market Dynamics - The overlap between trendy toy users and card users is significant, with many card players also engaging with Bubble Mart products, although marketing strategies differ [2][5] - The traditional IP-licensed cards are facing challenges as the market becomes saturated, leading to increased competition primarily based on price and volume [2][5] - The LABUBU card's appeal lies in its unique scarcity and artistic value, featuring limited edition items that enhance its collectible nature [3][5] Competitive Landscape - The global collectible trading card market is projected to grow from $7.267 billion in 2025 to $15.433 billion by 2032, with a compound annual growth rate of 11.36% [3][4] - China has emerged as one of the largest trading card markets, with significant growth potential as consumer spending is still relatively low compared to markets like Japan and the U.S. [4][6] - Major companies in the first tier of the market include Pokémon, Konami, and Topps, with a clear competitive hierarchy forming [4][6] Industry Trends - The Chinese card market is witnessing an influx of new players, with over 2,000 card-related companies currently operating, primarily concentrated in Guangdong, Liaoning, and Hainan [6][7] - The market is evolving towards a more mature and diversified structure, with a broader age demographic engaging with various IPs [7][8] - The future of the card market may hinge on the development of trading card games (TCG) that offer gameplay and competitive events, moving away from purely collectible cards [8]

北水成交净买入100.18亿 内资抢筹盈富基金近20亿港元 继续加仓中海油

Zhi Tong Cai Jing· 2025-10-22 13:29

Core Viewpoint - The Hong Kong stock market experienced significant net inflows from northbound trading, with notable buying activity in specific stocks such as China National Offshore Oil Corporation (CNOOC), Semiconductor Manufacturing International Corporation (SMIC), and Pop Mart International. Conversely, stocks like Hua Hong Semiconductor, Xiaomi, and Alibaba faced net selling pressure [2][7]. Group 1: Northbound Trading Activity - Northbound trading recorded a net inflow of 100.18 billion HKD, with 66.93 billion HKD from the Shanghai Stock Connect and 33.25 billion HKD from the Shenzhen Stock Connect [2]. - The most bought stocks included the Tracker Fund of Hong Kong (02800), CNOOC (00883), and SMIC (00981) [2]. - The most sold stocks were Hua Hong Semiconductor (01347), Xiaomi Group-W (01810), and Alibaba Group-W (09988) [2]. Group 2: Stock Performance and Analysis - SMIC saw a net inflow of 18.49 billion HKD in buying, with a selling amount of 15.57 billion HKD, resulting in a total transaction volume of 34.07 billion HKD [3]. - CNOOC received a net buy of 14.24 billion HKD, supported by reports indicating a focus on increasing reserves and production amid external uncertainties [7]. - Pop Mart reported a strong third-quarter performance with revenue growth of 245% to 250% year-on-year, leading to an upgrade in earnings forecasts by Bank of America [8]. Group 3: Sector Insights - The semiconductor sector showed divergence, with SMIC gaining net inflows of 6.42 billion HKD while Hua Hong Semiconductor faced net outflows of 2.97 billion HKD [7]. - Analysts remain optimistic about the semiconductor industry's growth driven by artificial intelligence and domestic production capabilities amid U.S. export controls [7]. - The collaboration between Innovent Biologics and Takeda Pharmaceuticals is expected to yield significant financial benefits, with potential payments reaching up to 114 billion USD [8].

经营的本质是什么?

Hu Xiu· 2025-10-22 13:24

Core Insights - The article discusses the importance of both external cycles and internal organization in determining a company's success or failure during different market conditions [1][2][3] - It presents a four-quadrant model to categorize companies based on their organizational strength and market cycles, illustrating how these factors interact to shape business outcomes [3][4] Quadrant Analysis Quadrant 1: Upward Cycle + Organizational Evolution - Companies like Mixue Ice City and Pop Mart thrive during industry booms due to strategic accuracy and efficient execution, benefiting from favorable market conditions [6][7] - Mixue Ice City's success is attributed to its low-cost model and 100% self-sourced supply chain, achieving high gross and net profit margins in the new tea beverage sector [10][11][12] - Pop Mart capitalizes on global expansion and market adaptability, demonstrating a keen understanding of market dynamics despite periods of lower visibility [14][15][16] Quadrant 2: Downward Cycle + Organizational Evolution - Companies such as Bottle Planet and Midea exemplify resilience in challenging environments, adapting their strategies to align with market demands [17][18] - Bottle Planet, known for its brand Jiangxiaobai, pivoted to a "new liquor" strategy to counteract declining traditional liquor sales, leading to renewed growth [20][21][24] - Midea's transformation into a technology ecosystem company, driven by a focus on organizational strength over individual leadership, has resulted in significant market value growth [26][27] Quadrant 3: Upward Cycle + Organizational Degeneration - Wahaha and Li Ning illustrate how poor organizational management can squander opportunities during favorable market conditions [28][29] - Wahaha's leadership struggles have hindered its ability to capitalize on the bottled water market, while Li Ning's missteps in brand strategy have led to significant market value decline [30][34][35] Quadrant 4: Downward Cycle + Organizational Degeneration - Companies like Master Kong and Three Squirrels face compounded challenges from external market pressures and internal management issues [37][38] - Master Kong's sales have declined due to the rise of food delivery services, while its strategies have failed to adapt effectively to changing consumer preferences [39][41] - Three Squirrels struggles with maintaining quality and adapting to market changes, resulting in significant revenue losses and competitive disadvantages [43][44] Conclusion - The analysis emphasizes that while market cycles are constant, the organizational structure and adaptability of a company are crucial for long-term survival and success [45][46][47]

泡泡玛特(09992.HK)25Q3经营情况前瞻:新品上新势能强劲 预计各渠道持续高速增长

Ge Long Hui· 2025-10-22 12:55

Core Viewpoint - The company is expected to show strong growth in Q3 2025, with significant increases in revenue and adjusted net profit driven by new product launches and continuous channel growth [1][2] Financial Performance - For Q3 2025, the company anticipates a revenue growth of 154.2% year-on-year, reaching approximately 9.17 billion yuan, and an adjusted net profit growth of 198.6%, amounting to about 3.03 billion yuan [1] - The adjusted profit margin is projected to be 33% [1] Product Development - In Q3 2025, the company plans to launch 31 new series of blind box figures and plush products, with a slight decrease in new series compared to the previous quarter but maintaining year-on-year levels [1] - Popular new products include various themed series that sold out on their launch day [1] Retail Expansion - As of the end of August, the company had 513 retail stores in mainland China, a 6.4% increase year-on-year, and 1,837 robot stores [1] - The average revenue per store increased by 57% to 2.48 million yuan for the July-August period [1] Online Sales Performance - The company's official Douyin flagship store achieved a GMV of 1.31 billion yuan in Q3 2025, a year-on-year increase of 302.2%, with sales volume reaching 9.49 million, up 677.9% [2] - The Tmall flagship store generated revenue of 251 million yuan, a 73.1% increase year-on-year, while JD.com saw a revenue increase of 99.6% for the same period [2] Future Outlook - The company has adjusted its profit forecasts for 2025-2027, with expected adjusted net profits of 10.96 billion, 14.92 billion, and 18.31 billion yuan respectively [2] - The adjusted PE ratios for 2025-2027 are projected to be 32.3x, 23.8x, and 19.4x [2]